Skip to content

Skip to content

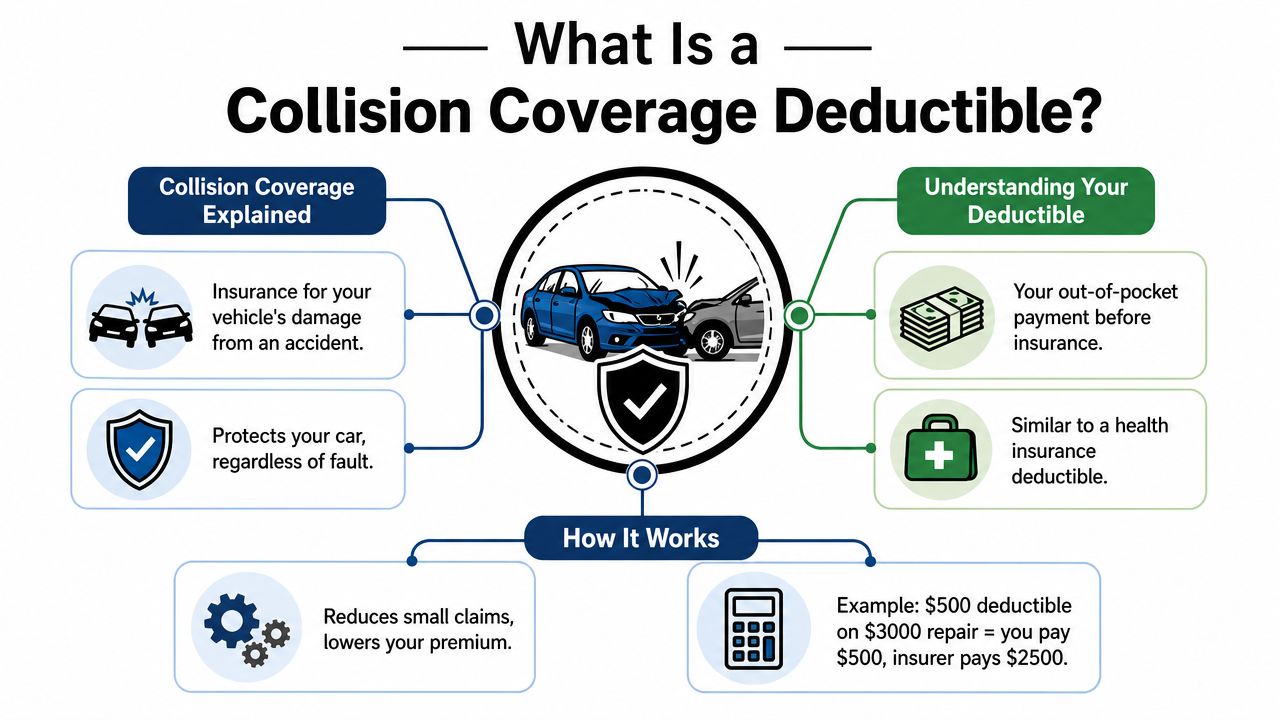

A collision coverage deductible is the amount of money you must pay out of pocket for car repairs after an accident before your own insurance company starts paying. Common deductible choices include $250, $500, $1,000, and $2,000, and $500 is the most common amount.

A car crash can change your life in seconds, but you don't have to face recovery alone. If you're reading this after a wreck in Houston or anywhere in Texas, you may already be dealing with repair shops, adjusters, missed work, and a car you need back on the road. Then the insurance company tells you that you still have to pay your deductible, even though the other driver caused the crash.

That's where many people feel blindsided.

A lot of drivers assume that if someone else was at fault, they won't have to pay anything up front. Sometimes that happens. Often, it doesn't. You may need to use your own collision coverage to get moving again, pay the deductible first, and then fight to get that money back later.

Your Guide to Navigating Insurance After a Texas Crash

If your car is damaged in a crash, your deductible is usually the first part of the repair bill that becomes your problem. Your insurer pays the rest of a covered collision claim after that amount is satisfied. That sounds simple on paper, but real claims rarely feel simple when you're the one trying to get to work, pick up your kids, or figure out whether the other driver's insurer is going to accept fault.

Texas drivers often run into trouble at the same point. The other insurer says it's still investigating. Your own insurer agrees to handle the repairs under your policy. The body shop starts work, and then you're told to pay your deductible before you can get your car back.

You can be right about fault and still have to pay first.

That doesn't mean you've lost the money for good. It means the recovery process may take more than one step. In many cases, your insurer will try to recover what it paid, along with your deductible, from the at-fault driver's insurer. If you're dealing with a national carrier and want to understand one common workflow, this guide to the State Farm claims process can help you see how these disputes often unfold.

The key is to understand what the deductible is, when it applies, and how Texas liability rules affect whether you get reimbursed. Once you understand that, you can make better choices and protect your rights during the claim.

What Is a Collision Coverage Deductible

A deductible is the amount you agree to pay out of pocket before your collision coverage pays for damage to your vehicle after a covered crash. Collision coverage usually applies when your car hits another vehicle or an object, such as a pole, fence, or guardrail. Insurers commonly offer deductible options such as $250, $500, $1,000, or $2,000, and Investopedia's overview of collision coverage notes that $500 is a common choice.

A simple way to read the math

The deductible is your share of a covered repair bill.

If your car has $10,000 in covered collision damage and your deductible is $500, your insurer would generally pay $9,500 and you would pay $500. The deductible applies per claim. If you have another separate covered crash later, the deductible can apply again.

That point matters in Texas because many drivers assume fault decides who pays first. Often, it does not. Your collision claim runs through your own policy first, even when another driver likely caused the wreck.

What collision coverage does and does not pay for

Collision coverage focuses on damage to your own vehicle. Liability coverage is different. It pays for damage or injuries you cause to other people. If you want a plain-language comparison, this resource can help you understand full coverage or liability.

Three parts of the claim often get mixed together:

- Damage to your car: Usually handled under your collision coverage if you bought it.

- Who caused the crash: That affects who should ultimately reimburse the loss.

- Your deductible: This usually comes out of your pocket first if you use your own policy.

A practical example helps. A driver in Houston gets rear-ended on I-45. Liability looks clear. Yet the other insurer may still dispute fault, delay its decision, or argue about how the crash happened. Meanwhile, the driver needs the car repaired now, not weeks from now. Filing through collision coverage can get the repairs moving, but it usually also means paying the deductible up front.

That is the part many people do not expect. The primary fight is sometimes not about whether you had coverage. It is about whether you ever get that deductible back after your insurer finishes the repair payment and starts trying to recover from the at-fault driver's insurer through subrogation. If liability remains disputed, recovering that money can take persistence and, in some cases, legal action tied to the broader accident claim.

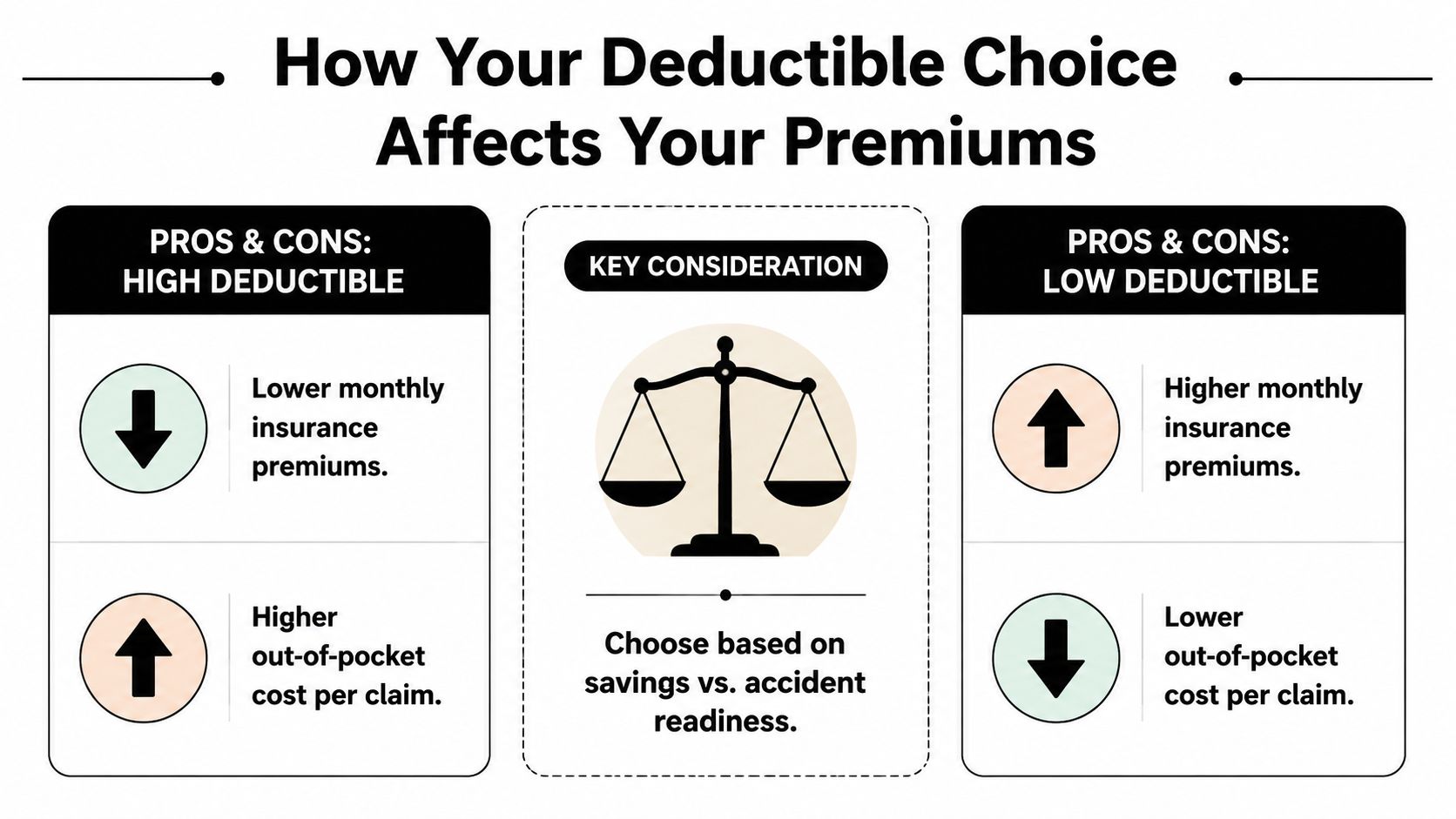

How Your Deductible Choice Affects Your Premiums

A deductible is the part of the repair bill you agree to carry yourself before your collision coverage starts paying. Your premium is the price you pay each month or every six months to keep that coverage in place. The balance between those two numbers matters a great deal after a Texas crash, especially if you need repairs quickly and later have to fight to get your deductible back.

The basic rule is simple. A higher deductible usually lowers your collision premium. A lower deductible usually raises it.

That tradeoff exists because collision claims are often expensive. In 2024, the average collision claim was $5,489, according to the Insurance Information Institute auto insurance facts and statistics page. If an insurer agrees to take on more risk before you pay out of pocket, it generally charges more for that promise.

The basic tradeoff

A deductible works like choosing how much of the first hit you can absorb yourself.

| Deductible choice | What usually happens |

|---|---|

| Lower deductible | Higher premium, but less to pay if you file a claim |

| Higher deductible | Lower premium, but more to pay after a crash |

A driver who chooses a $1,000 deductible instead of $500 may save money on premiums over time. But after a wreck, that driver usually has to come up with an extra $500 before the car is released from repair or the claim is fully processed. For many families, that difference is not abstract. It is rent money, grocery money, or the cost of getting to work next week.

How to think about your own risk

A better question than "What is the cheapest premium?" is this: If your car were damaged tomorrow, how much could you pay without throwing the rest of your month into chaos?

That is the number to build around.

Many Texas drivers focus on the premium because it shows up regularly on the bill. The deductible feels distant until a crash happens. Then it becomes immediate. If the other driver caused the wreck but that insurer disputes liability, you may still need to pay your own deductible first to get repairs started under your collision coverage. A high deductible can save money on paper, yet create real pressure when you are waiting on reimbursement through subrogation or trying to recover that amount as part of a broader injury or property damage claim.

Practical rule: Choose a deductible you could realistically pay during a bad month, not just a good one.

That approach helps you prepare for the problem many people overlook. The hard part is not always buying the policy. The hard part is carrying the deductible up front while insurers argue over fault and you wait to see whether that money comes back.

Getting Your Deductible Back After a Texas Accident

You get hit on a Houston freeway during the evening commute. The other driver says you stopped too fast. Your car needs repairs right away, so you use your own collision coverage and pay the deductible to get the work started. A few weeks pass, and the other insurer still has not accepted fault.

That is the part many Texas drivers do not see coming. Paying the deductible is often only the first step. Getting it back can turn into a second fight.

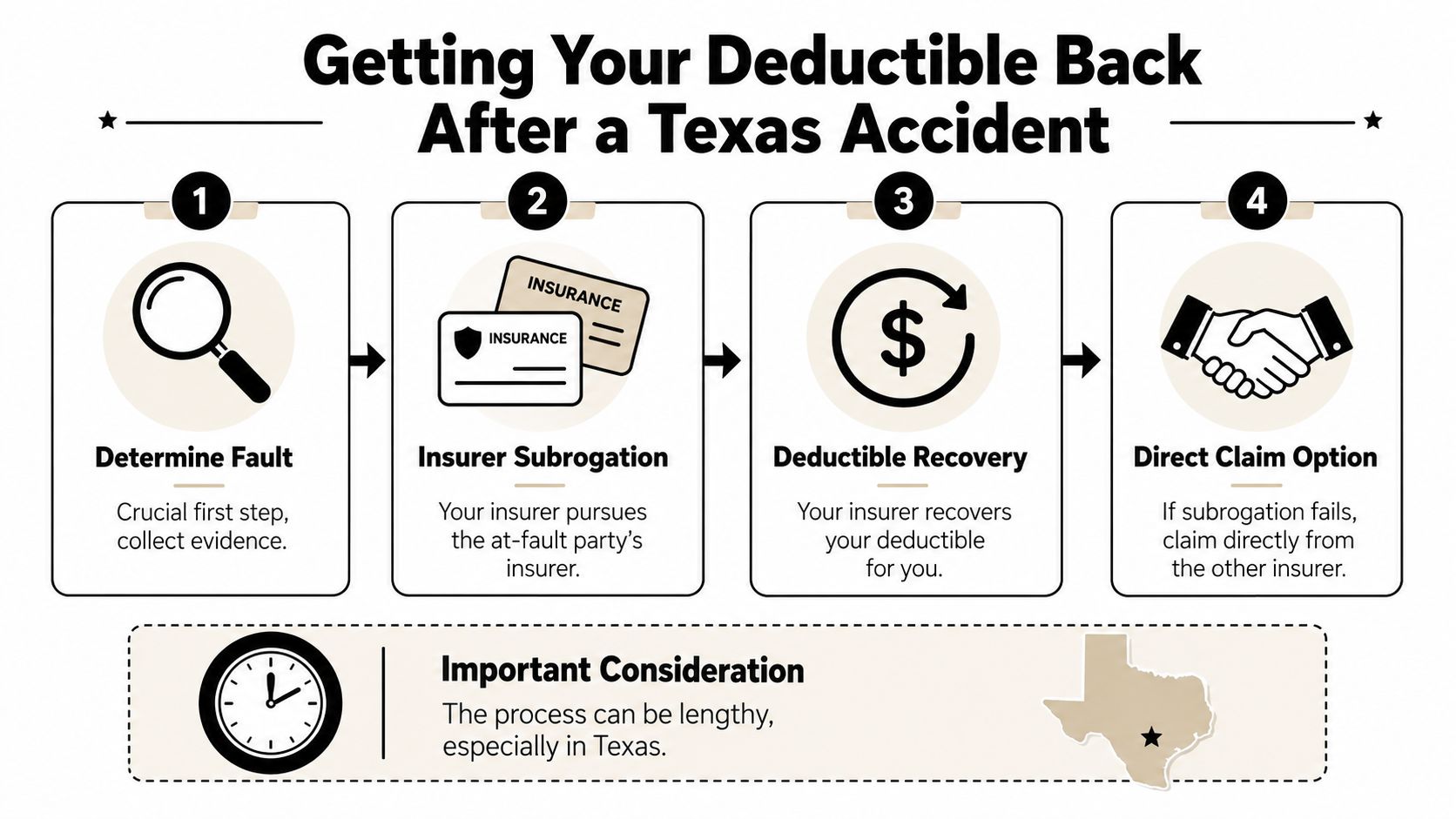

Three ways drivers usually recover a deductible

The other insurer pays it directly

If the at-fault driver's insurer accepts liability early, it may pay the property damage claim from the start. In that situation, you may not need to open a collision claim under your own policy.Your insurer pursues subrogation

Subrogation means your insurer tries to recover what it paid from the at-fault driver or that driver's insurance company. If your insurer gets paid back, your deductible is often included in that recovery.You bring a legal claim

If liability stays disputed, or the other side refuses fair payment, your deductible can become part of a larger claim for property damage or personal injury against the person who caused the wreck.

Subrogation sounds technical, but the idea is simple. It works like reimbursement after someone else covered a bill that should have been paid by the person who caused the problem. Your insurer pays first so repairs can begin. Then it tries to collect from the responsible party.

Here's a short explainer if you want to hear the issue discussed visually:

Why deductible recovery gets stuck in Texas

The delay usually comes down to fault. The other insurer may argue that you changed lanes without warning, followed too closely, or shared blame in some other way. Once that happens, your deductible refund can slow down or disappear unless the dispute gets resolved.

Texas uses a modified comparative fault system under Texas Civil Practice & Remedies Code Chapter 33. In plain language, fault can be divided between both drivers. If you were partly responsible, your recovery can be reduced by that percentage. If you are found more than 50 percent responsible, you generally cannot recover damages from the other side.

That rule matters because a deductible is still money you lost because of the crash. If the liability decision changes, your right to get that money back can change with it.

A real-world example of how the process plays out

A driver in Harris County is rear-ended in stop-and-go traffic. The damage is bad enough that the car has to go to the shop, and the driver needs it back quickly to keep getting to work. The other insurer says it is still investigating because its insured claims several vehicles were involved. To avoid more delay, the driver uses collision coverage and pays the deductible.

Weeks later, the liability decision is still unresolved.

At that point, the deductible is no longer just a line item on a repair estimate. It becomes part of the driver's total losses. In legal terms, those losses are called damages. Depending on the case, damages may include vehicle repairs, diminished value, medical bills, lost income, pain and suffering, and in fatal cases, wrongful death damages for surviving family members.

If your own insurer is pursuing subrogation, ask for updates in writing. Ask whether liability has been accepted, whether a demand has been sent, and whether your deductible will be refunded on a pro rata basis if the recovery is partial. Those details matter. A partial recovery can mean only part of the deductible comes back.

Sometimes subrogation works. Sometimes it stalls for months. Sometimes the at-fault driver is uninsured or does not carry enough coverage, which creates a different set of problems under underinsured motorist coverage in Texas.

You also want to keep every document tied to the vehicle claim, including photos, the crash report, repair invoices, proof of deductible payment, and messages from both insurers. If the vehicle later becomes a total loss or you have to shop for a replacement, title history can create another expensive surprise. Before buying another car with settlement funds, review the risks of buying a salvage title car.

If the other side keeps disputing fault and your deductible remains unpaid, legal counsel may be appropriate. The Law Office of Bryan Fagan, PLLC handles Texas motor vehicle injury matters, including disputes over crash liability and insurance recovery.

Deductibles in Total Loss and Uninsured Motorist Claims

A common Texas claim problem looks like this. Your car is so badly damaged that the insurer declares it a total loss, or the driver who hit you has no usable coverage, and you expect the deductible issue to clear up quickly. Instead, your own insurer pays under your policy, subtracts your deductible, and then the fight over who was at fault keeps that money tied up for months.

That is the part many drivers do not see coming.

When the car is a total loss

A total-loss claim works differently from a repair claim. Instead of paying a body shop bill, the insurer decides what your vehicle was worth right before the crash and applies the policy terms to that amount. If collision coverage is paying, your deductible is usually taken out of the settlement.

That can feel backwards. There is no repair invoice in your hand, no parts list, no labor charge. But the deductible still applies because it is your share of the loss under the policy, whether the car is fixed or replaced with a cash payment.

The next question is the one that matters in real life. Can you get that deductible back?

Sometimes yes, but only after your insurer recovers from the at-fault driver's carrier through subrogation, or after you pursue the at-fault driver in a claim or lawsuit if liability remains disputed. In Texas, deductible recovery often turns on proof. If the other insurer argues that you caused the crash, or even that you were partly at fault, your reimbursement can be delayed, reduced, or denied.

If you use settlement money to buy another vehicle, watch the title history closely. A lower sticker price can hide expensive problems later. Before buying one, review the risks of buying a salvage title car, especially if you are trying to make limited funds stretch after a wreck.

Uninsured motorist and underinsured motorist issues

When the other driver has no insurance, or too little insurance to cover the loss, your own policy may become the practical source of payment. These cases often involve uninsured motorist or underinsured motorist coverage. As noted earlier, underinsured motorist coverage in Texas can become a second track for recovery when the at-fault driver cannot fully pay for the harm caused.

That does not always mean your deductible problem disappears. The answer depends on the kind of claim, the wording of your policy, and whether your insurer later succeeds in recovering from the responsible party. Clients are often surprised by this. They assume that if the crash was clearly someone else's fault, their deductible should return automatically.

Insurance does not always work that neatly. If liability is disputed, your insurer may pay first and sort out fault later. Until that happens, you may be the one floating that money.

The fine print on zero-deductible offers

“Zero deductible” is a narrow promise, not a blanket promise.

It may apply to one part of the claim but not another. It may remove your out-of-pocket cost for certain vehicle damage, while leaving fights over rental bills, excluded damage, storage charges, or other losses untouched. It also does not guarantee that the insurer agrees with your version of how the crash happened.

That distinction matters in Texas deductible disputes. If the at-fault driver's insurer denies liability, or claims you share fault, the missing deductible can still become part of a larger recovery fight. At that point, your options may include waiting for subrogation to play out, pressing the liability carrier directly, or folding the deductible into a broader personal injury or property-damage claim.

Ask direct questions. What part of the loss is subject to no deductible? What part is still contested? If your insurer later recovers only part of the money from the at-fault side, ask whether your deductible refund will also be only partial.

Steps to Protect Your Claim and Your Rights

You don't need to know every insurance term at the crash scene. You do need to protect the evidence that helps prove fault and supports reimbursement later.

What to gather and keep

After a wreck, try to save the documents below in one folder, whether digital or paper:

- Police report information: Get the report number and the responding agency.

- Scene photos: Take pictures of all vehicles, debris, skid marks, road layout, and traffic signs.

- Repair records: Keep estimates, supplements, invoices, and messages from the shop.

- Proof of deductible payment: Save the receipt, credit card record, or written invoice showing you paid it.

- Insurance communications: Keep claim numbers, adjuster names, emails, and denial letters.

These details matter because deductible recovery often becomes an evidence problem. If an insurer later says it never received proof of payment or questions fault, your file becomes your advantage.

Know the legal terms that affect your case

A few legal phrases matter in almost every Texas auto insurance claim:

- Liability: Who is legally responsible for the crash.

- Comparative fault: Whether more than one driver shares blame under Texas law.

- Damages: The losses you're asking to be paid back for, such as repair costs, medical bills, lost wages, and pain and suffering.

- Statute of limitations: The legal deadline to file a lawsuit. In Texas, personal injury claims generally have a two-year deadline.

That last term is easy to ignore when you're focused on repairs. Don't ignore it. Waiting too long can weaken or even block your claim.

Dealing with adjusters without hurting your case

Insurance adjusters may sound friendly, but their job is still to evaluate and limit what the company pays. Be polite. Be careful. Stick to the facts.

A few practical habits help:

- Answer carefully: Don't guess about speed, distance, or fault.

- Read before signing: Don't sign broad releases unless you understand what rights you're giving up.

- Ask for it in writing: If an adjuster denies reimbursement, ask for the reason in writing.

- Get help early if things turn: This becomes more important if injuries, disputed fault, or lost income are involved.

For a fuller walkthrough, this article on how to deal with insurance adjusters is a useful next step.

Frequently Asked Questions About Collision Deductibles

Do I have to pay my deductible if the crash wasn't my fault

Often, yes. If you use your own collision coverage to repair your vehicle before the other insurer accepts liability, you'll usually need to pay your deductible first. Then you seek reimbursement through the insurance process, subrogation, or a legal claim.

This is one of the most common points of confusion in any auto insurance claim.

Who do I actually pay the deductible to

Usually, you pay it as part of the repair process. In many cases, that means the body shop collects the deductible when repairs are complete and the insurer pays the remaining covered amount under the claim arrangement.

Always get a receipt. If you later try to recover that money, proof of payment matters.

What if I can't afford my deductible

Talk with the repair shop about timing and payment options. Some shops may discuss practical ways to handle the payment schedule, but you should be cautious with any suggestion that sounds like the deductible will easily disappear.

If your crash caused injuries, time away from work, or major financial pressure, it may make sense to speak with a Houston car accident lawyer or Texas injury attorney sooner rather than later. The deductible may be only one piece of a larger damages claim.

Can an attorney help me recover my deductible

Yes. An attorney can help in several ways.

First, a lawyer can gather the evidence needed to prove liability and push back when the other insurer delays or denies fault. Second, the deductible can be included as part of a larger claim for damages. Third, if you're being blamed unfairly under Texas comparative fault rules, a lawyer can challenge that position before it reduces your recovery.

That matters even more in severe injury cases and fatal crashes involving wrongful death compensation. The property damage issue may be the first thing you notice, but it's often not the only thing you've lost.

If you're stuck between two insurance companies, getting conflicting answers, or paying out of pocket for a crash you didn't cause, legal guidance can take that burden off your shoulders and help you make decisions from a stronger position.

If you were hurt in a wreck and you're struggling with a deductible dispute, fault denial, or an insurance delay, The Law Office of Bryan Fagan, PLLC offers a free consultation for Texas accident victims and families. You can speak with a Houston car accident lawyer about your auto insurance claim, your rights under Texas law, and whether you may be able to recover your deductible along with other damages. You don't have to sort through this alone.