A car crash can change your life in seconds—but you don’t have to face recovery alone. When a wreck turns your world upside down, the last thing you should be worrying about is how you’ll pay for the immediate aftermath. In Texas, your own auto insurance policy can be a crucial first line of defense, offering something called Personal Injury Protection, or PIP.

Think of it as a financial first aid kit. It’s designed to help you cover initial medical bills and lost wages right away, no matter who was at fault for the crash. This guide will explain your rights, define key terms, and provide the practical advice you need to protect your family.

Your Financial First Aid Kit After a Texas Car Wreck

After a collision, the physical and emotional trauma is bad enough. But then the financial stress hits. Emergency room bills start piling up. You might be losing income because your injuries keep you from working.

All the while, you’re waiting for the at-fault driver’s insurance to pay, a process that can drag on for months. This is exactly where Texas PIP coverage steps in to bridge that gap.

How PIP Provides Immediate Relief

PIP is a form of no-fault insurance. That’s a key term. It means you can access your benefits to cover expenses without first having to prove the other driver caused the wreck.

This coverage is for you and your passengers. It’s a safety net that gives you breathing room to focus on getting better, not on how you’re going to pay for your next doctor’s visit.

Let’s say you’re a Houston driver rear-ended on I-45 by a distracted driver. This isn’t just some hypothetical—it’s a daily reality for Texans. Under Texas law, your insurance company is required to offer you at least $2,500 per person in PIP coverage. Some drivers choose to waive it in writing to save a few bucks a month, a decision they almost always regret when they’re suddenly facing thousands in out-of-pocket costs.

Protecting Your Financial Stability

Here’s a common misconception: people think that if they use their PIP benefits, they can’t go after the at-fault driver. That’s completely false.

Using your PIP has no impact on your right to file a personal injury claim against the driver who hit you. In fact, it does the opposite—it gives you the financial stability you need while your attorney builds a strong case to get you full and fair compensation for all your losses, or damages.

Plain-English Definitions:

- Damages: The legal term for the losses an accident victim suffers, including medical bills, lost wages, and pain and suffering.

- Liability: The legal responsibility for an accident. Proving the other driver’s liability is key to your personal injury claim.

Of course, your injuries are only one piece of the financial puzzle. You’ll also be dealing with vehicle damage and potentially unexpected repair costs. While PIP is focused on your medical bills and lost income, it’s a critical part of a broader strategy to shield yourself from the financial shocks that always follow a serious crash.

If you’ve been injured, the Houston car accident lawyers at The Law Office of Bryan Fagan, PLLC, can walk you through all of your options for recovery and make sure you’re protected.

Understanding What PIP Insurance Actually Covers

So, what does Texas Personal Injury Protection (PIP) actually do for you when you’re staring at a pile of medical bills and lost paychecks after a crash? Think of PIP as your financial first aid kit. It's a no-fault coverage within your own auto insurance claim, designed to get money in your hands fast.

The beauty of PIP is its speed. You don’t have to wait for lawyers to battle over who was at fault. You file a claim with your own insurance company and get immediate help for your most pressing economic needs. It’s a powerful tool that brings stability right when your life has been turned upside down.

What PIP Pays For: Medical Bills and Lost Wages

At its core, PIP is built to tackle the two biggest financial headaches that pop up after an injury accident: medical bills and the income you lose from being unable to work.

A standard Texas PIP policy will cover:

- 100% of Reasonable Medical Costs: This isn’t just a small part of your bills. It covers necessary medical care tied to the crash, like the ambulance that picked you up, the emergency room visit, hospital stays, follow-up appointments with your doctor, X-rays or MRIs, and physical therapy.

- 80% of Lost Income: If the doctor puts you on bed rest or your injuries keep you from doing your job, PIP steps in to replace 80% of your documented lost wages. This is often the lifeline that keeps the rent paid and the lights on while you recover.

It can also cover costs for essential services you can’t perform yourself anymore due to your injuries, like house cleaning or childcare.

What Your Texas PIP Coverage Typically Pays For

After a crash, expenses pile up fast. This table shows the kind of immediate financial relief a standard Texas PIP policy is designed to provide, covering the bills you can't afford to wait on.

| Expense Category | What It Covers | Example Cost in Texas |

|---|---|---|

| Emergency Transport | Ambulance ride from the accident scene to the hospital. | $1,200 – $2,500 |

| Hospital & ER Care | Emergency room visit, initial diagnostics, and hospital admission. | $3,000 – $10,000+ |

| Diagnostic Imaging | X-rays, MRIs, or CT scans needed to diagnose your injuries. | $300 – $5,000 |

| Lost Wages | Replaces 80% of your verified income if you're unable to work. | Varies by income |

| Physical Therapy | Rehabilitation sessions needed to recover function and mobility. | $100 – $350 per session |

| Replacement Services | Cost to hire someone for tasks you can't do (e.g., childcare, cleaning). | Varies |

This coverage acts as a crucial bridge, handling initial costs so you aren't buried in debt while your attorney pursues full compensation from the at-fault party.

A Real-World PIP Scenario in Houston

Let's make this real. Imagine you’re driving on I-45 when another car cuts into your lane, causing a wreck that leaves you with a broken leg. The bills start immediately.

Here’s how a basic $2,500 PIP policy would kick in:

- Ambulance Ride: The ride to the ER costs $1,200. PIP can pay that entire bill.

- Emergency Room Visit: The ER visit, with X-rays and setting your leg, comes to $4,000. Your PIP will cover the first $1,300 of that, which uses up your remaining $2,500 limit.

- Breathing Room: Just like that, you’ve handled $2,500 in urgent medical bills without touching your own bank account. This gives your Houston car accident lawyer the time needed to build a strong case against the at-fault driver for the rest of your medical bills and other damages.

PIP acts as an immediate financial bridge. It handles the initial costs so you aren't forced into debt while waiting for the at-fault driver's insurance company to pay what you are owed.

This example shows why PIP is so vital. It gives you instant relief. You still need to go after the negligent driver’s insurance for your full damages—including the rest of your medical bills, the other 20% of your lost wages, and your pain and suffering—but PIP takes the immediate financial pressure off your shoulders. It works with your main personal injury claim, not instead of it.

It's also crucial to understand how PIP is different from other coverages. To learn more, check out our guide on what Medical Payments coverage is and how it stacks up against PIP.

How PIP Works With Your Other Insurance Coverage

After a serious car wreck, it feels like you're juggling a dozen different problems at once, and insurance is easily the most confusing. You might have health insurance, your own auto policy, and the at-fault driver’s liability coverage all in play. So, who pays first?

The answer in Texas is simple: your Personal Injury Protection (PIP) coverage is primary. This means your PIP benefits are the very first in line to pay for your initial medical bills and a portion of your lost wages. It’s designed to get you immediate financial help before any other insurance even gets involved.

The Order of Payments Explained

Think of your different insurance policies as a series of safety nets. PIP is the first and most important one, there to catch you right after the fall.

Here’s the typical order of how things get paid:

- Your PIP Coverage (Pays First): You’ll start by filing a claim with your own insurance company to tap into these no-fault benefits. They are designed to pay out fast—often within 30 days of receiving your bills—no matter who caused the crash.

- Your Health Insurance (Pays Second): Once you’ve used up all your PIP benefits, your personal health insurance can kick in to cover additional medical treatments. Keep in mind, you’ll likely have to deal with deductibles and co-pays.

- The At-Fault Driver’s Insurance (Pays Last): Getting compensation from the negligent driver's liability policy is the final piece of the puzzle. This money comes from the settlement your attorney negotiates to cover all your remaining damages, including leftover medical bills, the rest of your lost wages, and compensation for your pain and suffering.

Using your PIP benefits is a critical first step. It protects your personal finances while your lawyer does the heavy lifting of building a strong case against the at-fault driver. To get a better handle on these concepts, check out our guide on first-party vs. third-party insurance claims and what they mean for your case.

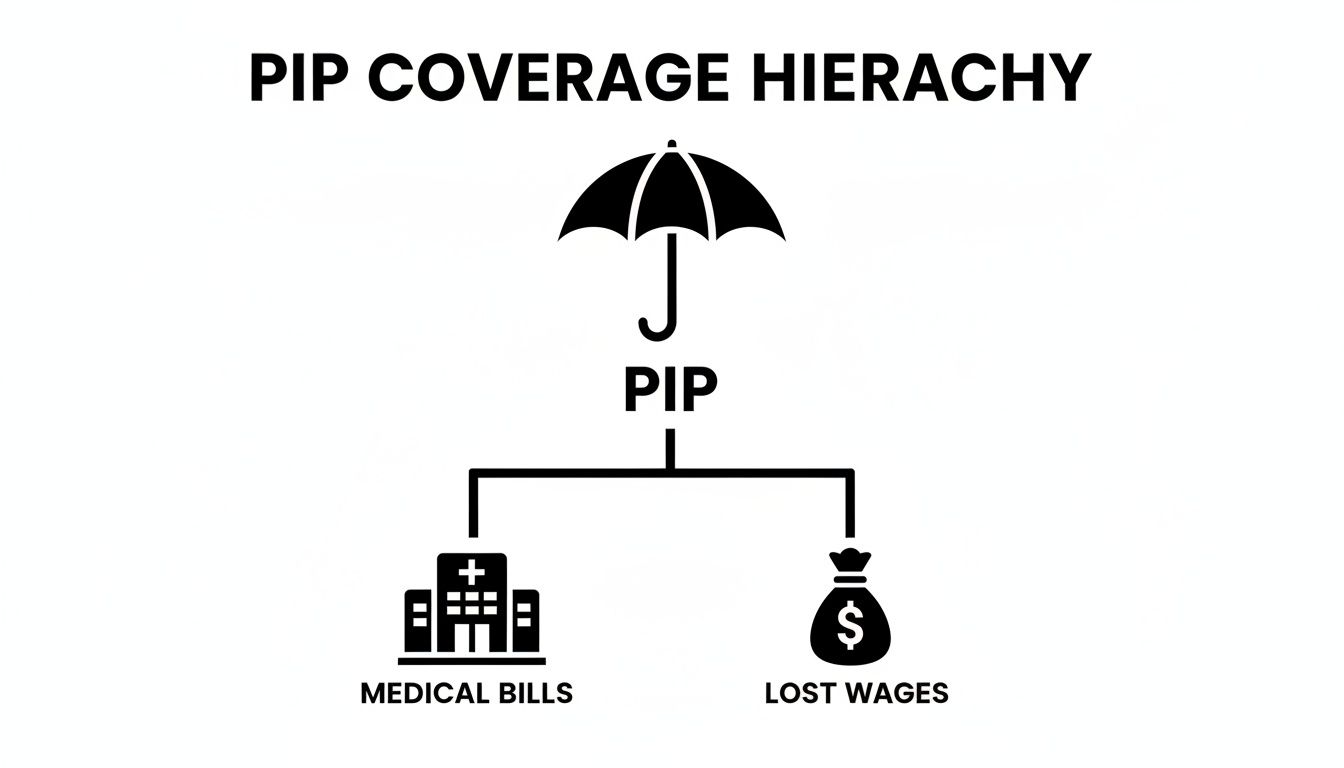

This diagram helps visualize how PIP acts like an umbrella, covering both your immediate medical bills and lost income right after an accident.

As you can see, PIP provides a two-pronged defense against the immediate financial fallout from a serious car wreck.

PIP vs. MedPay and The Myth of "Double Dipping"

A common point of confusion is the difference between PIP and Medical Payments (MedPay) coverage. While they both help with medical bills, PIP is almost always the better choice in Texas because it also covers 80% of your lost wages.

Even more importantly, MedPay policies usually give your insurance company subrogation rights.

Subrogation is a legal term that means if your insurer pays for your bills, they get to demand that money back from your final settlement. But here's the good news: Texas PIP law is a huge benefit to accident victims because it prohibits subrogation.

This means the money you get from your PIP policy is yours to keep, period. The insurance company cannot claw it back from your settlement. This is a critical advantage that helps you walk away with more money in your pocket.

Imagine you’re in a head-on collision in Austin caused by a drunk driver. You can't work, and the physical therapy bills are piling up. While Texas requires drivers to have liability insurance, many are uninsured or just carry the bare minimum. Your Personal Injury Protection (PIP) becomes your financial lifeline, potentially providing the funds you need to pursue wrongful death compensation if the worst happens.

Because PIP pays regardless of fault, it buys you the critical time needed to cover your immediate bills while an attorney fights the insurance companies for the full compensation you deserve. You can learn more about what goes into a Texas car accident settlement on consumershield.com.

Using your PIP benefits doesn't stop you from going after the negligent driver for every penny you're owed. Your personal injury claim will still demand payment for all your damages, including the very same bills your PIP already paid. A skilled Houston injury attorney at The Law Office of Bryan Fagan, PLLC, will manage this process to ensure you recover every dollar you’re entitled to.

How to File a PIP Claim Step by Step

Filing an insurance claim is the last thing you want to worry about after a car accident. When you’re trying to heal, getting your Texas Personal Injury Protection (PIP) benefits should be simple—it's the financial first aid you’ve paid for.

This guide will break down exactly how to open and manage your PIP claim, helping you get the support you’re owed without adding to your stress. The two most important things are moving quickly and keeping everything organized.

The Essential First Steps

The chaos right after a crash can be overwhelming, but a few quick actions can set your PIP claim up for success. The main goal is to get your own insurance carrier officially notified so the process can begin.

Notify Your Insurer Promptly: It doesn't matter if the other driver was 100% at fault—you must contact your own insurance company to use your PIP benefits. Call them as soon as you can after the accident. If you wait too long, the insurer may look for reasons to question your claim.

Formally Open a PIP Claim: When you get them on the phone, be direct. Tell them, "I need to open a Personal Injury Protection claim." The company will give you a dedicated claim number and assign an adjuster to your case. That number is your key to tracking every single part of your claim.

It's a good idea to keep a small notebook or a file on your phone just for the accident. Make sure you write down the claim number, the adjuster's name and contact info, and the date of every phone call.

Submitting Bills and Proving Losses

With your claim officially open, the next step is sending the right paperwork to your adjuster. The adjuster’s job is to confirm that your expenses are reasonable, necessary, and a direct result of the crash.

To get your benefits paid out, you have to submit your medical bills and document any income you've lost.

- Medical Bills: Every time you go to the doctor, hospital, or a physical therapist, get a copy of the bill. Send these straight to your PIP adjuster and make sure to include your claim number on everything you send. Don't let them stack up.

- Lost Wages: To receive the 80% coverage for lost income, you need to provide proof. This is usually a letter from your job that verifies your pay rate and the specific dates you couldn't work because of your injuries. If you're self-employed, you may need to submit tax returns or client invoices.

Staying organized is your best defense against claim delays. Keep copies of every single document you send to the insurance company—bills, receipts, letters from your doctor, and wage loss verification forms. This creates a paper trail that protects you.

Maintaining Communication and Watching for Pitfalls

Don’t just assume your claim is moving along smoothly if you don't hear anything. Check in with your PIP adjuster regularly and politely to make sure things are on track. If a payment is late, ask them why.

Unfortunately, even though PIP is a no-fault benefit, insurers can still put up roadblocks. Keep an eye out for common issues, like an adjuster unfairly claiming a medical treatment was "unnecessary" or saying your lost wage proof isn't good enough. These are red flags that you might need professional help.

When adjusters start playing games, delaying payment, or questioning legitimate costs, it's time to talk to a Texas injury attorney. An experienced lawyer can take over, handle all the communication, and fight to make sure the insurance company honors your policy.

For a deeper look into the general claims process, you can learn more about how to file a car accident claim in our detailed guide. The compassionate attorneys at The Law Office of Bryan Fagan, PLLC, are here to help you navigate every step.

Why You Should Never Waive Your PIP Coverage

Under Texas law, every auto insurance company is required to offer you Personal Injury Protection. But here’s the catch: the law also lets you reject it in writing. It’s a tempting offer for many drivers—a quick signature that seems to shave a few bucks off your monthly premium.

Frankly, it's one of the most dangerous financial gambles you can make.

That small amount you think you're saving—maybe $15 or $20 a month—is a drop in the bucket compared to the mountain of medical debt you could face after a crash. When you waive PIP, you're betting you’ll never get into an accident. Or, if you do, you're betting the other driver will be fully insured and their company will pay up fast. Those are risky bets to make on Texas roads.

The True Cost of Saving a Few Dollars

Let's make this real. Imagine you’re a driver in San Antonio who just waived PIP to save a little cash. A month later, an uninsured driver blows a red light and T-bones you on Loop 410. You walk away with a concussion and a dislocated shoulder, and the emergency room bills alone hit $15,000.

Because you waived PIP, you have no immediate way to cover those costs. Your health insurance might kick in eventually, but only after you’ve paid a high deductible, leaving you on the hook for thousands out of pocket. Your only other option is to sue the at-fault driver—who has no insurance and likely no assets—and hope to recover money that probably isn’t there. This is the exact financial nightmare PIP was designed to prevent.

Or picture a multi-vehicle pileup on I-35. You end up with whiplash and a fractured wrist—injuries that can easily rack up $1,500–$3,000 for a single ER visit in Texas. While a settlement may eventually come from a Texas personal injury claim, PIP is the bridge that gets you there, providing the immediate funds you need to keep your head above water.

Why Higher PIP Limits Are a Smart Investment

The state-mandated minimum for PIP is only $2,500. While that’s better than nothing, it can be completely wiped out by a single ambulance ride and an initial ER visit. That’s why we always tell our clients to look beyond the minimum and get serious about their coverage.

Most insurers offer much better PIP limits, including:

- $5,000

- $10,000

- Sometimes even more

Bumping your PIP limit to $10,000 or higher is one of the most cost-effective moves you can make to protect your family’s financial future. The premium increase is usually minimal, but the protection it buys you is massive. It creates a substantial fund to cover weeks of medical care and lost wages, giving you true peace of mind.

Think of higher PIP limits as an investment in your own financial security. For just a few extra dollars a month, you are buying protection from tens of thousands in potential out-of-pocket costs.

When you're trying to heal from a wreck, the last thing you need is a second crisis—a financial one. Keeping your Texas personal injury protection and opting for a higher limit gives you back a measure of control and stability when you need it most. If you're not sure what your policy includes or you need help after a crash, an experienced car accident lawyer can review your coverage and fight for every dollar you deserve.

How a Lawyer Maximizes Your Total Accident Recovery

Think of your Texas Personal Injury Protection (PIP) coverage as the first responders of your financial recovery—it’s there to provide immediate relief. It's a fantastic tool for covering initial medical bills and lost paychecks, but it’s just the start.

PIP was never designed to cover the full, devastating impact of a serious crash. That’s where a skilled car accident lawyer comes in. At The Law Office of Bryan Fagan, PLLC, we don't just manage your PIP claim; we build the comprehensive case needed to get you all the compensation you deserve.

Beyond PIP: Pursuing Full and Fair Damages

Your PIP policy is great for those immediate, calculable costs. But what about the pain that keeps you up at night? The trauma you relive every time you get in a car? PIP doesn't—and can't—touch these losses.

To get fair compensation for the true scope of your suffering, you need to file a personal injury claim against the driver who caused the accident. This is how you pursue damages for everything else, including:

- Pain and Suffering: The real-world physical pain and emotional turmoil caused by your injuries.

- Mental Anguish: The very real anxiety, trauma, and depression that follow a violent wreck.

- Future Medical Expenses: The projected costs for surgeries, long-term care, or physical therapy you'll need down the road.

- Lost Earning Capacity: The income you won't be able to earn because your injuries have impacted your ability to work.

We focus on telling your whole story—using medical records, expert testimony, and your own experience—to show the insurance company exactly how this crash turned your life upside down.

Navigating Critical Texas Laws

Insurance companies have one goal: to pay you as little as possible. They have entire teams of lawyers dedicated to minimizing their payouts. Having an advocate on your side levels the playing field, especially when you’re up against a clock and tricky Texas laws.

Plain-English Definitions:

- Statute of Limitations: In Texas, you have two years from the date of the accident to file a personal injury lawsuit. If you miss this deadline, you lose your right to seek compensation forever. An attorney ensures all deadlines are met.

- Comparative Fault: Under Texas law (Texas Civil Practice & Remedies Code Chapter 33), if you are found partially at fault for an accident, your final settlement can be reduced by your percentage of fault. For example, if you are 20% at fault, your award is cut by 20%.

Hiring a Texas injury attorney immediately is your best defense against these strategies. We get to work right away investigating the crash to establish the other driver's full liability and shut down any attempts to unfairly blame you.

If you’ve been hurt, don’t try to take on the insurance companies alone. Contact The Law Office of Bryan Fagan, PLLC, for a free consultation. Let us handle the legal fight so you can focus on what truly matters: your recovery.

Common Questions About Texas PIP Insurance

After a wreck, the last thing you need is a runaround from an insurance company. You’re hurt, you’re stressed, and you need straight answers. Here are some of the most common questions we get from our clients about Personal Injury Protection in Texas.

Can I Use PIP if the Accident Was My Fault?

Yes. This is the single most important thing to understand about Texas personal injury protection. It is “no-fault” coverage.

That means you can tap into your benefits to cover medical bills and lost wages no matter who caused the accident. Even if you were 100% responsible for the crash, you are still entitled to use the PIP benefits you've paid for. Think of it as the immediate safety net you bought for yourself.

Will Using My PIP Benefits Make My Insurance Premiums Go Up?

This is a huge worry for a lot of people, and it’s a fair question. The good news is that in Texas, insurance companies are legally forbidden from jacking up your rates just because you filed a single PIP claim, particularly if the accident wasn't your fault.

Your PIP coverage is a benefit you've already paid for through your premiums. You should never be punished for using it to protect your health and your family’s finances after a crash.

If you’re still worried about a potential rate hike, a Texas injury attorney can give you specific advice. But the truth is, the financial shield PIP provides almost always outweighs any small, hypothetical risk to your future premiums.

Are My Passengers Covered Under My PIP Policy?

They are. Your PIP coverage is tied to your vehicle, not just to you as the driver. This means if you get into an accident, your policy will cover you and any passengers riding in your car at the time of the collision, up to your policy's per-person limit.

This protection is surprisingly broad. It can also extend to family members who live with you, even if they get hit by a car as a pedestrian or are injured while riding in someone else's vehicle.

What Should I Do if My Medical Bills Exceed My PIP Limit?

This happens all the time. A single trip to the emergency room can burn through the minimum $2,500 PIP limit in a heartbeat. Once your PIP benefits are exhausted, you have a couple of primary options:

- Your Health Insurance: Your personal health insurance is the next line of defense. It can cover the rest of your medical costs, but you'll still be on the hook for deductibles and co-pays.

- The At-Fault Driver's Insurance: The real goal is to file a personal injury claim against the driver who caused the wreck. This is how you recover money for all your damages—the medical bills that PIP didn't cover, your pain and suffering, and any future medical care you might need.

Maxing out your PIP coverage is a big red flag. It’s a clear signal that it's time to talk to an experienced Houston car accident lawyer who can manage your bills while building a powerful case against the person who hurt you.

After a crash, you shouldn’t have to fight insurance companies alone. The Law Office of Bryan Fagan, PLLC, is here to protect your rights and help you get the full compensation you deserve. We inform, reassure, and empower our clients every step of the way. Contact us today for a free, no-obligation consultation to discuss your case and understand your options. Get the help you need now.