Skip to content

Skip to content

A car crash can change your life in seconds—but you don’t have to face recovery alone. The violent jolt, the shock, and the confusing aftermath often leave you feeling lost and unsure what to do next. If you're now struggling with the nagging, persistent pain of whiplash, please know you aren't alone—and help is available.

Your Guide to Texas Whiplash Settlements

This guide is here to explain the settlement for whiplash process here in Texas. Our goal is to give you the knowledge you need to stand up for your rights. Whiplash is so much more than a "sore neck." It's a serious soft tissue injury that can interfere with your job, your family life, and your overall well-being. A fair settlement needs to cover all of these impacts, not just the bill from your first trip to the ER.

We're going to break down exactly what goes into a whiplash settlement and give you a clear, step-by-step roadmap to help you handle your claim with confidence. Let's get started by looking at the core pieces that determine what your claim is truly worth.

Understanding the Injury Is Key

Before you can understand the claim, you have to understand the injury. Whiplash is often called Whiplash: The Invisible Injury for a good reason. Unlike a broken bone that shows up clearly on an X-ray, whiplash symptoms can be sneaky, sometimes not showing up for days after the accident.

You might start to notice things like:

- Nagging neck pain and stiffness that won't go away

- Headaches, especially those that seem to start at the base of your skull

- Feeling dizzy, foggy, or unusually tired

- A strange tingling or numbness running down your arms

Because these injuries aren't always obvious, insurance adjusters often try to downplay them or argue they aren't that serious. This is exactly why getting proper medical documentation and solid legal advice is so critical from the very beginning.

What Your Settlement Should Cover

A fair settlement for whiplash is about much more than just paying for your immediate medical bills. It needs to account for every single way this injury has impacted your life. In Texas, the person whose carelessness caused your injury is responsible for your damages—that's the legal term for all the losses you've suffered.

Your recovery should cover both the tangible, out-of-pocket costs and the very real, personal toll the injury takes on your daily life. This means accounting for both economic and non-economic damages.

Think about it this way: a Houston driver rear-ended on I-45 might have a growing stack of bills from their chiropractor and physical therapist. But they might also miss weeks of work, losing thousands in income. On top of that, the chronic pain could stop them from playing with their kids or enjoying their weekend hobbies. A fair settlement has to look at that whole picture to truly make things right. At The Law Office of Bryan Fagan, our Houston car accident lawyers fight to make sure every single loss is counted.

What Is a Typical Settlement for Whiplash?

After a car crash, one of the first questions that runs through your mind is, "What is my claim actually worth?" While there's no magic calculator that can spit out a number, understanding the typical ranges for a settlement for whiplash can help you set realistic expectations. Every single case is different, but real-world data gives us a solid starting point.

The final settlement amount is always tied directly to how severe your injury is and how much it has upended your life. A minor fender-bender on a quiet street in The Woodlands that only requires a few weeks of chiropractic visits will have a completely different value than a high-speed collision on Houston's I-45 that leaves you with chronic pain and a need for long-term physical therapy.

Breaking Down Whiplash Settlement Ranges

Settlement values aren't just random numbers pulled from thin air; they are carefully calculated based on the evidence. Data from experienced injury lawyers across the country shows a huge spectrum of potential outcomes. For instance, a mild case with minimal treatment might just settle for enough to cover your initial medical bills and not much more. But when the injuries are serious, the compensation has to reflect a much greater disruption to your life.

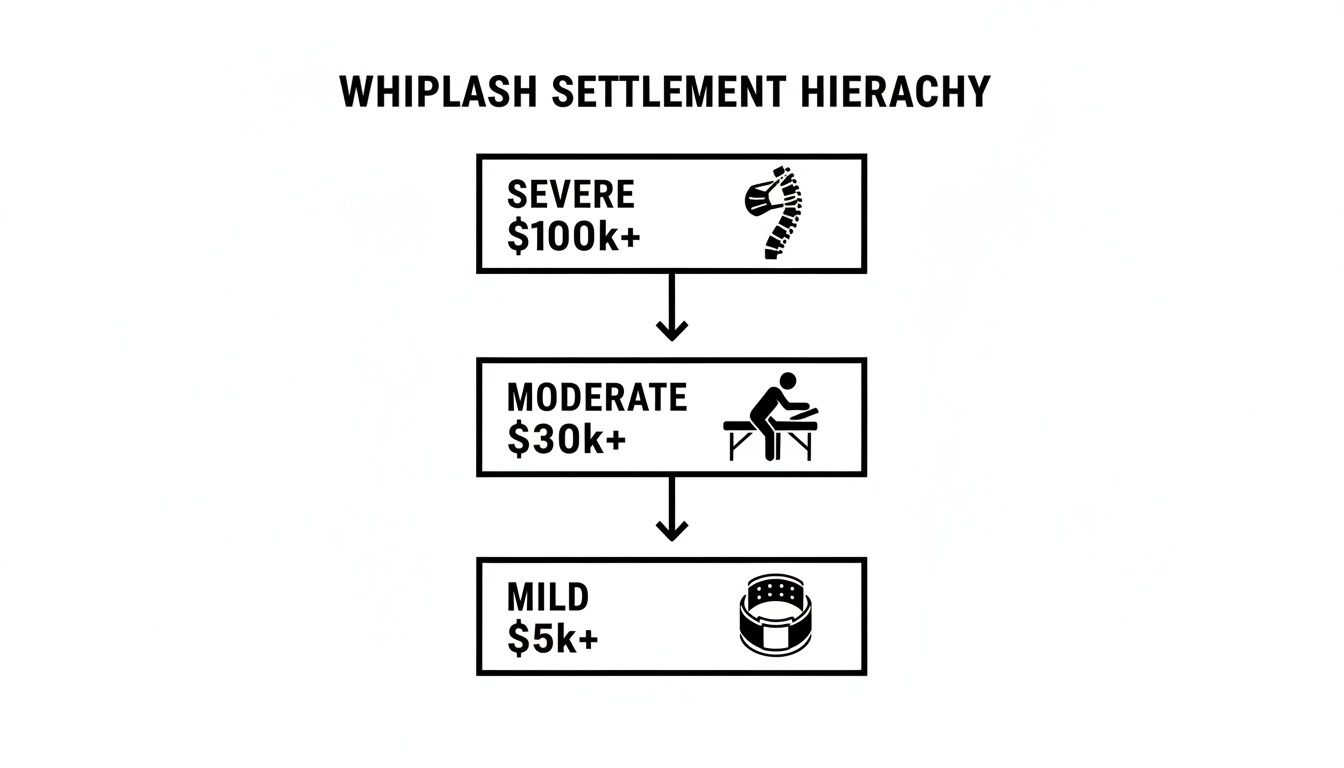

According to legal settlement data, the average whiplash settlement can range from $72,500 to over $1,008,258, depending on how bad the injury is.

- Payouts for mild cases with limited therapy often land between $5,000 and $15,000.

- Moderate injuries that need ongoing physical therapy can push settlements into the $30,000 to $75,000 range, which better accounts for lost wages and daily struggles.

- When whiplash causes severe complications like nerve damage or herniated discs requiring surgery, the figures can climb past $100,000, with some reaching $300,000 or more.

You can dig deeper into these figures and see how they're determined by reviewing whiplash compensation data from The Injury Lawyers.

Real-World Examples of Whiplash Cases

Let's put these numbers into context with a few real-world scenarios you might see right here on Texas roads:

-

Mild Whiplash Example: You're stopped at a red light in a Dallas suburb when you get lightly rear-ended. The next day, you feel some neck stiffness and see a doctor, who suggests a few weeks of chiropractic care. You don't miss any work. In a case like this, your settlement would likely cover your medical bills plus a small amount for your discomfort, probably falling into that lower settlement range.

-

Moderate Whiplash Example: A driver T-bones you at an intersection in Austin, causing significant neck and shoulder pain. Your doctor diagnoses a more serious sprain and puts you on a six-month physical therapy plan. You have to burn through your sick days and even miss out on a promotion at work because of the constant appointments and nagging pain. Your settlement needs to cover all your medical costs, your lost income, and the serious disruption to your career and daily life. This is where compensation can easily reach the tens of thousands.

-

Severe Whiplash Example: You are hit by a commercial truck on a major highway in San Antonio. The impact is violent, causing a herniated disc in your neck that presses on a nerve, leading to numbness down your arm and chronic, debilitating pain. You end up needing surgery and are told you might never be able to go back to your physically demanding job. This type of catastrophic injury demands a settlement that accounts for past and future medical care, a permanent loss of earning capacity, and immense pain and suffering.

The key takeaway is this: the more your injury disrupts your life—physically, financially, and emotionally—the higher your potential settlement value. This is why meticulous documentation is absolutely critical.

These examples show how the specific details of your accident and injury are what truly matter. An experienced Texas injury attorney at The Law Office of Bryan Fagan can help you gather the necessary medical records, expert opinions, and financial documents to build a case that accurately reflects your total losses. These figures also show how important it is to understand the full extent of your non-economic damages. Our team can help you learn more about how to calculate your pain and suffering damages to ensure your settlement is fair.

Key Factors Influencing Your Whiplash Settlement

When an insurance company starts evaluating your claim, they don't just pull a number out of thin air. The final value of your settlement for whiplash is built piece by piece, using evidence that shows exactly how this injury has turned your life upside down. Legally, these impacts are sorted into two buckets: economic damages and non-economic damages.

Think of it like building a case. Your economic damages are the hard, measurable facts—the foundation. Your non-economic damages are the human story—the pain, frustration, and loss of quality of life. To get a fair settlement, you have to prove both.

Economic Damages: The Tangible Financial Losses

Economic damages are the most straightforward part of any whiplash claim. These are the direct, out-of-pocket costs you've racked up because of the accident. You can prove them with bills, receipts, and pay stubs.

Your attorney’s job is to help you track down and document every single expense, which usually includes:

- Medical Bills: This covers it all—from the ambulance ride and ER visit to ongoing physical therapy, chiropractic adjustments, prescriptions, and any future medical care your doctor says you'll need.

- Lost Wages: If whiplash kept you out of work, you’re entitled to be paid back for every dollar of income you lost while you were recovering.

- Diminished Earning Capacity: This is a huge factor in more serious cases. If your injury permanently impacts your ability to do your job or forces you into a lower-paying role, your settlement has to account for this future loss of income.

This chart gives you a good visual of how settlement values often line up with the severity of the injury and the medical care required.

As you can see, a severe diagnosis that requires something like surgery is going to command a much higher settlement than a minor strain that just needs a few weeks of rest.

Non-Economic Damages: The Personal Impact

While it’s easy to add up medical bills and lost paychecks, the real toll of whiplash often lies in the harm you can’t put a price tag on. Non-economic damages are designed to compensate you for the personal, human cost of your injury.

These damages are more subjective, but they are just as real and compensable under Texas law. They include things like:

- Pain and Suffering: This accounts for the physical pain, chronic discomfort, and emotional distress you've been forced to live with since the crash.

- Mental Anguish: This can be anything from anxiety and depression to a genuine fear of driving or even PTSD that stems directly from the trauma of the accident.

- Loss of Enjoyment of Life: If your injury stops you from playing with your kids, enjoying your hobbies, or participating in activities you once loved, you deserve to be compensated for that loss.

Really understanding the full scope of whiplash injuries is crucial for assessing what your case is truly worth. The more evidence you can provide to show how your day-to-day life has been negatively affected, the stronger your argument for significant non-economic damages will be.

A Real-World Example: Calculating Total Damages

Let’s imagine a Dallas rideshare driver who gets rear-ended on the job. The whiplash is bad enough that he can't turn his head without sharp pain, making it impossible for him to drive safely for three months.

- His economic damages would include the ER bill, his weekly physical therapy sessions, and the $10,000+ in income he lost from being unable to work.

- His non-economic damages would cover the constant pain that kept him from coaching his son's baseball team and the new anxiety he feels every time he gets behind the wheel.

A skilled Texas injury lawyer would add all of these pieces together to demand a total settlement that truly reflects everything he’s lost.

Who Is Liable for My Whiplash Injury?

Beyond damages, a couple of other practical realities will heavily influence your final compensation: proving fault and dealing with insurance policy limits.

Liability is just the legal word for fault. Before you can recover a dime, you have to prove the other driver’s negligence caused the accident.

In Texas, having clear proof—like a police report, witness statements, or traffic camera footage—is everything. On top of that, the at-fault driver's insurance policy has a maximum payout limit, which can act as a ceiling on what the insurer will pay. An experienced Houston car accident lawyer knows how to investigate all available insurance policies to find every possible source of recovery and maximize what you can get.

How Texas Law Impacts Your Whiplash Claim

Getting what you deserve for a whiplash injury isn't just about adding up your medical bills. It’s also about understanding how Texas law shapes your case from day one. A few key state-specific rules can make or break your claim, directly impacting how much compensation you can actually recover.

An experienced Texas injury lawyer does more than just file paperwork; they navigate these legal minefields for you, making sure your rights are protected every step of the way.

One of the most unforgiving rules is the statute of limitations. In plain English, this is a strict deadline for filing a lawsuit. In Texas, you have just two years from the date of the accident to file. If you miss that window, your right to seek compensation is almost certainly gone forever, no matter how clear the other driver’s fault was.

That two-year clock is always ticking. The longer you wait, the more evidence disappears, memories fade, and the easier it is for the insurance company to argue your injuries weren't that serious to begin with.

Texas Proportionate Responsibility Rule

Another critical piece of the puzzle is what Texas calls “proportionate responsibility.” You might have heard it called comparative fault. You can find it in Chapter 33 of the Texas Civil Practice & Remedies Code, and it deals with situations where more than one person shares the blame for a crash.

Think of it like a pie chart of fault. If a jury decides you were partially responsible for the accident, your final settlement gets reduced by your percentage of blame.

For example, let’s say you’re in a T-bone crash in San Antonio. An investigation shows the other driver was 90% at fault for blowing through a red light, but you were 10% at fault for being momentarily distracted. If your total damages add up to $50,000, your final award would be cut by 10% ($5,000), leaving you with $45,000.

But here’s the most important part. Under the Texas 51% Bar Rule, if you are found to be 51% or more at fault, you get nothing. Zero. Insurance adjusters know this rule inside and out, and they will use any excuse they can find to shift blame onto you to either slash their payout or deny your claim entirely.

Uninsured and Underinsured Motorist Issues

What happens if the person who hit you has no insurance or just the bare-minimum policy that won’t cover your medical bills? It’s a terrifyingly common problem on Texas roads.

Fortunately, your own auto insurance policy might be your safety net. This is where Uninsured/Underinsured Motorist (UM/UIM) coverage comes in.

Filing a UM/UIM claim means you’re now negotiating with your own insurance company. You might think they'd be on your side, but at the end of the day, they are still a business trying to protect their bottom line. A skilled Texas injury attorney can step in and manage this process, making sure your own insurer treats you fairly and pays you the benefits you've been paying premiums for.

Keeping Up with Settlement Trends

The legal world doesn't stand still, and neither do settlement values. We're seeing whiplash payouts climb, driven by inflation, skyrocketing medical costs, and a growing understanding of just how debilitating these injuries can be. Chronic pain, cognitive issues, and other long-term effects are finally being taken more seriously.

Globally, whiplash settlements often fall between $10,000 and $100,000, but severe cases involving other neck and back injuries can go much higher. You can learn more about recent whiplash settlement amount figures from Meyers Injury Law to see how these numbers are broken down. Staying on top of these trends is crucial. It allows your lawyer to fight for a settlement that reflects the real-world costs of today, not what was considered fair five years ago.

Steps to Take to Protect Your Whiplash Claim

The chaos after a car crash is disorienting. Your head is spinning, adrenaline is pumping, and it's hard to think straight. But what you do in those first few moments and days is absolutely critical to protecting your right to fair compensation.

Building a strong whiplash claim isn't something that happens overnight. It starts at the scene of the accident. Think of every step you take—calling the police, taking a photo, seeing a doctor—as laying another brick in the foundation of your case. Each one helps prove your story and document exactly what you've lost.

Step 1: Seek Prompt Medical Attention

This is, without a doubt, the single most important thing you can do. Even if you think you feel fine, you need to see a doctor right away. The adrenaline rush from a collision is powerful and can easily mask the pain of a whiplash injury, which often takes hours or even days to fully set in.

Putting off medical care is one of the biggest mistakes we see people make. Insurance adjusters will jump on any delay, arguing that if you weren't hurt badly enough to see a doctor immediately, your injuries must not be serious. A prompt medical evaluation creates an official record that directly connects your neck pain to the accident.

Step 2: Document Everything at the Scene

If you're physically able to, start documenting everything you can. Your smartphone is your best friend in this situation.

Use it to:

- Take Photos and Videos: Get pictures of the damage to both cars from every angle. Don’t forget to photograph the wider scene, including any skid marks, traffic signals, and even the weather conditions.

- Gather Information: Swap names, phone numbers, and insurance details with the other driver. Just as important, get the names and numbers of anyone who witnessed the crash.

- Wait for the Police: Always call 911. The official police report is a vital piece of evidence. It provides an objective account of what happened and is often the first thing an insurance company looks at to determine liability.

Step 3: Be Cautious When Speaking to Insurance Adjusters

It won’t be long before the other driver's insurance adjuster calls you. Remember, this person is not on your side. Their goal is simple: protect their company's bottom line by paying you as little as possible—or nothing at all.

Here’s what you need to keep in mind:

- Stick to the Facts: Only give them the basics, like your name and where the accident happened. Don't go into detail about your injuries or speculate on who was at fault.

- Decline a Recorded Statement: You are under no obligation to give them a recorded statement. Adjusters are trained to ask tricky, leading questions to get you to say something that they can twist and use against you later.

- Never Accept a Quick Offer: Insurance companies love to dangle a lowball offer early on. They're hoping you'll be tempted by fast cash before you even know how serious your injuries are or how much treatment you'll need.

The best thing you can say is to politely decline to discuss the details and tell the adjuster that your Houston car accident lawyer will be in touch. That simple sentence stops them in their tracks, protects you, and shows them you mean business. Speaking with an attorney first is the smartest way to protect your right to a full and fair settlement for whiplash.

Why You Need a Houston Whiplash Injury Lawyer

After a car crash, it's tempting to think the at-fault driver's insurance company will step up and do the right thing. But you have to remember who they really work for. Insurance companies are businesses, and their number one goal is protecting their bottom line—which means paying you as little as possible.

They have a playbook for whiplash claims. Adjusters will often try to downplay your injury, calling it "minor" or "temporary" to justify a lowball settlement offer. This is where having an experienced Houston car accident lawyer on your side changes everything.

At The Law Office of Bryan Fagan, we level the playing field. We’ve seen these tactics countless times, and our job is to make sure they don’t get away with undervaluing your pain and suffering.

We Build Your Case for Maximum Value

We don't just take the insurance company's word for it. From the moment you hire us, we launch our own independent investigation to build the strongest case possible.

This isn't just paperwork; it's a strategic process that involves:

- Digging for Evidence: We go beyond the initial police report. We track down witnesses, analyze photos from the scene, and piece together exactly what happened to establish clear liability.

- Working with Medical Experts: Whiplash is more than just a sore neck. We consult with doctors and specialists who understand the long-term impact of these injuries. Their testimony helps us prove the full cost of your care—not just today's bills, but any future treatment you might need.

- Calculating Every Single Loss: Your claim is about more than medical expenses. We meticulously document everything you've lost, from missed paychecks and reduced earning ability to the daily physical pain and emotional toll the accident has taken on your life.

We take over all communication with the insurer. You won’t have to deal with another phone call, email, or negotiation tactic. Our attorneys are tough negotiators, but we're always prepared to take your fight to court if the insurance company refuses to offer a fair settlement.

No Win, No Fee Guarantee

The last thing you need to worry about after an accident is how you’re going to afford a lawyer. That’s why we handle all our personal injury cases on a contingency-fee basis.

What does that mean for you? It’s simple: you pay us nothing unless we win your case. There are no upfront costs and no hidden fees. Our payment is a percentage of the settlement we secure on your behalf.

This arrangement removes all financial risk, so you can focus entirely on getting better. It also means our goals are perfectly aligned with yours—we are deeply motivated to get you the maximum compensation possible.

It's helpful to understand what a claim could be worth. Globally, as regulations evolve, many soft-tissue whiplash settlements fall between $5,000 to $25,000. However, with solid medical evidence, these numbers can climb significantly. Average insurance payouts often reach $12,000-$30,000 and can surge past $100,000 for severe, well-documented cases. You can see how global trends are shaping these claims on Clyde & Co..

To learn more about how our fees work, check out our detailed guide on how much lawyers take from a settlement.

Common Questions About Whiplash Settlements in Texas

When you're dealing with the pain and shock of a whiplash injury, the last thing you want to worry about is a complicated legal process. It’s completely normal to have questions about what comes next. Getting clear, straightforward answers can help you feel like you’re back in control.

Let’s walk through some of the most common questions our clients ask about getting a fair settlement for whiplash in Texas. Our goal is to cut through the legal jargon and give you the confidence you need to move forward.

How Long Does a Whiplash Settlement Take in Texas?

This is usually the first question people ask, and the honest answer is: it really depends. There's no one-size-fits-all timeline. A straightforward claim, where the other driver is clearly at fault and your injuries are minor, might wrap up in just a few months.

However, many cases aren't that simple. Several things can extend the timeline:

- How serious are your injuries? If you need ongoing medical care, it's crucial to wait until you've reached "maximum medical improvement." Settling too early means you could be left paying for future treatments out of your own pocket.

- Is there a fight over fault? If the insurance company tries to pin some of the blame on you, it takes time to gather the evidence needed to set the record straight.

- Do we need to file a lawsuit? If an insurer digs in their heels and refuses to make a fair offer, filing a lawsuit is the next step. While this doesn't guarantee a trial, it can lengthen the process to a year or more.

Do I Have to Go to Court for a Whiplash Settlement?

Most people picture a dramatic courtroom scene, and the thought of testifying is stressful. Here’s the good news: the overwhelming majority of personal injury cases—well over 90% of them—are settled long before a trial ever happens.

A settlement is just a formal agreement worked out between your lawyer and the insurance company. Filing a lawsuit is often a strategic move to show the insurer that you're serious. More often than not, that's all it takes to bring them back to the negotiating table with a much more reasonable offer.

Can I Still File a Claim If I Had a Pre-existing Neck Condition?

Yes, absolutely. This is a huge source of anxiety for many clients, and it's a tactic insurance adjusters love to use to try and deny a claim or lowball an offer. But Texas law is on your side.

The "eggshell skull" rule is a legal principle that says the at-fault party is responsible for the harm they caused, even if you were more vulnerable to injury than the average person. If the crash made a previous condition worse, you have the right to recover damages for that new level of pain and suffering.

The key here is solid medical documentation. Your doctor needs to clearly show how the accident aggravated or worsened your pre-existing condition.

What If the Other Driver Was Uninsured?

That moment when you realize the at-fault driver has no insurance is incredibly frustrating. It can feel like you've hit a dead end, but you may still have options.

This is exactly what Uninsured/Underinsured Motorist (UM/UIM) coverage on your own auto policy is for. An experienced Houston car accident lawyer can dig into your policy, figure out your coverage, and help you file a claim with your own insurance company to cover your medical bills and other losses.

The path to recovery after a car accident can feel overwhelming, but you don't have to walk it alone. Understanding your rights is the first step toward getting the justice and compensation you deserve. The dedicated attorneys at The Law Office of Bryan Fagan, PLLC, are here to handle the legal heavy lifting so you can focus on what truly matters: getting better.

If you've been injured, don't wait to get the help you need. Contact us today for a free, no-obligation consultation to talk about your case. Let us fight for you. Visit us at https://houstonaccidentlawyers.net.