A car crash can change your life in seconds—but you don’t have to face recovery alone. The moments after a collision are confusing and overwhelming, and one of the most urgent questions is always, "How am I going to pay for my medical care?" The good news is that your health insurance can—and absolutely should—be used to pay for your treatment right away.

Using your own health plan from day one ensures you get the care you need without waiting for the other driver's insurance company to accept responsibility, a process that can drag on for months. It's a critical first step that protects both your physical and financial health.

Who Is Liable in a Texas Car Accident?

While your own insurance policies provide immediate help, your financial recovery ultimately depends on one question: who was at fault for the crash? In Texas, proving the other driver’s liability is how you hold them legally and financially accountable for the harm they caused.

Liability is a legal term that means responsibility. To establish it, you must prove the other driver was negligent. Simply put, negligence is the failure to use reasonable care to keep others safe. A driver who is texting, speeding, or running a red light is being negligent.

Understanding Texas Negligence and Comparative Fault

Texas operates under a legal rule called modified comparative fault, often known as the “51% bar rule.” This law, found in the Texas Civil Practice & Remedies Code (Chapter 33), is crucial because it determines if you can recover money and how much you can receive.

Here’s how it works in plain English:

- Liability: The legal responsibility for an accident. If another driver is liable, their insurance must pay for your losses.

- Comparative Fault: A rule that assigns a percentage of blame to each person involved in an accident.

- The 51% Rule: You can recover financial compensation (known as damages) as long as you are 50% or less at fault. However, your final award will be reduced by your percentage of fault. If you are found to be 51% or more at fault, you are barred from recovering any money at all.

For example, imagine a Houston driver T-bones you at an intersection on I-45. They clearly ran a stop sign, but evidence shows you were driving five miles per hour over the speed limit. A jury might decide the other driver was 90% at fault, but you were 10% at fault. If your total damages were $100,000, your award would be reduced by your 10% share, and you would receive $90,000.

This is why the other driver's insurance company will fight to shift even a tiny bit of blame onto you. An experienced Houston car accident lawyer knows how to build a strong case with police reports, photos, and witness statements to prove the other driver’s liability and protect your right to full compensation.

Steps to Take After a Crash to Protect Your Rights

The actions you take in the minutes and days after a car wreck can have a huge impact on your health and your ability to file a successful auto insurance claim. Here is some practical, step-by-step advice for accident victims.

Your First Step: Use Your Health Insurance for Medical Care

Always give your health insurance card to the staff at the emergency room or urgent care clinic. This simple act allows the hospital to bill your provider directly, stopping a flood of intimidating medical bills from landing on your doorstep.

Putting off medical treatment because you're worried about who will pay is a serious mistake. It can harm your health and weaken your personal injury claim. Insurance adjusters love to argue that if you didn't see a doctor right away, your injuries must not have been that serious.

Using your health plan accomplishes several critical goals:

- It gives you immediate access to medical care. You can see doctors, get the scans and tests you need, and start treatment without delay.

- It prevents medical debt. This keeps bills from piling up and being sent to collections while your car accident claim is still being sorted out.

- It documents your injuries. A clear, immediate medical record is powerful evidence when it comes time to prove the extent of your harm.

Remember, even though your health plan pays upfront, the person who caused the crash is still legally responsible for your damages—the legal term for all the losses you suffered, including medical costs. A Texas injury attorney will work to make sure the at-fault driver's insurance ultimately reimburses every penny. You can learn more in our detailed guide on who pays medical bills after a Texas car accident.

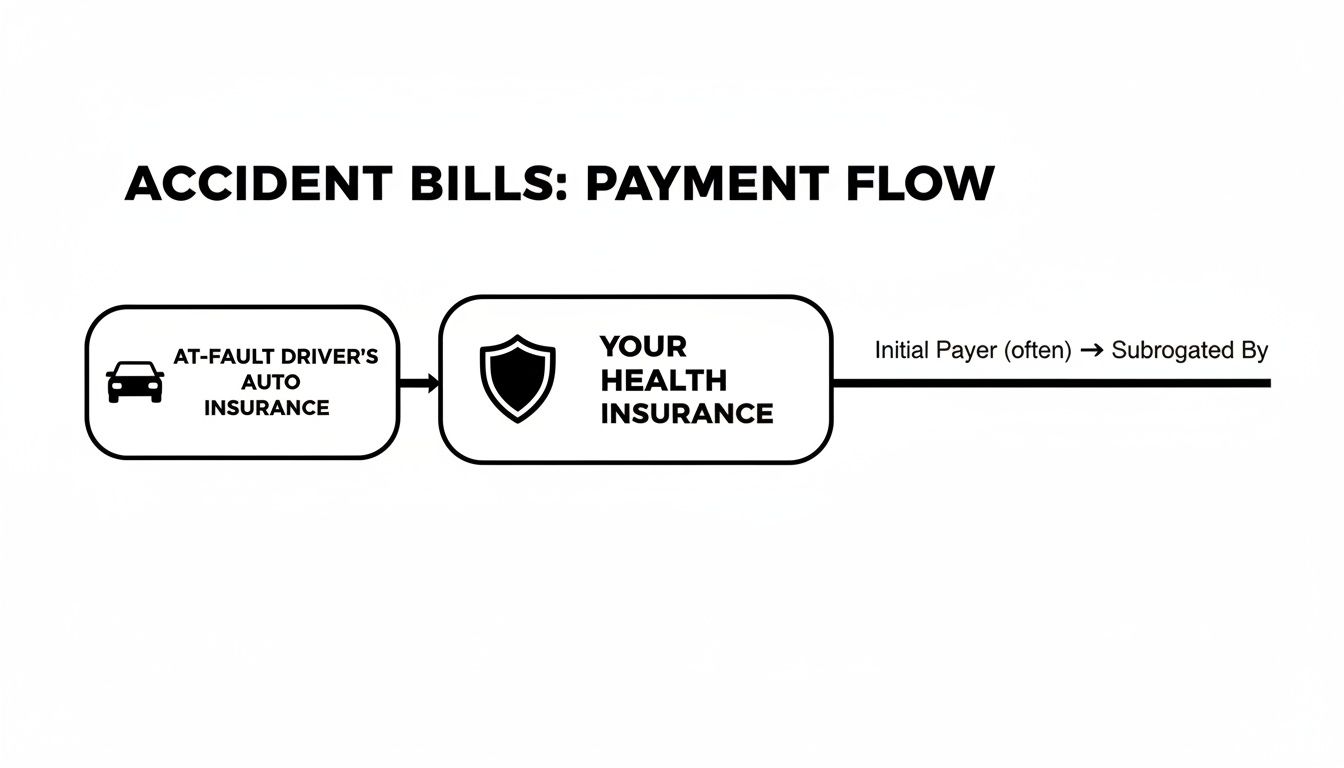

How Different Insurance Policies Work Together

Figuring out which insurance pays for what can feel like a puzzle. You have your health insurance, the other driver's auto policy, and your own car insurance—all with different rules. Here’s how they fit together.

| Insurance Type | Who Pays Initially | Who Is Ultimately Responsible |

|---|---|---|

| Health Insurance | Your health insurance company. | The at-fault driver's auto insurance. |

| MedPay/PIP (Auto) | Your own auto insurance company. | The at-fault driver's auto insurance. |

| At-Fault Driver's Liability | No one—you must wait for the claim to settle. | The at-fault driver's auto insurance. |

As you can see, relying on the other driver's insurance to pay bills as they come in isn't an option. Using your own health insurance is the key to getting the care you need without financial stress.

Filing a Claim: Navigating the Insurance Maze

After getting medical care, the next step is dealing with the insurance companies. This process involves your own auto policy, your health insurer, and the at-fault driver's liability coverage. Understanding their roles is crucial.

Your First Line of Defense: PIP and MedPay

Right after an accident, the first place you should look for help is your own auto insurance policy. Two types of coverage act as your financial first responders: Personal Injury Protection (PIP) and Medical Payments (MedPay).

- Personal Injury Protection (PIP): This is standard coverage in Texas unless you reject it in writing. PIP is incredibly helpful because it covers your medical bills and a portion of your lost wages, no matter who was at fault.

- Medical Payments (MedPay): This is an optional add-on that also pays for medical care for you and your passengers, regardless of who caused the crash. You can learn more in our guide on what is Medical Payments coverage.

Using PIP or MedPay first is a smart move—it can help cover your health insurance deductibles and copays, which means less money coming out of your pocket right away.

The Role of Health Insurance as a Bridge

Your health insurance acts as a vital financial bridge, covering your medical bills while your Houston car accident lawyer builds the case against the at-fault driver. Without it, you could face overwhelming medical debt while you wait months for a settlement.

Think of it like this: your health insurance steps in to make sure you get the care you need now, and the at-fault driver’s insurance pays them back later when your case settles.

This process ensures your treatment isn't delayed just because the legal fight is still ongoing.

The Safety Net: Uninsured/Underinsured Motorist Coverage

What happens if the driver who hit you has no insurance or not enough to cover your bills? This is where Uninsured/Underinsured Motorist (UM/UIM) coverage on your own auto policy becomes a lifesaver.

If the at-fault driver is uninsured, your UM coverage steps in to pay for your damages. If they are insured but their policy limits aren't high enough to cover your total losses, your UIM coverage makes up the difference. Having this coverage is essential for protecting your family from financial disaster after a serious crash, which can be critical if a loved one needs wrongful death compensation.

Understanding Subrogation: Why Your Health Insurer Wants Its Money Back

After a serious wreck, you might get a letter from your health insurance company that uses a legal term you’ve never seen before: subrogation. It sounds intimidating, but it’s a simple concept you must understand.

Think of it this way: your health insurance company paid your urgent medical bills after the crash. But once you get a settlement from the at-fault driver's insurance, your health insurer has a legal right to be paid back for the money they fronted you. That is subrogation.

How Subrogation Affects Your Settlement

Your health insurer will send a "notice of lien" to the at-fault driver's insurance company, staking a legal claim to a piece of your future settlement.

Here’s what that means for you:

- You Cannot Ignore It: This is a legal right. If you disregard the claim, your health insurer can sue you directly.

- It Comes Out of Your Settlement: The subrogation amount is paid directly from your total settlement. If your settlement is $100,000 and your health plan paid $30,000 in bills, that $30,000 must be repaid.

- It Is Negotiable: This is the most critical part. A skilled Houston car accident lawyer can—and should—negotiate to reduce that amount.

An experienced attorney knows the legal arguments to slash a subrogation claim. Successfully reducing this amount means more of the settlement money stays where it belongs—in your pocket. This negotiation is a standard part of our service and can make a huge difference in your financial outcome.

Navigating Hospital Liens and Protecting Your Settlement

Another financial roadblock that can appear is a hospital lien. This is a legal claim a hospital can file directly against your future personal injury settlement to ensure they get paid first. This is different from subrogation; it’s a claim filed by the hospital itself.

Why Hospital Liens Can Be So Aggressive

Under Texas law, hospitals have the right to file these liens. The problem is, they often bill at a much higher "chargemaster" rate than they would ever accept from a health insurance company. This inflated billing can gut your settlement. For example, a hospital might send a bill for $30,000 for services an insurance company would have paid just $8,000 for.

The consequences for uninsured victims can be devastating. Research shows that crash victims without health insurance face a 37% to 59% higher odds of dying from their injuries compared to those with coverage. This grim statistic shows health insurance isn't just about bills; it’s a critical lifeline. You can read the full research about these injury outcomes to learn more.

How a Lawyer Fights Back to Protect Your Money

The good news is you don't have to accept a hospital lien at face value. A Texas injury attorney can challenge these aggressive claims.

At The Law Office of Bryan Fagan, PLLC, we take these steps:

- Verify the Lien’s Validity: We ensure the hospital followed every legal requirement. If they made a mistake, the lien could be invalid.

- Audit the Bills: We meticulously review every line item for unreasonable or duplicate charges.

- Negotiate from a Position of Strength: We fight to reduce the lien amount significantly, sometimes by more than half.

A hospital lien is a demand, not a final verdict. Our job is to ensure the hospital accepts a fair payment, which leaves more of your hard-won settlement in your hands. For more details on protecting your financial recovery, review this guide on maximizing an auto accident settlement.

Why You Need a Lawyer to Handle Insurance Negotiations

Trying to deal with insurance companies after a crash can feel like a full-time job you never asked for. An experienced Texas personal injury lawyer is your most critical advocate, lifting that administrative and emotional weight off your shoulders. We handle every phone call, email, and letter so you can focus on getting better.

We get to work immediately, building a powerful claim backed by solid evidence—police reports, witness statements, and medical records—to prove the other driver's liability.

Fighting for the Full Value of Your Claim

Insurance adjusters are skilled negotiators whose job is to pay out as little as possible. Having a lawyer on your side levels that playing field. We start by meticulously calculating all of your damages, the legal term for your total losses.

A complete damages claim under Texas law (Texas Civil Practice & Remedies Code, Chapter 41) must account for:

- All past and future medical costs, from the ER visit to physical therapy and medications.

- Lost wages and any impact the injury has on your future earning ability.

- Pain and suffering, which is real compensation for the physical and emotional trauma you’ve endured.

- Property damage to your vehicle.

We bundle this evidence into a formal package to demand fair payment. For those interested, there are great resources that explain how to write an insurance demand letter, a key step in these negotiations.

Protecting Your Settlement from Liens and Subrogation

One of the most valuable things an attorney does is manage the tangled web of subrogation and hospital liens. We actively negotiate with your health insurer and medical providers to reduce the amount you have to pay them back. This step alone can dramatically increase the money you get to keep. To learn more about our approach, check out our guide on how to negotiate an insurance settlement.

Answering Your Top Questions About Health Insurance After a Wreck

The chaos after a car crash is overwhelming. Here are some clear, straightforward answers to the questions we hear most often from families like yours.

Should I Give the Hospital My Health Insurance Information?

Yes, absolutely. Always give the hospital or clinic your health insurance card right away. It’s the quickest path to getting your bills paid and ensuring you get the care you need without interruption. Using your health insurance protects you financially while your personal injury lawyer focuses on holding the other driver accountable.

What if My Health Insurance Company Denies the Claim?

While uncommon, it can happen. Sometimes a health insurer denies a claim because they are confused about who should pay first. If this happens, don't panic—call a car accident attorney immediately. An experienced lawyer can contact your insurer, clarify their legal duty to cover your care, and ensure your treatment continues while they pursue the auto insurer.

Can I Get My Deductible and Co-pays Back?

Yes. Every penny you spend out of pocket on medical care is part of your legal damages. That includes your health insurance deductible, co-pays for doctor visits, and prescription costs. Your attorney will carefully track these expenses and demand that the at-fault party’s insurance reimburse you for them as part of your total settlement. Keep every bill and receipt.

What Is the Deadline for a Car Accident Claim in Texas?

In Texas, the law that sets a firm deadline for filing a lawsuit is called the statute of limitations. For most car accident claims, you have just two years from the date of the crash to file your case in court.

If you miss that two-year window, you will almost certainly lose your right to seek compensation forever. It is one of the harshest rules in the legal system. That’s why it is so important to contact an attorney as soon as possible after an accident to protect your rights.

A serious car accident can make you feel powerless, but you have the right to demand justice and fair compensation. The experienced and compassionate team at The Law Office of Bryan Fagan, PLLC is here to take on the insurance companies for you. Let us handle the legal fight so you can focus on what’s most important—your recovery. We are here to inform, reassure, and empower you every step of the way.

Contact us today for a free, no-obligation consultation to talk about your case and learn how a dedicated Texas injury attorney can help you and your family. https://houstonaccidentlawyers.net