A serious car crash can change your life in seconds—but you don’t have to face recovery alone. When you finally secure a settlement, you’re looking for relief, not another headache from the IRS. One of the first and most important questions our clients ask is, "Is my lawsuit settlement taxable?"

The short answer is: it depends. But the good news for accident victims is that money you receive for physical injuries and medical bills is generally not taxable under Texas and federal law. It’s the compensation for things like lost wages or punitive damages where the rules get a little more complicated.

Your Texas Settlement and Taxes: A Clear Guide

After surviving a major Texas car accident, dealing with the IRS is the last thing you should have to worry about. This guide will break down how your settlement funds are treated for tax purposes in a straightforward, easy-to-understand way, empowering you with the knowledge you need.

The core idea behind the tax law is to make you whole again without hitting you with an extra tax bill for your physical recovery. We'll explain the key IRS rules in plain English, helping you see the critical difference between compensation for physical losses versus economic ones. Getting this right is a vital step in protecting your financial future after a crash.

Who Is Liable in a Texas Car Accident?

Before we dive into taxes, it helps to understand a few key legal terms that will come up during your claim. In Texas, determining who is responsible for your injuries is based on the concept of liability, which simply means legal responsibility for causing the accident. This is usually determined by negligence—when a driver fails to act with reasonable care, causing harm to others.

Texas follows a comparative fault rule (Texas Civil Practice & Remedies Code § 33.001), which means your compensation can be reduced by your percentage of fault. For example, if you are found 10% at fault for a Houston car accident, your total damages would be reduced by 10%. However, if you are found to be more than 50% at fault, you cannot recover any damages at all.

Your damages are the monetary compensation you receive for your losses, which can include medical bills, lost wages, and pain and suffering. It's these damages that are subject to tax rules.

The Foundation of Settlement Taxation

The U.S. tax code has specific rules for personal injury awards. At its heart, the rule is simple: a settlement is taxable if it replaces income you would have earned, but it’s non-taxable when it compensates you for physical injuries or sickness.

Think of it this way: you never paid taxes on your physical health to begin with, so the money you get to restore it shouldn't be taxed either. It’s a matter of fairness. For instance, if a Houston driver is rear-ended on I-45, the funds covering their hospital bills and physical therapy are meant to restore what was lost—and are therefore tax-free.

However, other parts of a settlement are seen differently by the IRS:

- Lost Wages: This portion is usually taxable. Why? Because it directly replaces income you would have paid taxes on if you had been able to work.

- Punitive Damages: These are designed to punish the at-fault party for extreme negligence, as outlined in Texas Civil Practice & Remedies Code Chapter 41. Since they aren't meant to compensate you for a specific loss, they are almost always taxable.

To give you a clearer picture, here's a simple breakdown of how different types of compensation are typically treated.

Quick Guide to Settlement Taxability

| Type of Compensation (Damages) | Generally Taxable? | Reason |

|---|---|---|

| Physical Injuries/Sickness | No | Restores you to your pre-injury state; not considered income. |

| Medical Expenses | No | Reimburses you for direct costs of treatment related to the physical injury. |

| Emotional Distress | No (if from physical injury) | Considered part of the pain and suffering tied to the physical harm. |

| Lost Wages | Yes | Replaces income that would have been taxed if you had earned it. |

| Punitive Damages | Yes | Intended to punish the defendant, not to compensate you for a specific loss. |

| Interest on Settlement | Yes | Treated as investment income, separate from the actual compensation for injury. |

This table is a great starting point, but always remember that how your settlement is structured in the final agreement can make a huge difference.

Once you have a firm handle on your settlement's tax implications, you can start planning for the future. That might even include looking into how to invest a lump sum of money you’ve received. With the right legal and financial guidance, you can navigate these complexities with confidence.

Why Some of Your Settlement Money Is Tax-Free

After a car wreck, you’re not just dealing with physical pain. You’re facing emotional stress and a mountain of bills. When a settlement check finally arrives, it’s meant to help you put the pieces back together. The good news is, the IRS generally agrees with this idea.

The core principle is simple: personal injury compensation is meant to make you “whole” again. It’s a reimbursement for something you lost—your health—not new income you’ve earned. Since you never paid taxes on your physical well-being in the first place, the money you get to restore it isn't considered taxable.

The Law That Protects Your Recovery

This isn’t just a courtesy from the government; it’s written right into the tax code. Section 104(a)(2) of the Internal Revenue Code is the key. It specifically states that money you receive as compensation for “personal physical injuries or physical sickness” doesn’t count as part of your gross income.

This section is the legal bedrock that shields most of your car accident settlement from taxes. The law recognizes these funds aren't a lottery win. They are a critical part of your recovery, intended to cover the very real, and often staggering, costs of getting better.

Think about a common scenario right here in Texas. A driver gets rear-ended on I-45 in Houston and suffers a serious back injury. Their settlement is designed to cover things like:

- Hospital bills and emergency room visits

- The cost of surgery

- Ongoing physical therapy and rehab

- Medications and necessary medical equipment

Every dollar allocated for these costs is directly tied to the physical harm they suffered. Thanks to Section 104(a)(2), this money is tax-free because its purpose is to restore the victim’s physical health.

The goal of a personal injury settlement isn't to make you rich; it's to make you whole. The tax code supports this by exempting funds for physical harm, ensuring your recovery isn't cut short by a tax bill.

What Does the IRS Mean by "Origin of the Claim"?

When the IRS looks at a settlement, they want to know the origin of the claim. In plain English, they’re asking: "What was the fundamental reason you filed the lawsuit?" For a Texas car accident victim, the answer is almost always a physical injury.

This is a crucial distinction. Even if your claim includes other damages, like emotional distress, their tax treatment hinges on whether they flow directly from that initial physical injury. If the anxiety, sleepless nights, or PTSD you're experiencing is a direct result of the physical trauma from the crash, the compensation for that suffering is also typically non-taxable.

For example, say you’re battling post-traumatic stress disorder after a brutal T-bone collision in Dallas. The money you receive for that emotional anguish is tax-free because it’s a direct consequence of your physical injuries. It's all part of the same non-taxable package aimed at making you whole again.

Your Houston car accident lawyer will work to make sure your settlement agreement clearly spells this out, linking all compensation back to your physical injuries and the resulting pain and suffering. This helps protect the funds you need most.

Breaking Down Your Settlement: What the IRS Can and Can’t Touch

When you get a settlement check, it’s easy to think of it as one big lump sum for your trouble. But in the eyes of the law—and more importantly, the IRS—it’s actually a mix of different types of compensation called damages. Getting a handle on these categories is the key to knowing whether you'll owe taxes on your settlement.

Each type of damage gets treated differently. This is why a sharp Houston car accident lawyer will fight to structure your settlement agreement in a way that clearly defines each amount, a move that can make a huge difference in how much you actually get to keep.

Let's break down the common pieces of a Texas personal injury settlement.

Non-Taxable Damages: The Core of Your Recovery

Good news first. The biggest and most important chunk of your settlement is usually non-taxable. This is the money intended to compensate you for direct physical losses—to help make you whole again after the accident.

- Compensation for Physical Injuries and Sickness: This is the bedrock of the tax-free rule. Any funds specifically for your bodily harm—a broken leg, a traumatic brain injury, or the chronic pain from a rear-end collision—are not considered income by the IRS.

- Medical Expenses: This bucket covers every related medical cost you can think of. It includes repayment for the hospital stay, surgery, doctor visits, physical therapy, and prescriptions. It even covers the future medical care you’ll need because of what happened. Since this is just paying you back, it's not taxed.

- Pain and Suffering: This compensates you for the physical agony and emotional trauma that are directly tied to your physical injuries. Think of the daily misery from a severe burn or the constant ache from a spinal injury. As long as it grows out of a physical injury, it’s tax-free.

The logic is simple: this money isn't meant to make you rich. It's meant to restore what was taken from you. That's why the IRS keeps its hands off.

Taxable Damages: When Settlement Money Becomes Income

While the core of your settlement is protected, other parts are seen as income by the IRS and, you guessed it, are taxable. It’s absolutely critical to know which parts fall into this category so you aren’t hit with a surprise tax bill later.

The reasoning here is also straightforward: if the money replaces income you would have paid taxes on anyway, then the settlement money is also taxable. Likewise, if the money is seen as a financial gain rather than compensation for a loss, expect it to be taxed.

A settlement isn't a single pot of money; it's a carefully allocated fund where each part has a specific purpose. Clearly defining that purpose in the settlement agreement is one of the most important steps to protect your financial recovery from the IRS.

Here are the most common types of taxable damages in a personal injury claim:

- Lost Wages and Lost Earning Capacity: If your injuries forced you to miss work, part of your settlement will cover that lost income. Since your regular paychecks would have been taxed, this compensation is taxable, too. This applies to both the wages you’ve already lost and what you’re projected to lose in the future.

- Punitive Damages: In situations where the at-fault party’s behavior was particularly outrageous—like a drunk driver causing a catastrophic crash in Dallas—a court might award punitive damages. These aren't to compensate you for a loss but to punish the defendant. Because the IRS sees this as a windfall, it is always taxable.

- Interest on the Judgment: Sometimes there's a delay between when a judgment is awarded and when you actually get paid. Any interest that builds up during that time is treated just like interest from a savings account, making it taxable income.

The Gray Area: Emotional Distress

Emotional distress can be one of the trickiest parts of a settlement. Whether it’s taxed or not depends entirely on what caused it.

If your emotional distress—anxiety, depression, PTSD—is a direct result of your physical injuries, then the compensation for it is not taxable. For example, if you suffer from PTSD because of the trauma of the collision itself, that money is tied to your physical harm and stays tax-free.

However, if a claim is for emotional distress by itself, with no underlying physical injury, the IRS treats that money as taxable income. This is exactly why solid medical evidence connecting your mental state to your physical injuries is so critical for your case.

The exact wording in your settlement documents matters immensely. Money for lost wages is taxed as ordinary income, and punitive damages are fully taxable. Both the courts and the IRS will scrutinize the agreement to understand the real purpose behind each payment. When the allocation to physical injuries is clear and backed by medical records, it’s far more likely those funds will remain tax-free.

For a deeper dive into this topic, you can also explore our detailed guide on the taxation of settlement funds. Your attorney will play a crucial role in negotiating and writing this agreement to maximize the non-taxable parts of your award, making sure you keep as much of your hard-won compensation as possible.

The Critical Role of Settlement Agreement Language

When you're trying to figure out if your lawsuit settlement is taxable, the single most important document is the settlement agreement itself. This isn't just a piece of paper ending your claim; it's a financial roadmap that the IRS will follow to the letter. How the money is categorized—or allocated—within that document can be the difference between protecting your recovery and getting hit with a massive, unexpected tax bill.

A poorly worded agreement that’s vague about why you're being compensated is an open invitation for IRS scrutiny. On the other hand, a carefully drafted agreement is your best defense. A skilled Houston personal injury attorney will fight to allocate the maximum amount possible to non-taxable categories, primarily your "physical injuries and sickness" and the resulting "pain and suffering."

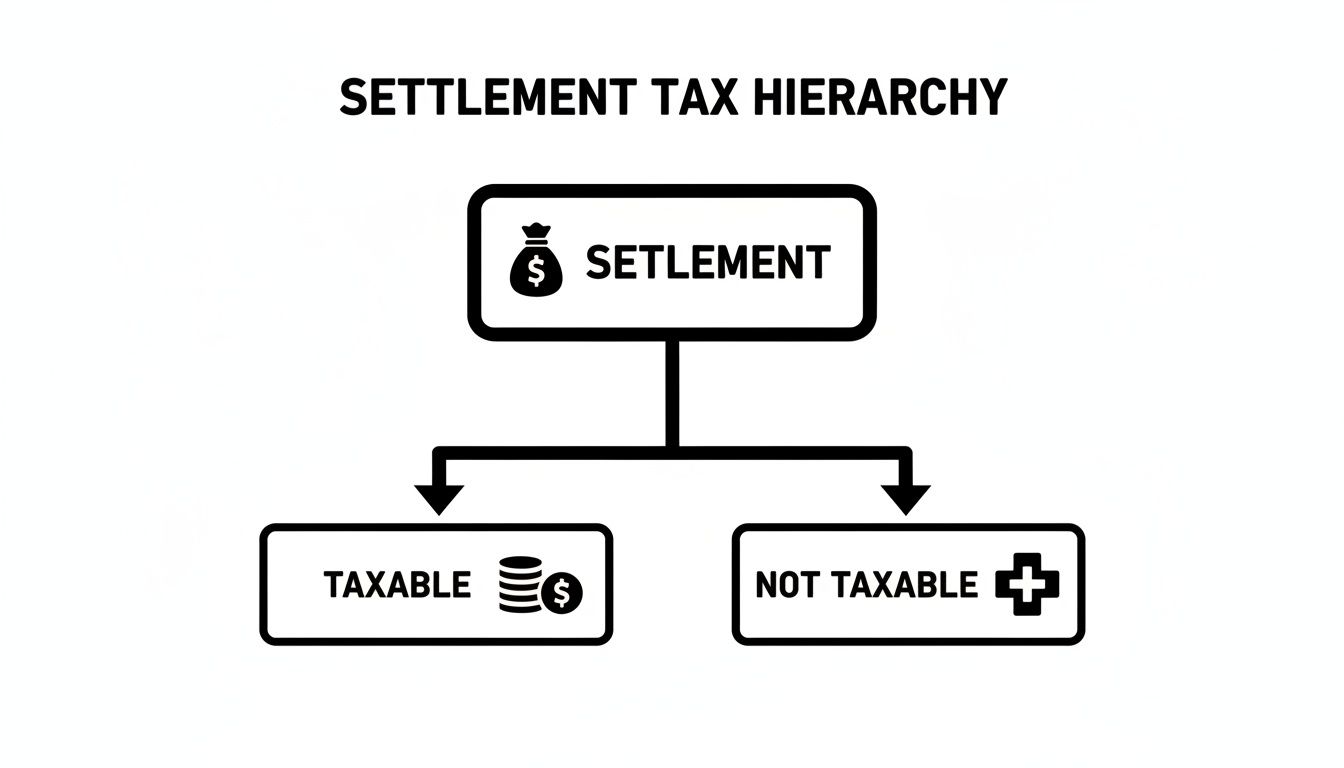

This infographic simplifies how a settlement is divided into taxable and non-taxable piles.

As you can see, all the funds start in one pool. They're only split after their legal purpose is defined, with compensation for physical injuries staying tax-free while economic replacements like lost wages become taxable.

How Words on a Page Change Your Tax Outcome

Let's imagine two people get into similar car accidents on a San Antonio highway. Both suffer identical injuries and, after their legal battles, each accepts a $300,000 settlement.

- Settlement A: The agreement is vague. It just says the money is for "all claims arising from the accident."

- Settlement B: The agreement is specific. It allocates $225,000 for physical injuries, medical bills, and pain and suffering, and $75,000 for lost wages.

The person with Settlement A is walking on thin ice. The IRS could easily challenge the entire amount, potentially deciding that a huge chunk of it is taxable. But the person with Settlement B has a clear, defensible position: only the $75,000 for lost wages is subject to income tax. The language made all the difference.

The negotiation of your settlement agreement isn't just about the final dollar amount. It's about strategically defining what each dollar is for, creating a legal and financial shield that protects the money you need most.

The High Cost of a Poorly Drafted Agreement

The financial stakes here are incredibly high. A single mistake or unclear phrase in the settlement language can lead to devastating tax consequences. This isn't just a hypothetical risk; it's a reality that has been proven time and again in tax court.

For instance, tax professionals often point to real-world cases where vague wording led to disaster. In one notable case, a settlement of over $1.5 million was structured in a way that drew intense IRS scrutiny. The IRS ultimately argued the plaintiff owed more than $588,000 in back taxes and penalties, partly because the agreement failed to clearly allocate the funds and properly account for attorney fees. You can discover more insights about how settlement language can create six-figure tax problems from legal analyses of these court cases.

This is exactly why having a Texas injury attorney who understands tax implications isn't a luxury—it's essential. We work tirelessly to ensure the language in your final agreement is precise, legally sound, and structured to minimize your tax liability, safeguarding the financial stability you fought so hard to win back.

Navigating Attorney Fees and IRS Reporting

Figuring out how your attorney's fees and the inevitable IRS paperwork fit into your settlement can be one of the most confusing parts of the whole process. It's a common headache for accident victims, but once you understand how the system works, it’s much less intimidating.

Here’s the part that trips most people up: the IRS often looks at the gross settlement amount first. That’s the total number before any money is taken out for legal fees or other costs. Even though your Houston car accident lawyer gets paid directly from the settlement funds, the government initially sees that entire lump sum as potential income for you.

Understanding the Form 1099

Sometime after your case wraps up, you'll almost certainly get a tax form in the mail from the defendant’s insurance company. It's usually a Form 1099-MISC or Form 1099-NEC, and the number on it will likely be the entire settlement amount.

It’s absolutely critical that you don't ignore this document. But its arrival doesn't mean you owe taxes on the whole thing. Think of the 1099 as the start of a conversation with the IRS, not the final word. It just reports the payment; it's your job to explain what that payment was for.

Receiving a Form 1099 for your full settlement can be alarming, but it's standard procedure. It simply means you must account for the funds on your tax return, separating the non-taxable portions from any taxable amounts.

How to Properly Account for Your Settlement

Your tax return is where you set the record straight. You have to report the total amount shown on the 1099 and then legally subtract the parts that aren't taxable. This is exactly why having a well-drafted settlement agreement that breaks down the funds is so important.

Here’s a simplified look at how it works:

- Report the Gross Amount: Start by reporting the total figure from the Form 1099.

- Subtract Non-Taxable Damages: Next, you'll deduct the portion allocated to your physical injuries, medical bills, and related pain and suffering.

- Account for Attorney Fees: You may also be able to deduct the attorney fees paid out of the taxable portion of your settlement, like the fees associated with recovering lost wages or punitive damages.

The rules for deducting legal fees can get tricky, which is why getting professional help is key. For a clearer picture of how fees work, you can learn more about how much lawyers typically take from a settlement and how that structure is set up.

Because the tax code is so specific, we always urge our clients to have both their personal injury attorney and a qualified tax professional in their corner. This dual-expert approach ensures everything is reported correctly, protecting you from future IRS audits, penalties, or unnecessary stress. Your focus should be on your recovery, not fighting a tax battle that could have been avoided.

How a Texas Personal Injury Lawyer Protects Your Settlement

Getting through a serious accident is tough enough. The last thing you need is to face a tangled financial and legal battle on your own. This is where an experienced Houston personal injury attorney proves their worth. A good lawyer does so much more than just fight for a big check—they protect the money you'll need to rebuild your future.

At The Law Office of Bryan Fagan, our job includes strategically structuring your settlement to be as tax-efficient as possible. Here in the U.S., anyone receiving a settlement—including Texas auto-accident victims—has to figure out how to report that money to the IRS. Since most settlements are a mix of taxable and non-taxable funds, our deep understanding of the rules is absolutely essential.

Strategic Guidance From Day One

From the very first day you hire us, our mission is to protect both your legal rights and your financial recovery. We get to work immediately, meticulously documenting how every part of your ordeal—from the physical pain to the emotional trauma—is a direct result of your physical injuries. This groundwork is crucial for building the legal foundation to classify the largest possible portion of your settlement as non-taxable.

A critical, often overlooked, part of a lawyer's duty is maintaining airtight security for your private information. We follow a strict law firm data security guide to ensure your sensitive case details and settlement information are safeguarded every step of the way.

Masterful Negotiation and Drafting

Negotiating and drafting the final settlement agreement is where the magic really happens. The language in this document has to be exact. We fight to make sure it clearly allocates specific amounts to non-taxable categories like "physical injuries" and "pain and suffering," which creates a powerful defense if the IRS ever decides to take a closer look.

You don't just need a lawyer who can win; you need one who knows how to protect what you've won. We are committed to safeguarding your settlement so you can focus on healing.

We will walk you through all the complexities of your recovery, making sure you understand your rights and options at every turn. Learning more about what a car accident lawyer does can give you a much clearer picture of the comprehensive support we provide.

You don't have to navigate this challenging time by yourself. If you're recovering from an accident, reach out to us for a free, no-obligation consultation. Let's talk about how we can help protect your settlement.

Common Questions About Lawsuit Settlement Taxes

We get it—navigating the aftermath of a car accident is confusing enough without worrying about the IRS. Here are some clear, straightforward answers to the questions we hear most often from our clients.

Is My Emotional Distress Taxable if It Was Caused by My Injuries?

This is a critical distinction, and it's one the IRS pays close attention to. If your emotional distress—like anxiety, depression, or PTSD—is a direct result of the physical injuries you suffered in the accident, the compensation for that distress is generally not taxable.

Think of it this way: if you now live with chronic anxiety because of the trauma from the crash and your physical pain, that compensation is part of your physical recovery. It’s all tied together, so it stays tax-free.

However, if a settlement is only for emotional distress without any underlying physical injury, the IRS views it as taxable income. This is exactly why getting detailed medical records that connect your emotional state to your physical harm is so important—it protects your settlement from taxes.

What Is a Structured Settlement and How Does It Affect My Taxes?

A structured settlement isn't a lump-sum payment. Instead, it’s an arrangement where you receive your money in a series of guaranteed payments over time. For victims of catastrophic injuries who will need lifelong care, this can be an incredible tool for long-term financial security.

The best part? The tax-free status of the money related to your physical injuries still applies. Even better, any interest or growth earned on the funds that fuel those future payments is also typically tax-free. If it makes sense for your financial future, your Houston personal injury lawyer can negotiate a structured settlement as part of your case.

A structured settlement offers stability and peace of mind. It guarantees a steady, tax-free income stream to cover your future needs, all while preserving the tax-free nature of your physical injury compensation.

Do I Have to Report a Non-Taxable Settlement to the IRS?

This is a big one. Even if your entire settlement is for non-taxable physical injuries, you will likely still get a Form 1099 from the defendant's insurance company for the full amount. You should never ignore this form.

When this happens, you’ll need to report the total amount on your tax return and then deduct the non-taxable portion. You’ll also need to explain why it’s excluded under IRS Code Section 104(a)(2). If you don't account for that 1099, you could easily trigger an IRS inquiry or even an audit. It’s absolutely essential to talk to a qualified tax professional who can show you how to report everything correctly and avoid any headaches down the road.

At The Law Office of Bryan Fagan, PLLC, we believe you shouldn't have to become a tax expert while you're trying to heal. If a Texas car accident has turned your life upside down, let our experienced team fight to protect not only your rights but your financial future as well.

Contact us today for a free, no-obligation consultation to see how we can help. Visit us at https://houstonaccidentlawyers.net to get started.