Skip to content

Skip to content

A car crash can change your life in seconds — but you don’t have to face recovery alone. If you've been hurt in a car wreck in Texas, one of the first questions on your mind is probably, "How much is my settlement actually worth?" It's a fair question, but the honest answer is: there's no magic number.

A car accident settlement isn't a prize you win; it's a calculated value based on everything you've lost. While you might see national averages floating around—some suggest around $37,000 for moderate injuries—the real amount could be anywhere from a few thousand to millions of dollars. It all depends on the severity of the crash and the ripple effect it has on your life.

What Is a Typical Car Accident Settlement in Texas?

A crash can flip your world upside down in a matter of seconds. Suddenly, you're dealing with physical pain, emotional trauma, and a stack of bills that keeps growing. The stress is immense, and you need to know what kind of financial recovery is possible.

The truth is, there's no "typical" settlement because every single case is unique. For example, a Houston driver rear-ended on I-45 with minor whiplash will have a very different case than someone who suffered a traumatic brain injury in a multi-car pileup. Your story, your injuries, and your losses are what matter, not some generic average.

National Averages vs. Your Reality

Statistics can give you a ballpark idea, but they don't tell your story. Recent data from thousands of cases puts the average U.S. car accident settlement at $37,248.62. That number often reflects claims for less severe injuries, like whiplash, where settlements might fall in the $10,000 to $15,000 range to cover some basic medical care and a few missed paychecks. You can explore more personal injury settlement examples to see how widely these amounts can vary.

But a statistic can't possibly capture the true cost of a life-altering injury. Your claim's value isn't based on an average; it's built piece by piece from your personal losses.

A fair settlement is not a lottery win. It is a calculated recovery designed to restore the financial, physical, and emotional stability that was taken from you. The goal is to make you "whole" again in the eyes of the law.

The Core Components of Your Claim

To figure out what your case might be worth, you have to break it down into its core components. These are the building blocks that an experienced Texas injury attorney uses to construct a powerful case and demand fair compensation from the insurance company.

Here’s a look at the key factors insurance adjusters and lawyers use to calculate the value of a car accident claim.

Key Factors That Shape Your Settlement Amount

| Influencing Factor | How It Affects Your Settlement | Example |

|---|---|---|

| Medical Bills | This includes every single medical cost, past and future. The higher the bills, the higher the baseline value of your claim. | Ambulance ride, ER visit, surgeries, physical therapy, prescription medications, and even future care needs. |

| Lost Income | Covers wages you lost while out of work and any impact on your ability to earn in the future. | Pay stubs showing missed work, or an expert's projection of lost earning capacity if you can no longer do your old job. |

| Pain and Suffering | This compensates you for the non-economic damages—the physical pain and emotional distress you've endured. | Chronic pain, anxiety, PTSD, depression, or the loss of enjoyment of life resulting from the accident. |

These elements form the foundation of your claim. A skilled attorney knows how to document and argue for each one to ensure nothing is left on the table.

Understanding the Building Blocks of Your Claim

A fair settlement isn't just about covering your first emergency room bill. In Texas, the goal is to make you "whole" again. This means getting financial compensation for every single loss you've suffered because someone else was careless behind the wheel. To figure out what your settlement might be worth, we have to first break down these losses, which are legally known as damages.

Think of these damages as the individual building blocks of your claim. Each block represents a different type of loss you've experienced. When we stack them all together, they form the total value of your case. These blocks generally fall into two main categories: economic and non-economic damages.

Economic Damages: The Tangible Costs

Economic damages are the most straightforward part of your claim because they have a clear paper trail. These are the tangible, out-of-pocket expenses you can prove with receipts, bills, invoices, and pay stubs.

Your settlement should cover all of these costs—both what you've already paid and what you'll need in the future.

- Medical Expenses: This is everything related to your physical recovery. Think ambulance rides, hospital stays, surgeries, physical therapy, prescriptions, and any medical equipment you need.

- Future Medical Care: If your injuries require long-term treatment, like ongoing therapy or future surgeries, we need to account for those anticipated costs right now.

- Lost Wages: This covers the paychecks you missed while you were out of work and recovering.

- Loss of Earning Capacity: What if your injuries keep you from returning to your old job or limit your ability to earn a living down the road? You can seek compensation for that diminished earning potential.

- Property Damage: This is simply the cost to repair or replace your vehicle and any personal items, like a laptop or phone, that were destroyed in the crash.

Of course, before you can even think about the value of your claim, you need to know the immediate steps to take after a wreck. Learning what to do after a motor vehicle accident is crucial for protecting your rights from the very start.

Non-Economic Damages: The Human Impact

While economic damages add up your financial losses, non-economic damages are all about the profound, personal impact the accident has had on your life. These losses don't come with a price tag, but they are just as real and deserve just as much recognition in your settlement.

These intangible damages compensate you for the human cost of the crash—the suffering that goes far beyond bank statements and medical bills. A skilled Houston car accident lawyer knows how to demonstrate this suffering to an insurance company.

For example, imagine a driver is rear-ended on I-45 and suffers whiplash. The economic damages are easy to see: the ER visit and the chiropractor bills. But the non-economic damages account for the constant neck pain that keeps them from picking up their toddler, the new anxiety they feel every time they merge onto the freeway, and the loss of joy from being unable to play their weekend softball game.

Common types of non-economic damages in Texas include:

- Pain and Suffering: Compensation for the physical pain and discomfort you've had to endure.

- Mental Anguish: This covers the emotional toll—the fear, anxiety, depression, or even PTSD that follows a traumatic crash.

- Physical Impairment or Disfigurement: Compensation for permanent scars, the loss of a limb, or other lasting physical limitations.

- Loss of Consortium: If the injuries are catastrophic, a spouse may be able to claim damages for the loss of companionship, support, and intimacy.

- Loss of Enjoyment of Life: This addresses your inability to enjoy daily activities, hobbies, and life's simple pleasures the way you did before the crash.

Together, these economic and non-economic damages form the complete picture of your losses. An experienced Texas injury attorney at The Law Office of Bryan Fagan will meticulously document every single block to build the strongest possible foundation for your claim, ensuring no aspect of your suffering gets overlooked.

How Texas Laws Shape Your Settlement Value

Figuring out what a car accident settlement is worth in Texas isn't as simple as just adding up your medical bills. The final number is heavily influenced by state laws. These aren't just technicalities buried in law books; they have real-world power to either boost or slash the compensation you can actually receive.

An experienced Houston car accident lawyer understands how to navigate these rules. We use them to protect your rights and build a case that stands up to the insurance company’s tactics.

Texas Modified Comparative Fault Rule

The single most important law you need to know is Texas's modified comparative fault rule. In plain English, this rule addresses crashes where more than one person might share the blame. You can find it in Chapter 33 of the Texas Civil Practice & Remedies Code.

Here’s how it works: your potential settlement is reduced by your percentage of fault. If a jury decides you were 20% responsible for the accident, your total compensation award would be reduced by 20%.

But here's the critical part.

The law includes a strict 51% bar rule. If a jury or insurance adjuster decides you were 51% or more at fault, you are legally barred from recovering a single penny. It doesn't matter how severe your injuries are—your claim is worth zero.

This is why you have to fight back against any attempt to unfairly shift blame onto you. Insurance adjusters love using this rule to their advantage. They might argue you braked a split-second too late or didn't swerve fast enough—anything to assign you a small percentage of fault and reduce their payout. A skilled attorney will gather the evidence needed to prove the other driver's liability (their legal responsibility) and shut down these tactics.

The Two-Year Statute of Limitations

Another crucial Texas law is the statute of limitations. This is a hard deadline for taking legal action. For nearly all car accident claims in Texas, you have just two years from the date of the crash to file a personal injury lawsuit.

If you miss that two-year window, you lose your right to sue forever. The insurance company knows this. Once that deadline passes, they have no legal reason to offer you a fair settlement because you no longer have any leverage to force them to pay.

Two years might sound like a long time, but it disappears quickly when you're building a strong case. During that period, we need to:

- Investigate the crash thoroughly by collecting police reports, witness statements, and photos.

- Wait for you to finish medical treatment so we have a full picture of your injuries and future care needs.

- Gather all your medical records and bills to accurately calculate the financial damages.

- Negotiate with the insurance company in an attempt to settle before a lawsuit is even necessary.

Acting fast is key. Contacting a lawyer soon after the accident ensures that we can preserve critical evidence and protect your rights from day one.

Insurance Minimums and UM/UIM Coverage

Finally, the other driver's insurance coverage can cap what you recover. Texas law only requires drivers to carry a minimum of $30,000 in liability coverage for bodily injury per person. In any serious accident, your medical bills alone can blow past that number in a heartbeat.

This is where your own insurance policy can save the day. Uninsured/Underinsured Motorist (UM/UIM) coverage is an optional part of your policy that pays for your losses when the at-fault driver has no insurance or not enough to cover your damages. In cities like Houston or Dallas where hit-and-runs and uninsured drivers are all too common, having this protection can be the difference between a fair recovery and getting stuck with the bills.

If you've been hurt, our job is to explore every available insurance policy—including your own UM/UIM coverage—to find all possible sources of compensation and maximize your settlement.

Figuring Out What Your Settlement Might Be Worth

While only a seasoned Texas injury lawyer can pin down the true value of your claim, you can get a ballpark idea. Understanding the basic math helps you see how insurance companies and attorneys look at a case. It empowers you to know when an offer is fair and when it's just plain low.

One of the most common starting points is something called the multiplier method. This isn't a hard-and-fast legal rule, but it's a formula used across the industry to get a rough estimate of the "pain and suffering" part of a claim. It gives everyone a baseline number to work from, which can then be adjusted based on the specifics of what happened to you.

The Multiplier Method Explained

The formula itself is pretty straightforward. You begin by adding up all your concrete, provable financial losses—what we call economic damages. This includes every medical bill you've received, the cost of any future care you'll need, and every dollar of wages you've lost from being out of work.

Once you have that total, you multiply it by a number, usually somewhere between 1.5 and 5. This number is the "multiplier."

Economic Damages (Medical Bills + Lost Wages) x Multiplier (1.5 to 5) = Estimated Settlement Value

The real trick is picking the right multiplier. A lower number, like 1.5 or 2, is typically for less severe injuries that heal up without much fuss, like a minor whiplash case. A higher multiplier, like a 4 or 5, is reserved for catastrophic injuries—the kind that cause permanent disability, disfigurement, or a lifetime of chronic pain. A good lawyer's job is to fight for the highest possible multiplier your injuries justify.

A Real-World Calculation Example

Let's walk through how this works. Imagine a Houston driver gets T-boned in an intersection. The crash leaves them with a fractured leg that needs surgery and a long road of physical therapy.

Here’s a step-by-step look at how their lawyer might calculate an initial settlement demand:

Add Up the Economic Damages:

- Emergency Room Visit: $7,000

- Surgery Costs: $30,000

- Physical Therapy (8 weeks): $6,000

- Lost Wages (10 weeks): $12,000

- Total Economic Damages: $55,000

Choose the Right Multiplier: This was a serious injury. It required surgery and significantly disrupted their life with a painful recovery. A multiplier of 3 is a reasonable starting point.

Calculate the Estimated Value:

- $55,000 (Economic Damages) x 3 (Multiplier) = $165,000

In this scenario, an experienced attorney would likely open negotiations by demanding a settlement in the neighborhood of $165,000. This figure accounts for both the hard financial costs and the very real, though less tangible, pain and suffering the victim went through. To dive deeper into this specific part of the calculation, check out our guide on how to calculate pain and suffering damages.

Typical Settlement Payouts Can Vary Wildly

It's critical to understand that every case is different, and settlement amounts are all over the map. The table below gives a general idea of potential ranges, but these are just estimates.

Sample Settlement Ranges by Injury Severity

Illustrative settlement ranges for common car accident injuries in Texas. These are estimates and actual amounts vary based on case specifics.

| Injury Type | Common Settlement Range (Estimate) | Key Factors |

|---|---|---|

| Minor Soft Tissue Injuries (e.g., whiplash, strains) | $8,000 – $25,000 | Limited medical treatment, quick recovery, minimal lost work time. |

| Moderate Injuries (e.g., bone fractures, herniated disc) | $50,000 – $250,000 | Requires surgery or extensive physical therapy, significant lost wages, some lingering pain. |

| Severe Injuries (e.g., spinal cord injury, TBI) | $500,000 – $5,000,000+ | Permanent disability, requires lifelong medical care, loss of earning capacity, profound impact on quality of life. |

While a typical car accident settlement for minor to moderate injuries often falls between $8,200 and $30,000, severe cases can easily climb into the hundreds of thousands or even millions. For instance, one recent analysis found the average car accident settlement from 2021 to 2024 was $55,056, showing just how wide the spectrum is.

Ultimately, your final number will hinge on many things: how clear it is who was at fault, the insurance policy limits of the other driver, and just how strong the evidence is that your legal team puts together.

Steps to File Your Car Accident Claim

When you’re hurt in a crash, the medical bills start piling up while your paychecks stop coming in. It’s completely natural to wonder, "How long is this going to take?" Everyone wants to get their settlement money quickly, but the timeline can swing wildly depending on the details of your case.

A simple fender-bender with clear fault might wrap up in a few months. But for more serious crashes, you have to be patient. Rushing to take the first lowball offer from an insurance company is a huge mistake—it almost guarantees you'll leave money on the table that you desperately need.

Key Stages That Influence the Timeline

Getting a settlement isn't a single event; it's a process with several critical steps. Each one takes time to get right, and a delay in one area can push back the entire timeline. A deliberate, thorough approach is the only way to build a claim that the insurance company can't ignore.

Here’s a breakdown of the main stages:

- Investigation and Evidence Gathering: Right after the crash, we get to work collecting police reports, talking to witnesses, and gathering photos from the scene. Our goal is to lock down proof of liability from day one.

- Medical Treatment and Recovery: This is often the longest part of the journey. We can't know the true value of your claim until you’ve reached Maximum Medical Improvement (MMI). That’s the point where your doctor says you’re as recovered as you’re going to get. Only then can we understand the full, long-term cost of your injuries.

- Drafting the Demand Letter: Once we have the complete picture of your medical bills, lost wages, and future needs—your total damages—we put together a detailed demand package. This letter lays out our case and tells the insurance company exactly what they owe you.

- Negotiation with the Insurer: The adjuster will review our demand and come back with a counteroffer. It’s almost always far too low. This kicks off a back-and-forth negotiation that can take weeks or even months.

- Filing a Lawsuit: If the insurance company refuses to be reasonable, we won’t think twice about filing a lawsuit to protect your rights. In Texas, you only have a two-year statute of limitations, so we have to act decisively to hold the at-fault driver accountable.

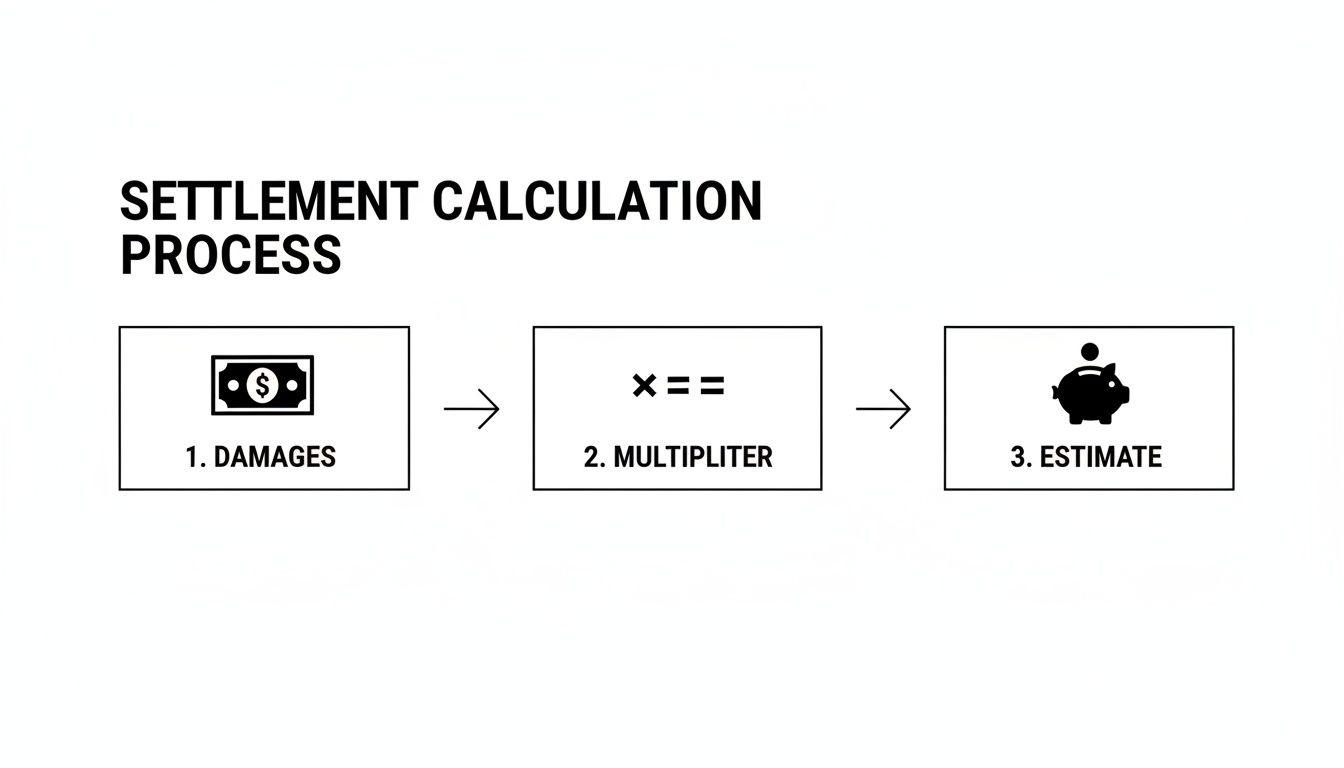

The infographic below gives you a clear picture of how we move from adding up your damages to landing on a final settlement number.

As you can see, everything starts with proving your damages. That number becomes the foundation for everything that follows.

How Injury Severity Affects the Wait

The single biggest factor that dictates your settlement timeline is how badly you were hurt. A serious injury means more treatment, a longer recovery, and a much more complicated calculation of what you’ll need for the rest of your life.

Think about it this way: a minor fender-bender in a parking lot might settle in 6 to 12 months. A more common rear-end collision on a Houston freeway could take 12 to 24 months. But a catastrophic T-bone or head-on collision that leaves you with permanent injuries? You could be looking at 24 to 36 months or even longer.

The more money that’s at stake, the harder the insurance company will fight to avoid paying. A complex case, like a multi-car pile-up on I-45 with everyone blaming each other, is going to take a lot longer than a straightforward crash where fault is obvious.

Waiting is frustrating, but it’s essential to getting the full and fair compensation you need to put your life back together. For a deeper look at what to expect, check out our detailed guide on the car accident settlement timeline. At The Law Office of Bryan Fagan, we’ll keep you in the loop every step of the way, making sure your case gets the attention and urgency it deserves.

Why a Texas Attorney Is Key to Maximizing Your Settlement

Trying to handle an insurance claim alone after a crash is like stepping into a professional negotiation without knowing the rules. Insurance companies have teams of adjusters and lawyers whose entire job is to protect their bottom line—which means paying you as little as they possibly can. An experienced Texas injury attorney completely levels that playing field, making sure your rights are protected from day one.

From the moment you hire The Law Office of Bryan Fagan, we take the entire burden off your shoulders. You can finally stop worrying about aggressive phone calls from adjusters and confusing paperwork. Your only job is to focus on your physical and emotional recovery. We’ll handle everything else.

We Are Your Advocates and Your Shield

Our role is to be your dedicated advocate, building a powerful case designed to secure the full and fair compensation you deserve. We get to work immediately on the critical tasks that strengthen your claim.

This includes:

- Conducting a Thorough Investigation: We dig deep to gather all crucial evidence—police reports, witness statements, photos of the scene, and more—to establish clear liability.

- Calculating Your Total Damages: We don't just add up your current medical bills and call it a day. We work with medical and financial experts to project your future care needs and lost earning capacity, making sure your settlement covers your long-term stability.

- Handling All Communications: We take over all contact with the insurance companies. This shields you from their pressure tactics and prevents you from accidentally saying something they could twist to devalue your claim.

- Negotiating from a Position of Strength: Our reputation as trial-ready attorneys sends a clear message: we won't accept a lowball offer. We negotiate aggressively for a settlement that truly reflects everything you’ve lost.

An experienced Houston car accident lawyer does more than just file paperwork; we build a strategic case that forces the insurance company to take your claim seriously and pay what is fair.

No Financial Risk to You

We understand that the last thing you need after a crash is another financial worry. That’s why we handle all car accident cases on a contingency fee basis. What does that mean for you? It means you pay absolutely nothing upfront. We cover all the costs of investigating and pursuing your claim.

Our fee is simply a percentage of the settlement we win for you. If we don’t secure a recovery on your behalf, you don’t owe us a dime. This arrangement removes all financial risk and allows you to access expert legal help when you need it most. You can learn more about how our fee structure works by reading our guide to auto accident attorney fees.

We are your partners in this fight, fully invested in achieving the best possible outcome for you and your family.

Still Have Questions? Here Are Some We Hear Every Day.

After a crash, your mind is probably racing with questions and uncertainty. It's completely normal. In this final section, we'll give you clear, straight-up answers to some of the most common concerns we hear from clients just like you. Our goal is to give you the information you need to move forward with confidence.

Will I Have to Go to Court for My Settlement?

The short answer is: probably not. The vast majority of car accident cases—well over 95% of them—are settled through direct negotiations with the insurance company, long before a courtroom ever comes into the picture. A good Houston car accident lawyer's primary goal is to get you a full and fair settlement as efficiently as possible.

But here’s the thing: if an insurer refuses to offer what your claim is truly worth, we are always prepared to file a lawsuit and fight for you at trial. Often, just knowing we're trial-tested attorneys who won't back down is enough to bring the insurance company back to the table with a much more reasonable offer.

With Medical Bills Piling Up, How Can I Possibly Afford a Lawyer?

We get it. The last thing you need after an accident is another bill to worry about. That’s exactly why The Law Office of Bryan Fagan works on a contingency-fee basis.

What does that mean for you? It means you pay absolutely nothing upfront. We cover all the costs of investigating your accident, building your case, and pursuing your claim. Our fee is simply a percentage of the settlement we successfully recover for you.

In plain English: If we don’t win your case, you don’t pay us a single dime. This approach ensures that everyone, regardless of their financial situation, has access to top-tier legal help when they need it most.

Should I Just Take the First Offer from the Insurance Company?

Be extremely careful with any early settlement offer you receive from an insurance adjuster. These first offers are almost always a lowball tactic designed to close your case out quickly and for as little money as possible.

Think about what that first offer rarely, if ever, includes:

- Future Medical Needs: It almost certainly won't cover the cost of ongoing physical therapy, potential future surgeries, or long-term pain management.

- Lost Earning Capacity: It completely ignores how your injuries might impact your ability to earn a living months or even years down the road.

- Full Pain and Suffering: It drastically minimizes the immense physical pain and emotional trauma—your non-economic damages—that you've been forced to endure.

Once you accept an offer and sign that release form, your case is closed forever. You can't go back for more money, even if your injuries turn out to be far more serious than you first realized. Before you sign anything, let us take a look. A free consultation with our team can help you understand what your car accident claim is really worth and stop you from leaving money on the table.

When you’re ready to fight for the compensation you deserve, The Law Office of Bryan Fagan, PLLC is here for you. We understand what you are going through, and we are ready to help you take the first step toward recovery. Contact us today for a free, no-obligation consultation to discuss your case and learn how we can protect your rights and your future.