A car crash can change your life in seconds—but you don’t have to face recovery alone. When another driver’s mistake on a Texas road leaves you with serious injuries, the last thing you want to hear is that they only carry the bare minimum insurance. Suddenly, a mountain of medical bills and lost wages seems impossible to overcome. Their insurance won't even scratch the surface.

This is a terrifyingly common nightmare. It feels deeply unfair that someone else's negligence and poor financial planning could derail your life. How are you supposed to pay for everything?

Your Financial Shield After a Serious Texas Car Accident

Imagine getting into a major wreck on a packed Houston highway. The recovery is long, the medical bills are piling up, and you can't work. Then comes the gut punch: the driver who hit you has a policy that barely covers a fraction of your costs. This is where a difficult situation turns into a full-blown financial crisis for too many Texas families.

You're left wondering how you’ll ever get back on your feet when the person responsible for your pain can't cover the damage they caused.

What Is Underinsured Motorist Coverage?

This exact scenario is why Underinsured Motorist (UIM) coverage exists. It’s an optional but critical part of your own auto insurance policy, designed specifically to protect you from this kind of shortfall. Think of it as a safety net that you buy for yourself.

When the at-fault driver's insurance runs out, your UIM coverage kicks in to cover the remaining costs—up to the limits you selected for your own policy.

UIM coverage isn't about the other driver—it's about protecting yourself and your family. It ensures a negligent driver's poor insurance choices don't get to dictate your financial future.

This guide will walk you through exactly how this crucial coverage works here in Texas. Understanding your rights is the first step toward reclaiming your life after a crash. We'll show you how UIM can be your best defense against the financial devastation a serious car accident can cause.

Navigating the claims process can be complex, and a Houston car accident lawyer can make sure your rights are protected every step of the way. When your future feels uncertain, you don’t have to face it alone.

Understanding Underinsured Motorist Coverage in Texas

So, what exactly is Underinsured Motorist (UIM) coverage? Let's break it down in plain English. Imagine the at-fault driver's insurance policy is like a small bucket of water trying to put out a massive house fire. It might help a little, but it's nowhere near enough to cover the devastating costs of your injuries.

Your UIM coverage is the large water reserve you wisely set aside for yourself. It’s designed to kick in and cover the financial gap between your total losses and the other driver’s tiny policy limits, all the way up to the amount of coverage you purchased for yourself.

What UIM Covers After a Crash

When we talk about your losses, or “damages” in legal terms, we mean much more than just the first stack of hospital bills. Damages are the full measure of everything you have lost because someone else was careless.

Your UIM coverage is there to help pay for a wide range of these very real costs, including:

- Medical Expenses: This covers everything from the ambulance ride and ER visit to surgeries, ongoing physical therapy, and any future medical care you might need.

- Lost Wages: If your injuries have you out of work, UIM can compensate you for the paychecks you've missed.

- Diminished Earning Capacity: For serious injuries that permanently impact your ability to earn a living, this helps cover that long-term financial hit.

- Pain and Suffering: This is compensation for the physical pain and emotional trauma you've been forced to endure because of the accident and your injuries.

These are the real, and often overwhelming, consequences of a bad crash. Your UIM policy is a critical tool to help make you whole again.

UIM Coverage vs. At-Fault Driver's Liability Insurance

It's easy to get these two confused, but they play very different roles. The at-fault driver's insurance is meant to pay for the harm they caused others. Your UIM coverage is a safety net you buy to protect yourself when their policy isn't enough.

This table breaks down the key differences:

| Coverage Feature | At-Fault Driver's Liability Insurance | Your Underinsured Motorist (UIM) Coverage |

|---|---|---|

| Who It Protects | You (the victim) and other injured parties, up to the policy limit. | You and your passengers, when the at-fault driver's insurance is insufficient. |

| Who Buys It | The driver who caused the accident. | You, as part of your own auto insurance policy. |

| When It Applies | When the policyholder is legally responsible for causing the accident. | After the at-fault driver's liability insurance has been completely paid out, but your damages still aren't fully covered. |

| Primary Goal | To cover the damages the at-fault driver is legally obligated to pay. | To fill the financial gap between your total damages and the at-fault driver's low policy limits. |

Simply put, their insurance is the first line of defense. Yours is the essential backup plan that steps in when their defense crumbles.

The Key Difference Between UM and UIM Coverage

You’ll often see UIM coverage bundled with Uninsured Motorist (UM) coverage, but they handle two different—and equally frustrating—scenarios. While both are there to protect you, it's vital to know the distinction. We dive deeper in our guide to Uninsured Motorist coverage in Texas, but here’s a quick breakdown:

- Uninsured Motorist (UM): This kicks in when the at-fault driver has no insurance at all.

- Underinsured Motorist (UIM): This applies when the at-fault driver has insurance, but their policy limits are too low to cover all your damages.

Picture a multi-car pileup on I-10 in Houston. The driver who caused it might only carry Texas's minimum liability coverage of $30,000 per person. If three people are seriously hurt with medical bills over $100,000 each, that minimum policy gets wiped out almost instantly. This is precisely where your own UIM policy becomes your most powerful lifeline for financial recovery.

Why This Coverage Is So Important in Texas

This isn't just a theoretical problem; it’s a daily reality on Texas roads. Think about a San Antonio family shattered by a head-on collision caused by a distracted driver. Their medical bills are astronomical, but the at-fault driver only has the state-minimum insurance. UIM coverage is what steps in to bridge that enormous financial gap.

Sadly, a shocking number of Texas drivers are underinsured. Recent data shows that nationally, the combined rate of uninsured and underinsured drivers hit a decade-high of 33.4% in 2023. You can see more of these alarming trends from the Insurance Research Council. This statistic underscores just how vulnerable you are without your own UIM protection. Your financial well-being should never depend on another driver’s poor choices.

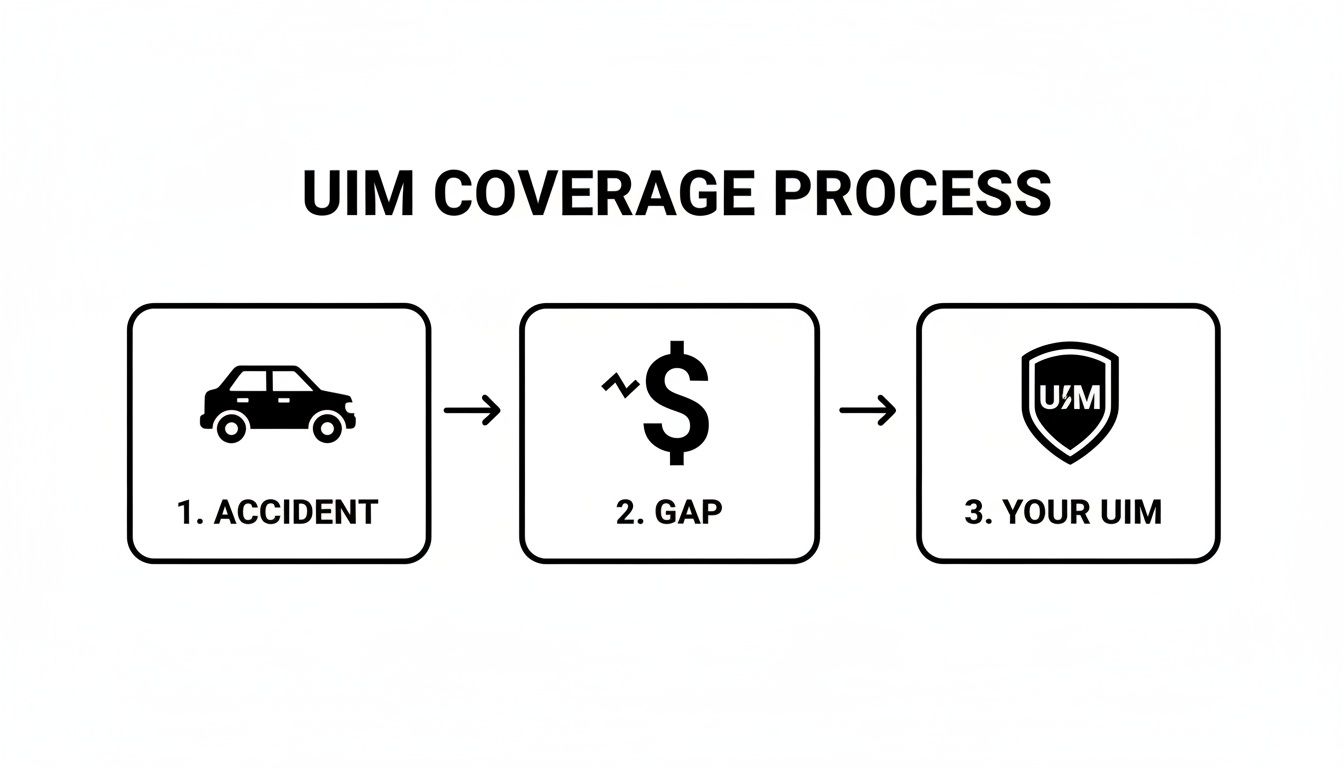

Steps to File an Insurance Claim in Texas

Filing a claim for your Underinsured Motorist (UIM) benefits can feel like staring up at a mountain. It’s intimidating, but knowing the right path to take makes all the difference. This isn’t just about filling out forms; it’s about timing, strategy, and protecting your right to get the compensation you truly deserve.

The flowchart below gives you a bird's-eye view of how a UIM claim works. Think of it as your UIM coverage stepping in to build a financial bridge where the other driver's insurance falls short.

As you can see, the journey starts with the accident, moves to identifying that coverage gap, and ends with your own policy acting as the financial shield you paid for.

Your Step-by-Step Guide to Filing a UIM Claim

Every car wreck is different, but the fundamental steps for a successful UIM claim in Texas follow a specific sequence. Getting one of these steps wrong can put your entire claim in jeopardy, which is exactly why having an experienced Texas injury attorney in your corner is so critical.

Here’s a practical roadmap of what the process looks like:

- Get Medical Help Immediately: Your health comes first, always. Seeing a doctor right after the crash doesn't just start your physical recovery; it creates an official medical record connecting your injuries to the accident. This paperwork is crucial evidence.

- Report the Crash and Notify Insurers: Call the police to get an official accident report. You also need to promptly let both the at-fault driver's insurance company and your own carrier know about the accident and that you plan to file a claim.

- Gather Every Piece of Evidence: A strong claim needs a strong foundation. That means collecting the police report, photos from the scene, pictures of your injuries, any witness information you can get, and every single medical bill and record related to your treatment.

- Settle with the At-Fault Driver's Insurance First: Before you can tap into your UIM coverage, you have to go through the other driver's policy. The goal here is to get them to offer you a settlement for their full policy limit.

This first step is what officially proves the other driver was "underinsured"—it demonstrates that their coverage wasn't enough to cover your total damages.

The Most Critical Step: Permission to Settle

Before you even think about accepting a settlement offer from the at-fault driver's insurer, you must get written permission from your own insurance company. This is, without a doubt, the most important and most frequently missed step in the entire UIM process.

Why does it matter so much? When your insurance company pays out on a UIM claim, they get the right to go after the at-fault driver to get their money back. This is called subrogation. If you settle without their permission, you’ve just signed away their right to do that, and they can legally—and will—deny your UIM claim completely.

Never, ever accept a settlement from the at-fault driver’s insurance without getting written consent from your own UIM carrier first. It’s a mistake that could cost you every penny of your UIM benefits.

Submitting Your UIM Demand and Fighting for Fair Value

Once you have that permission slip in hand and have settled with the other driver's insurer, it’s time for round two. You or your attorney will put together a formal demand package for your own insurance company. This packet lays out all your damages—medical costs, lost income, pain and suffering—and formally demands payment under your UIM policy.

This is often the point where your insurance company, which you've paid faithfully for years, suddenly feels more like an opponent. Their adjusters will pick apart your claim, looking for any reason to pay you less. They might challenge how bad your injuries are or argue that some of your medical treatments weren't necessary.

An experienced Houston car accident lawyer has seen these tactics a thousand times. We know how to build a case that they can't ignore, backing up our demands with solid evidence. We handle the frustrating back-and-forth, fighting for the full value of your claim. And if they refuse to be fair? We won't hesitate to file a lawsuit and take them to court. You've been through enough—let us take on the fight for you.

How to Calculate the Value of Your UIM Claim

Figuring out what your claim is really worth is the first and most important step toward getting a fair recovery. After a serious accident, it’s never just about the first hospital bill. It's about understanding the full financial, physical, and emotional toll the crash has taken on your life. This total amount is what we call “damages” in a personal injury claim.

Pulling that number together is a detailed process. It means adding up every single cost and loss you’ve had to bear because someone else was negligent behind the wheel.

Defining Your Total Damages

To make sure nothing gets missed, we break down your damages into two main categories. Think of these as the building blocks of your entire claim.

- Economic Damages: These are the straightforward, calculable financial hits. This bucket includes all your medical bills (what you've already paid and what you'll need in the future), lost income from being out of work, and the cost of any long-term care or rehab.

- Non-Economic Damages: These are the losses that don't come with a receipt but are just as real and devastating. This is compensation for your physical pain and suffering, emotional distress, mental anguish, and the loss of enjoyment of life.

A Texas injury attorney will often work with medical and financial experts to put a precise dollar amount on these damages, ensuring no stone is left unturned. That final figure represents what you are legally entitled to recover.

A Real-World UIM Calculation Example

Let's walk through a real-world example to show how UIM coverage actually works.

Imagine a Dallas driver gets T-boned at an intersection by a driver who ran a red light. The crash leaves them with serious injuries needing surgery and months of physical therapy. After a thorough evaluation of all their losses, their total damages are calculated to be $250,000.

Now, the driver who caused the wreck only has Texas's minimum liability insurance, which is just $30,000 per person for bodily injury.

Here’s how the math plays out:

- Total Damages: $250,000

- At-Fault Driver’s Policy Limit: $30,000

- The Shortfall: $250,000 – $30,000 = $220,000

The at-fault driver's insurance pays its full $30,000, but that leaves a staggering $220,000 gap. This is the exact moment your own UIM coverage is supposed to kick in and cover that remaining amount, as long as your UIM policy limits are at least $220,000.

In Texas, your UIM coverage pays the difference between your total damages and the amount paid by the at-fault driver's liability policy, up to your own UIM policy limit.

This is why choosing high UIM limits is so critical—it directly determines your ability to be made whole after a life-altering crash. With the number of underinsured drivers on our roads climbing, this protection is more important than ever. In fact, a recent study showed one in three U.S. drivers (33.4%) were uninsured or underinsured in 2023, a big jump from 2017. You can read the full research about these motorist trends to see just how big the risk has become.

The Impact of Comparative Fault in Texas

There's a Texas law you need to know about called comparative fault, sometimes called proportionate responsibility. This rule, found in Chapter 33 of the Texas Civil Practice & Remedies Code, examines whether you were partially to blame for the accident.

If a jury decides you were 10% at fault for the crash, your total compensation gets cut by 10%. In our example, a $250,000 award would be knocked down to $225,000. And here's the really harsh part: if you are found to be 51% or more at fault, Texas law says you get nothing at all.

Insurance companies love to use this rule to try and shift blame onto you, even when it's not deserved, just to lower what they have to pay. A skilled Houston car accident lawyer knows these tactics and will fight back hard against baseless accusations, working to prove the other driver was fully responsible for your injuries. Don’t let an insurance adjuster bully you—we’re here to protect your right to a full and fair recovery.

Common Mistakes and Insurance Company Tactics to Avoid

When you file an underinsured motorist claim, the whole dynamic with your insurance company flips. It can be a jarring experience. The company you’ve been paying premiums to every single month suddenly isn’t on your side anymore. You're now in a negotiation against them, and their goal is simple: protect their bottom line by paying you as little as possible.

Knowing their playbook—and the common mistakes people make—is your first line of defense in protecting your right to fair compensation.

Never Give a Recorded Statement Without Legal Advice

It won’t take long for an adjuster from your insurance company to call. They’ll likely ask for a recorded statement, framing it as a routine, necessary step. Don't be fooled. This is a strategic move designed to dig up anything they can use against you.

It's shockingly easy for your words to be twisted or taken out of context. An innocent comment like, "I'm feeling a bit better today," can be used down the road to argue your injuries aren't as bad as you claim. The best response is to politely decline until you've spoken with a Houston car accident lawyer.

Be Wary of Early Settlement Offers and Signing Documents

If the insurance company quickly slides a settlement offer your way, that’s a massive red flag. They know you're feeling the financial and emotional strain after an accident. They’re banking on you accepting a lowball amount out of sheer desperation. These first offers almost never cover the full, long-term costs of your injuries.

Along the same lines, never sign any release forms or waivers without having a lawyer review them first. You could be unknowingly signing away your rights to any future compensation, including for medical problems that haven't even surfaced yet.

An insurance adjuster's primary job is to resolve your claim for the lowest possible cost to the company. They are not there to ensure you receive what is fair—they are there to protect their profits.

This is a harsh truth, but it’s critical to understand, especially when you see how many drivers are on the road without enough coverage. A 2023 report from the Insurance Research Council found that a staggering 33.4% of U.S. drivers were either uninsured or underinsured, a number that has shot up in recent years. You can discover more insights about these alarming motorist trends on carriermanagement.com. This statistic shows exactly why your UIM claim is so vital—and why your insurer will fight so hard to minimize what they have to pay you.

Common Tactics Insurers Use to Devalue Your Claim

Insurance companies have a whole playbook of tactics designed to reduce or outright deny legitimate UIM claims. Knowing what to expect helps you and your attorney build a much stronger case. Their strategies often include:

- Delaying the Process: They might drag their feet on the investigation, ignore your calls, or ask for the same documents over and over. The goal is to wear you down with frustration until you accept a low offer just to be done with it.

- Disputing Your Medical Needs: The adjuster may try to argue that some of your medical treatments weren't necessary or that the bills were unreasonable.

- Blaming Pre-existing Conditions: They will comb through your medical history, looking for any old injury or condition they can blame for your current pain, even if it has no connection.

- Conducting Surveillance: It’s not unheard of for insurers to hire private investigators to watch you or monitor your social media. They are looking for a single photo or post that contradicts your injury claims.

When an insurer uses these tactics unreasonably, they can cross a legal line into acting in "bad faith." You can learn more about what constitutes a bad faith insurance claim in our article to get a better handle on your rights. At The Law Office of Bryan Fagan, we see these moves coming. We build a powerful, evidence-based case to shut them down, making sure you aren't taken advantage of when you're most vulnerable.

Why You Need a Texas Car Accident Lawyer for Your UIM Claim

It’s a tough reality to face, but filing an underinsured motorist (UIM) claim isn't just about paperwork. It's a complex legal fight against your own insurance company—a massive corporation with a team of adjusters trained to protect their bottom line, not yours.

Trying to handle this on your own, especially while you’re recovering from serious injuries, puts you at a huge disadvantage. An experienced Houston car accident lawyer doesn't just help; they level the playing field. You've been through enough. Let us take on the legal battle so you can focus on what matters: your health and your family. Your fight becomes our fight.

We Manage the Entire Process for You

From the moment you hire us, we take the weight off your shoulders. We’ll handle every single phone call and email with the insurance adjusters, who are professional negotiators looking for any reason to reduce your payout.

Our team takes full control of the claim from start to finish. This frees you from the constant stress of looming deadlines and invasive requests for information. We know the tactics they use, and we come prepared to shut down every attempt they make to devalue your auto insurance claim.

Building a Case for Maximum Compensation

A successful UIM claim requires so much more than just a stack of medical bills. It demands a powerful, evidence-backed case proving the true, full extent of your damages. This is where an experienced Texas injury attorney is absolutely critical.

Here’s a glimpse of how we build your case for you:

- Digging Deep with a Detailed Investigation: We go beyond the initial police report. We track down witnesses, gather physical evidence, and piece together exactly how the accident happened and how severe it was.

- Bringing in the Experts: To accurately value your claim, we often work with respected medical specialists, accident reconstructionists, and financial experts. They help us calculate everything from your future medical costs to your lost earning potential.

- Negotiating from a Position of Strength: Armed with indisputable evidence, we don’t just ask for a fair settlement—we demand it. We force the insurance company to recognize the true value of what you’ve lost.

Understanding your rights is key, and we are committed to making sure you have all the information you need.

Remember, your insurance company has an entire legal team protecting their interests. You deserve to have a dedicated advocate fighting just as hard for yours.

We are always prepared to take your case to court if the insurance company refuses to make a fair offer. While many law firms shy away from trial, we are seasoned litigators who will not back down.

Our firm operates on a contingency fee basis, which means you pay us absolutely nothing unless we win your case. There is zero financial risk to you. If you're curious about the first steps, this Complete Guide Law Firm Client Intake offers a great overview of how law firms get started with new clients.

Contact us today for a free, no-strings-attached consultation to discuss your case and your rights.

Frequently Asked Questions About Texas UIM Coverage

When you're trying to figure out your rights after a car wreck, it's completely normal to have a ton of questions. We've been there with countless clients, and we've gathered the most common questions people ask about underinsured motorist (UIM) coverage right here in Texas. Our goal is simple: give you clear, straightforward answers so you can make the best decisions for yourself and your family.

How Much UIM Coverage Should I Really Have in Texas?

This is probably the most critical question you can ask before an accident happens. While there isn't a magic number that fits everyone, here’s a solid rule of thumb we always recommend: match your UIM coverage limits to your own liability coverage limits.

Think about it this way: if you carry a $100,000/$300,000 liability policy to protect other people if you cause a crash, shouldn't you have the same level of protection for yourself? Having that same amount for your UIM coverage ensures you have a real safety net if you're seriously hurt by a driver who chose to carry only the bare-minimum insurance required by law.

Can I Use My UIM Coverage if I Was a Passenger or a Pedestrian?

Yes, you absolutely can. This is a powerful feature of UIM coverage that catches many people by surprise. In Texas, your UIM coverage is designed to follow the person, not just the car you're in.

This means you can file a claim under your own UIM policy if an underinsured driver hits you while you are:

- Riding as a passenger in your friend’s car.

- Out for a walk or a jog and get hit in a crosswalk.

- Riding your bicycle down the street.

This protection extends to you and any relatives living in your household, giving you a vital layer of financial security no matter how or where a collision happens.

What Happens if My Insurance Company Just Denies My UIM Claim?

Getting a denial letter can feel like a punch to the gut, but it is not the final word. If your own insurance company denies a valid UIM claim without a good reason, they may be acting in bad faith. That's a serious violation of the legal duty they owe you as their policyholder.

When this happens, you have every right to fight their decision. An experienced Texas injury attorney can step in and file a lawsuit against the insurance company for breach of contract and bad faith practices. Our job is to hold them accountable and force them to pay the benefits you are rightfully owed under the policy you paid for.

Will Filing a UIM Claim Make My Insurance Rates Go Up?

This is a huge fear, and it stops too many people from using the benefits they’ve been paying for month after month. The good news is that Texas law is very clear on this.

Under the Texas Insurance Code, your insurance company cannot legally raise your premiums for filing a UIM or UM claim as long as the accident was not your fault.

You paid for this coverage for this exact scenario. Don't let the fear of a rate hike stop you from getting the compensation you desperately need to recover. Understanding how underinsured motorist coverage works is the key to protecting your financial future after a crash.

You have been through more than enough. You shouldn’t have to fight the insurance company on your own. At The Law Office of Bryan Fagan, PLLC, our dedicated Houston car accident lawyers are here to handle every single detail of your UIM claim. We’ll make sure your rights are protected so you can get the full compensation you deserve.

Contact us today for a free, no-obligation consultation to find out how we can help.