A car crash can change your life in seconds—but you don’t have to face recovery alone. In the chaotic aftermath, the single most important tool for your financial protection is liability insurance—the specific coverage that every at-fault driver is legally required to carry in Texas.

This coverage is designed to pay for the injuries and property damage they cause to others. When you're the one left picking up the pieces after a crash caused by someone else's carelessness, their policy is where your recovery starts.

Understanding Your First Steps with Texas Liability Insurance

After a crash, it's completely normal to feel overwhelmed. You're hurt, your car is wrecked, and the stress is piling up. The first step toward regaining control is understanding the basics of liability insurance in Texas, since this is the primary source of compensation you'll turn to when the other driver was to blame.

Every driver on a Texas road must carry what's known as 30/60/25 liability coverage. These aren't just random numbers; they represent hard dollar limits that will directly impact how much you can recover for your losses.

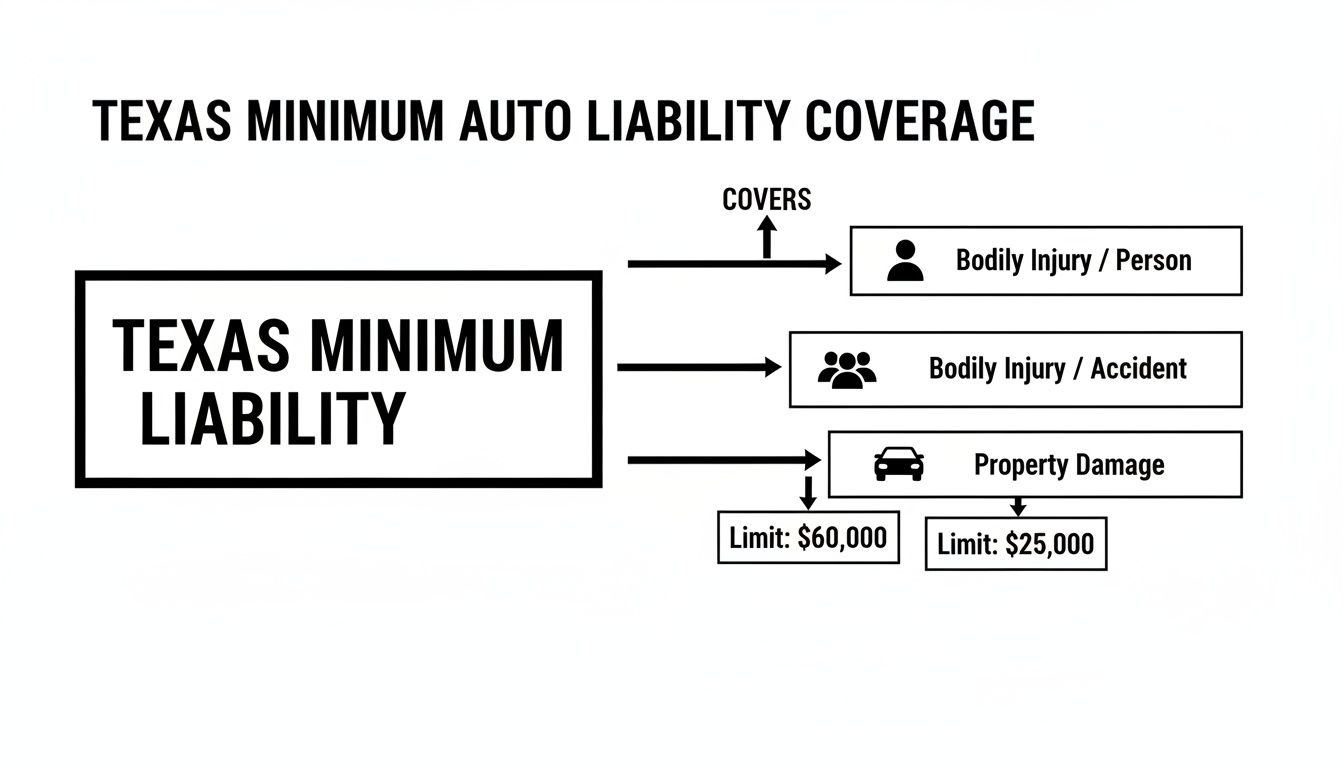

What Do the Minimum Coverage Numbers Actually Mean?

It's helpful to think of "30/60/25" as three separate pots of money the at-fault driver's insurance company has available to cover the harm they caused. Each number serves a very specific purpose:

- $30,000 Bodily Injury Liability per person: This is the absolute maximum the insurer will pay for any single person's medical bills, lost income, and pain and suffering.

- $60,000 Bodily Injury Liability per accident: This is the total cap for all injuries in the crash. It doesn't matter if two, three, or five people were hurt—$60,000 is the most the policy will pay out for everyone combined.

- $25,000 Property Damage Liability per accident: This is the maximum amount available to fix or replace your vehicle and any other property that was damaged, like a laptop in the trunk or a fence that was hit.

To make this crystal clear, we've broken down Texas's mandatory '30/60/25' liability requirements in the table below. It lays out what each part of the policy is for and its corresponding minimum dollar amount.

Texas Minimum Liability Insurance Requirements at a Glance

| Coverage Type | Minimum Amount | What It Covers |

|---|---|---|

| Bodily Injury Liability (BI) | $30,000 | The maximum payout for a single person's injuries in an accident. |

| Bodily Injury Liability (BI) | $60,000 | The total maximum payout for all injuries combined in a single accident. |

| Property Damage Liability (PD) | $25,000 | The maximum payout for all property damage, primarily your vehicle repairs. |

Understanding these limits is the first step in figuring out what compensation is immediately available after being hit by a negligent driver.

Why the State Minimum Is Often Not Enough

Here’s the harsh reality: while this coverage is legally required, it's frequently not enough to cover the actual costs of a serious crash.

For instance, a single night's stay in a Houston-area hospital can easily blow past the $30,000 per-person limit. If your injuries are severe, require surgery, or involve long-term rehabilitation, the at-fault driver's policy can run out almost immediately, leaving you on the hook for thousands in unpaid medical bills. The problem gets even worse if multiple people were injured, as everyone has to share that limited $60,000 pot.

This is a critical and frustrating situation we see all the time. The other driver followed the law, but their bare-bones insurance policy comes nowhere close to making you whole again. This is precisely why it’s so important to understand your own policy, especially your Uninsured/Underinsured Motorist (UIM) coverage, which is designed to protect you in these exact scenarios.

At The Law Office of Bryan Fagan, PLLC, our job is to help you navigate these complex insurance limits and uncover every possible source of compensation. If you've been injured, you don't have to face the insurance maze by yourself. Contact our dedicated Houston car accident lawyers for a free, no-obligation consultation to talk about your rights and legal options.

What Does Liability Insurance Actually Pay For?

When another driver’s mistake leaves you with a wrecked car and mounting medical bills, their liability insurance is supposed to be the financial backstop that makes you whole again. But what does it really cover?

Think of it this way: the other driver’s policy is there to pay for your damages—a legal term for all the losses you suffered because of their negligence. These payments come from the two distinct parts of their liability coverage: Bodily Injury (BI) and Property Damage (PD).

Covering the Cost to Your Body and Well-Being

The Bodily Injury portion of the at-fault driver's policy is designed to cover everything related to your physical injuries. It’s not just about the ER visit; it’s meant to address the entire financial and personal fallout from the crash.

BI liability is intended to pay for:

- Medical Expenses: This is the big one. It covers the ambulance ride, hospital stays, surgeries, physical therapy, prescription drugs, follow-up appointments, and any medical equipment you might need.

- Lost Wages: If you can’t work because of your injuries, this coverage is supposed to replace that lost income. It can also cover your loss of future earning capacity if the injuries are permanent and impact your career long-term.

- Pain and Suffering: This compensates you for the physical pain, emotional distress, and mental anguish the crash has caused. It’s harder to put a price tag on, but it’s a very real and critical part of your claim for damages.

For example, a Houston driver rear-ended on I-45 who suffers a serious back injury can seek compensation from the at-fault driver's Bodily Injury Liability for their surgery costs, months of lost income, and the chronic pain they now have to live with. To dig deeper into this, you can learn more about what is bodily injury liability coverage in our detailed guide.

Paying for Your Damaged Property

The second piece of the puzzle is Property Damage Liability. This part is much more straightforward. It’s there to pay for the repair or replacement of your vehicle and anything else you own that was damaged in the collision.

This typically includes:

- The bill from the auto body shop to fix your car.

- The actual cash value of your vehicle if it’s totaled.

- Damage to personal items inside the car, like a laptop or phone that was destroyed.

- The cost of a rental car while yours is out of commission.

It's crucial to remember that the at-fault driver's liability insurance pays for your damages, not their own. Their policy provides zero coverage for their own injuries or vehicle repairs. It exists solely to compensate you—the victim of their mistake.

The Critical Gaps in Liability Coverage

While liability insurance is non-negotiable, it has some massive limitations that can leave you in a tough spot. The most glaring problem is when the at-fault driver only carries the bare minimum coverage required by Texas law.

As we've seen, a $30,000 Bodily Injury limit can be wiped out by a single serious injury, leaving you with a mountain of unpaid bills.

This is where your own insurance policy becomes your most important safety net. Coverages like Personal Injury Protection (PIP) and Uninsured/Underinsured Motorist (UM/UIM) are specifically designed to fill these gaps. PIP helps cover your initial medical costs no matter who was at fault, and UM/UIM kicks in when the other driver has too little insurance—or none at all. Without them, you could be stuck paying for someone else's negligence.

How Texas Law Determines Who Is Liable in a Car Accident

When another driver hits you, it seems simple enough: their liability insurance should cover your damages. But before a single dollar is paid, the insurance company has to answer one critical question: who was legally at fault?

In Texas, this financial responsibility is built on the legal concept of negligence. In plain English, negligence means someone failed to act with reasonable care, and that failure caused you harm. A driver who runs a red light, glances at a text, or tailgates another car has acted negligently. Proving that negligence is the cornerstone of every personal injury claim.

Understanding Comparative Fault in Texas

Texas law recognizes that accidents are not always 100% one person's fault. This is where the state’s modified comparative fault rule (Texas Civil Practice & Remedies Code § 33.001), also known as the "51% bar," comes into play. This is one of the most important factors that will shape your financial recovery.

Here’s how it works: an insurance adjuster or a jury will assign a percentage of fault to everyone involved. As long as you are found to be 50% or less responsible, you can still recover money from the other party.

However, your total compensation will be reduced by your percentage of fault. If you are found to be 51% or more at fault, you are barred from recovering any money at all.

Real-World Example:

Imagine a driver is T-boned at a busy Houston intersection. A jury decides the other driver was 80% at fault for running a yellow light. However, they determine our driver was 20% at fault for going slightly over the speed limit. If the total damages are $100,000, our driver’s award is reduced by their 20% of fault. They can recover $80,000.

How Insurance Adjusters Use Fault to Lower Payouts

Insurance adjusters are masters of this rule. Their job is to protect their company's bottom line, which means paying out as little as possible. They will dig into the police report, pick apart witness statements, and even twist your own words to pin some percentage of the blame on you.

Even if they only manage to assign you 10% or 20% of the fault, that can save their company thousands of dollars on your claim. It's a classic tactic they use to justify a lowball settlement offer. You can learn more about comparative negligence in Texas and how it affects injury claims in our detailed guide.

The System Designed to Protect You

While insurers are focused on their profits, it's important to remember that Texas has regulations in place to protect consumers. The Texas Department of Insurance was overhauled back in the 1990s to promote fair competition and keep rates stable for drivers.

Those decades-old rules still form the backbone of consumer protection today. But even with these protections, fighting an unfair fault assessment takes evidence and experience.

An experienced Houston car accident lawyer knows how to build a case that clearly shows the other driver’s negligence while defending you against any attempts to unfairly shift the blame. We gather the proof that matters—traffic camera footage, accident reconstruction reports, and expert testimony—to tell the true story of what happened and protect your right to full and fair compensation.

Common Hurdles When Filing a Liability Insurance Claim

Filing an insurance claim after a car accident should be straightforward: you report the facts and get paid fairly for your damages. Unfortunately, that’s rarely how it works. When you file an auto insurance claim against the other driver's liability insurance, you’re not dealing with a neutral party. You're up against a business laser-focused on its own bottom line.

Their goal is simple: pay you as little as possible, or better yet, nothing at all. To do that, insurance adjusters pull from a standard playbook of tactics designed to delay, devalue, or deny your claim. Knowing what to expect is the first step toward protecting yourself.

The Lowball Settlement Offer

One of the oldest tricks in the book is the quick, lowball settlement offer. Just a few days after the crash, an adjuster will call, sounding incredibly friendly and concerned. They might offer you a check for a few thousand dollars on the spot, framing it as a way to help with your immediate bills.

It’s tempting, especially when you’re out of work and medical expenses are piling up. But this offer is almost always a fraction of what your claim is really worth. They’re betting you’ll take the cash before you understand the full extent of your injuries, the cost of future medical care, or how long you’ll be unable to work.

Once you accept a settlement and sign that release form, your case is over for good. You can't go back and ask for more money later, even if you find out you need surgery or long-term physical therapy.

Disputing Your Injuries and Medical Needs

Another common tactic is to question the severity of your injuries. The adjuster might argue that your medical treatments weren't necessary, that your injuries were pre-existing, or that you’re just exaggerating your pain.

It’s a deeply frustrating strategy meant to make you doubt your own experience. The insurance company might:

- Comb through your medical history, looking for any old injury they can blame for your current pain.

- Challenge your doctor's treatment plan, suggesting you should have tried cheaper alternatives.

- Hire their own "medical expert" to review your file and write a report claiming your injuries aren't as bad as you and your doctor say they are.

The entire point is to create doubt and find an excuse to pay less for your medical bills and your pain and suffering.

Shifting the Blame onto You

As we’ve covered, Texas's comparative fault rule is a powerful weapon for insurance companies. They will dig into every detail of the crash, looking for any excuse—no matter how small—to pin a percentage of the blame on you.

Were you driving one mile per hour over the speed limit? Did you hit the brakes a split-second too late? They will twist any detail they can find to argue that you were partially at fault. Shifting just 10% of the blame onto you cuts their payout by 10%, saving them a ton of money. You can learn more about the specific reasons and methods they use by reading about why insurance companies deny claims and the strategies they employ.

Understanding the Economic Pressures

It's also helpful to remember that insurance companies in Texas are under enormous financial pressure. The state's insurance market is a huge part of the economy, making up 8.2% of its GDP. But factors like explosive population growth in cities like Houston, skyrocketing vehicle repair costs, and frequent, severe weather events have squeezed their profit margins thin. That economic reality often leads to more aggressive tactics as they fight harder than ever to limit payouts. You can find more data about the property and casualty insurance industry in Texas on ibisworld.com.

Finally, you might get hit with frustrating coverage disputes. The insurer could claim the at-fault driver’s policy lapsed right before the crash or that the specific circumstances of your accident aren't covered. These aren't just administrative hiccups; they are calculated moves. A skilled Houston car accident lawyer has seen these tactics thousands of times and knows how to build a powerful, evidence-based case that forces the insurer to play fair.

Steps to File an Insurance Claim After a Crash

In the chaos right after a car wreck, it’s almost impossible to think clearly. But the steps you take—or don't take—in those first few hours can make or break your ability to get fair compensation down the road. This practical, step-by-step advice can protect your rights and build a strong foundation for your auto insurance claim.

Before anything else, your health and safety are the top priority. Even if you feel fine, get a professional medical evaluation right away. The adrenaline rush from a crash can easily mask serious injuries like whiplash or internal bleeding that might not show up for hours or even days. Seeking immediate medical care ensures you get the treatment you need and creates an official record that links your injuries directly to the accident.

1. Document Everything at the Scene

As soon as it's safe, start gathering evidence at the scene. This information is the bedrock of your claim and your best defense against the other driver changing their story later on.

- Report the Accident: Always call 911. A police report is an official, unbiased record of what happened, and insurance adjusters take it seriously.

- Take Pictures and Videos: Use your smartphone to document everything. Get photos of both cars from different angles, the license plates, skid marks, nearby traffic signs, and any visible injuries you have.

- Exchange Information: Get the other driver's name, address, phone number, and—most importantly—their insurance policy information. Ask any witnesses for their names and contact info, too.

2. Notify Insurers and Understand Your Deadline

You should report the accident to your own insurance company, even when you weren't at fault. Stick to the basic facts: who, what, where, and when.

When you contact the at-fault driver’s insurance company, remember that their adjuster is not on your side. Never give a recorded statement without first speaking to a Texas injury attorney. They are trained to ask tricky questions designed to get you to downplay your injuries or accidentally admit partial fault.

You also need to be aware of the statute of limitations. In plain English, this is the legal deadline to file a lawsuit. In Texas, you generally have just two years from the date of the accident to file a personal injury lawsuit. If you miss this deadline, you lose your right to seek compensation forever.

3. Seek Legal Guidance to Protect Your Rights

The Law Office of Bryan Fagan, PLLC, is here to guide you through every one of these steps. We handle the insurance adjusters and the legal legwork so you can focus on what truly matters: your recovery. Contact our compassionate team for a free, no-obligation consultation to discuss your case.

How a Texas Car Accident Attorney Levels the Playing Field

After a crash, trying to take on an insurance company by yourself is an uphill battle. You’re supposed to be focused on healing from your injuries, but suddenly you’re expected to become an expert negotiator and claims specialist overnight.

It’s overwhelming. But you don’t have to face it alone.

When you hire a dedicated Texas car accident lawyer from The Law Office of Bryan Fagan, PLLC, the playing field is instantly leveled. We step in as your advocates, managing every single detail of your claim so you can focus on what truly matters—your recovery.

Your Advocate and Investigator

From day one, we take over. All communication with the insurance company goes through us. No more stressful calls from adjusters trying to pressure you into a quick, lowball settlement.

Our team immediately launches a thorough investigation into the crash to gather the hard evidence needed to establish clear liability. This means collecting police reports, tracking down and interviewing witnesses, and, when necessary, bringing in accident reconstruction experts to prove exactly how the collision happened.

We then meticulously calculate the full and fair value of your damages, digging much deeper than just the initial hospital bills. Our calculations include:

- All current and future medical expenses, from the ER visit to long-term physical therapy and rehabilitation.

- Lost income and diminished earning capacity if your injuries keep you out of work or impact your career long-term.

- Pain and suffering, which accounts for the immense physical and emotional toll the accident has taken on your life.

Negotiating from a Position of Strength

Armed with solid evidence and a comprehensive valuation of your claim, we negotiate relentlessly for a settlement that is just. Insurance companies are businesses, and they know we are fully prepared to take your case to court if they refuse to be fair.

This willingness to go to trial is often the key to securing a fair offer without ever having to step inside a courtroom. They take our demands seriously because they know we won't back down.

For any legal practice, understanding how to achieve strong online visibility is crucial. This is especially true for those focusing on personal injury, where effectively marketing legal services can be key to helping clients. Learn more about strategies for Unleashing Business Growth Online in Texas. Our firm understands that many Texas families also face complex financial circumstances that affect their insurance decisions. Texas law even allows insurers to use credit scores in setting rates, meaning drivers with poor credit often pay significantly higher premiums, sometimes over $1,000 more annually for full coverage. This isn't just about a car wreck; it's about protecting your rights and securing the financial stability your family needs to move forward.

Common Questions After a Texas Car Accident

After a serious wreck, your head is spinning with a million questions. Finding clear, straightforward answers is the first step toward getting your feet back on the ground. Here are some of the most common questions we hear from injured Texans trying to figure out what comes next.

What if the Other Driver's Insurance Can't Cover All My Bills?

This is an incredibly common and stressful scenario, especially since Texas requires such low minimum liability coverage. When the at-fault driver's policy runs out but you're still facing a mountain of medical bills and lost wages, you'll need to look at other options.

This is exactly what your own Uninsured/Underinsured Motorist (UIM) coverage is for. It's a crucial part of your own insurance policy designed to kick in and cover the gap between what the other driver’s policy paid and what you're truly owed, right up to your own UIM limits.

If you don't have UIM coverage, it gets tougher—but not impossible. An experienced car accident attorney can dig deeper to find other sources of recovery. That could mean going after the at-fault driver’s personal assets or finding out if another party (like their employer) shares some of the blame. These are definitely more complex legal fights, but they can be necessary.

Should I Give the Other Driver's Insurance Adjuster a Recorded Statement?

No. We strongly advise you to politely decline. Never give a recorded statement without your own lawyer present.

It's easy to think the adjuster is just trying to gather facts, but that's not their job. Their one and only goal is to protect their company's bottom line by paying you as little as possible.

Adjusters are trained professionals skilled at asking tricky, leading questions. They know how to get you to say something they can later twist to downplay your injuries, question the facts of the crash, or even pin some of the blame on you.

The best response is simple and firm: "I'm not comfortable giving a recorded statement right now. My attorney will be in contact with you." That one sentence protects you from having your own words used against you down the road.

How Long Do I Have to File a Lawsuit for a Car Wreck in Texas?

In Texas, the law that sets the deadline for filing a personal injury claim is called the statute of limitations. For most car accidents, you have two years from the date of the crash to file a lawsuit.

This is a hard-and-fast deadline. If you miss it, you lose your right to seek compensation forever. No exceptions.

And while two years might sound like plenty of time, it disappears quickly. Building a solid case means gathering evidence, tracking down witnesses, getting expert opinions, and dealing with the insurance company. Contacting a Texas injury attorney right away ensures that all the critical pieces are preserved while they're still fresh and that every legal deadline is met with time to spare. Don't wait until the clock is running out to protect your rights.

A car accident can make you feel completely overwhelmed and powerless, but you do not have to take on the insurance companies by yourself. At The Law Office of Bryan Fagan, PLLC, our compassionate Houston personal injury attorneys are here to take the legal burden off your shoulders. We will answer your questions, fight for the wrongful death compensation your family may deserve, and work tirelessly for every dollar you need to recover. Contact us today for a free, no-pressure consultation to discuss your case and find out how we can help you move forward.