A car crash can change your life in seconds—but you don’t have to face recovery alone. The moments after a collision are confusing and overwhelming, but the steps you take are critical for protecting your health and your legal rights. Knowing how to report an accident to insurance is the first step toward getting the support you need to rebuild.

Your First Steps After a Texas Car Accident

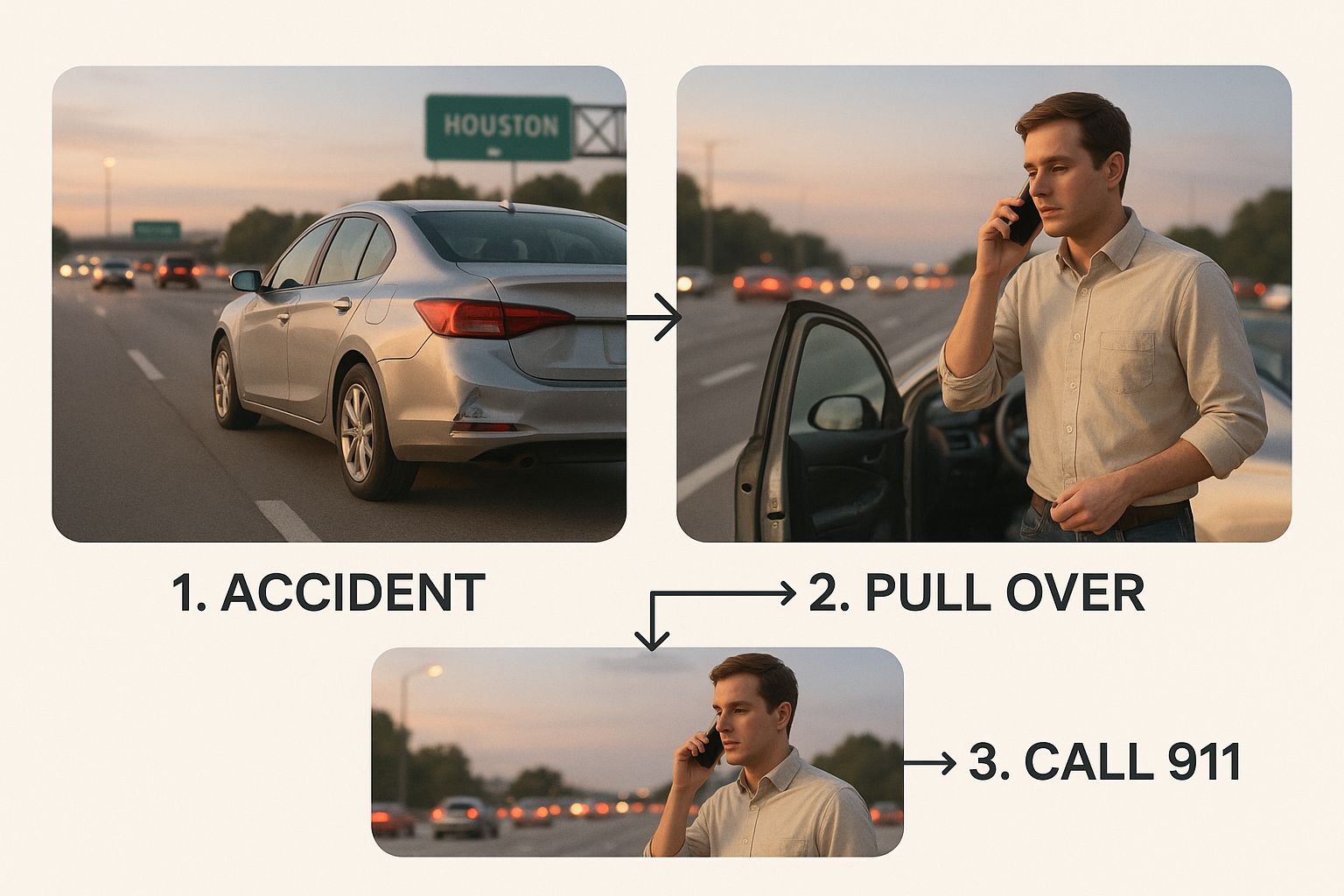

In the confusion and adrenaline rush following a crash, your first thought must be safety. If you’ve been in a wreck on a chaotic road like Houston's I-45, the very first thing you need to do is assess the situation for injuries.

If it's possible and safe, move your vehicle to the shoulder or another nearby spot out of traffic to prevent a secondary collision. Once you're out of immediate harm's way, call 911. You should do this right away, even if the crash seems minor.

Reporting the accident to the police is a non-negotiable step in Texas. A formal police report creates an official, unbiased record of what happened—something that is priceless when it's time to report the accident to insurance. Without it, the other driver might change their story later, making your claim a much harder fight to prove liability—a legal term for who is at fault.

While waiting for help to arrive, you'll need to interact with the other driver. Be calm and stick to the facts. Exchange names, contact information, and insurance policy numbers, but do not discuss who was at fault. Simple, reflexive phrases like "I'm so sorry" can be twisted by insurance adjusters and used as an admission of guilt.

The infographic below outlines the essential on-scene actions that protect both your physical safety and your legal rights.

As you can see, securing the scene and calling for emergency help are the top priorities before you even think about collecting evidence. These first moves form the bedrock of a successful claim.

On-Scene Accident Checklist for Your Insurance Claim

To help you remember what to do in such a stressful moment, we've put together a quick checklist. Think of this as your practical, step-by-step advice for the critical actions to take right after a car accident in Texas.

| Action | Why It's Critical for Your Claim |

|---|---|

| Check for Injuries & Call 911 | Creates an official record (police report) and ensures everyone receives necessary medical attention. A medical report is key evidence. |

| Move to Safety (If Possible) | Prevents further accidents and injuries, which could complicate your claim and liability. |

| Exchange Information | You'll need the other driver's name, contact info, driver's license number, license plate, and insurance policy details to file your claim. |

| Document the Scene | Take photos of vehicle damage, road conditions, traffic signs, and any visible injuries. This is your firsthand evidence. |

| Get Witness Contact Info | Independent witness testimony can be incredibly powerful in supporting your version of events if the other driver disputes fault. |

| Do NOT Admit Fault | Avoid apologies or any statements that could be interpreted as accepting blame. Let the evidence and investigators determine fault. |

Following these steps methodically brings a sense of order to a chaotic situation and sets you on the right path toward recovery.

For a more detailed breakdown of what to do, you can learn more about the crucial steps to take after a car accident in our comprehensive guide.

Gathering Evidence to Support Your Auto Insurance Claim

Once you know everyone is safe and medical help is on the way, your next move is critical: documentation. The evidence you gather in those first few minutes after a wreck builds the entire foundation of your auto insurance claim. This is what you'll need to prove liability—the legal term for who is at fault for the accident.

Think of yourself as an investigator. Your smartphone is the best tool you have. Start taking pictures—many more than you think you need. Get photos of the damage to every vehicle from all angles, both up close and from a distance to show how they came to rest. Don't forget to capture skid marks, traffic signs, weather conditions, and any visible injuries.

Key Information to Collect at the Scene

Photos are just the start. You also need to gather specific details from the other driver and anyone who saw what happened. This information is what your insurance company and your Houston car accident lawyer will use to piece the story together.

Make sure you get:

- Driver Information: The other driver's full name, address, phone number, and driver's license number.

- Insurance Details: Their insurance company and the policy number.

- Vehicle Information: The make, model, color, and license plate of their car.

- Witness Contacts: Names and phone numbers of anyone who saw the crash. An unbiased account from a bystander can be incredibly powerful.

This careful documentation helps establish who was at fault and prevents the other driver from changing their story later. You can learn more about how to avoid common mistakes that could ruin your injury claim in our detailed guide.

In Texas, establishing liability is based on the concept of negligence. The evidence you gather helps demonstrate that the other driver failed to act with reasonable care, causing the accident and your injuries. This is the foundation of Texas personal injury law.

The importance of this step cannot be overstated. Between 2014 and 2023, insured losses from major events worldwide hit a staggering USD 944 billion, which shows just how vital insurance is for financial recovery. The evidence you collect is your key to making sure your claim is handled efficiently, so you can get the compensation you need without fighting unnecessary battles.

Making the First Call to Your Insurance Company

Once you’ve gathered your evidence at the scene, the next move is to notify your own insurance company. Most policies have a clause requiring you to report any crash promptly, so you really should aim to make this call within 24 hours.

This first conversation is more important than you might think. It sets the tone for your entire claim process.

Keep in mind who you're talking to. The adjuster on the other end of the line works for the insurance company, and their primary job is to protect the company's bottom line. What you say—and just as critically, what you don’t say—can make or break your claim. Be polite and cooperative, but be smart about it.

What to Say When You Report the Accident

When you pick up the phone, your only goal is to give a simple, factual notification that an accident happened. That’s it. Stick to the undisputed facts and resist any urge to editorialize, guess, or offer your opinion on how it all went down.

Before you dial, have this info handy:

- Your insurance policy number.

- The date, time, and exact location of the crash.

- Names and contact details for the other drivers.

- The police report number, if one was generated.

A good way to start is by simply saying, "I need to report an accident." Then, calmly provide the basic information. If they ask how you're feeling, the safest and most honest response is often, "I'm planning to get a medical evaluation." This is true, and it prevents you from accidentally minimizing injuries that might not be obvious yet.

Crucial Tip: Never, ever admit fault or even apologize. A simple "I'm so sorry" can be twisted into an admission of guilt. Let the police report and the evidence determine who is liable.

What Not to Say to the Adjuster

Insurance adjusters are trained professionals. They know how to ask leading questions designed to get you to say something that could weaken your claim. Don't fall for it.

Never guess about things like the other car's speed or what you think caused the crash. If you don't know for sure, just say so.

Most importantly, never agree to give a recorded statement until you've spoken with a Houston car accident lawyer. You are not legally required to provide one right away, and it's a tool they can easily use against you later. Your initial report is all they need from you at this stage.

Navigating Talks with the Other Driver's Insurer

It won’t be long after the crash before your phone rings. On the other end will be a friendly-sounding adjuster from the other driver's insurance company.

Don't let the polite tone fool you. Their job isn’t to help you—it's to protect their company’s profits by paying you as little as they possibly can. They are trained professionals, and every question they ask is designed to find a reason to devalue your claim or, even better, shift the blame for the accident onto you.

Understanding How Texas's "Comparative Fault" Rule Works Against You

One of the most common tactics adjusters use is built around Texas's comparative fault rule. This law, found in the Texas Civil Practice & Remedies Code, Chapter 33, states that your final compensation can be reduced by your percentage of fault for the crash.

For example, if you are found to be 20% at fault for an accident, any compensation you receive will be reduced by 20%. Even worse, if you're found to be 51% or more at fault, you get nothing. Zero.

This is why adjusters ask such specific, leading questions. They're fishing for you to admit you were even slightly distracted, a little unsure about a traffic light, or that you braked hard. For example, imagine a Houston driver rear-ended on I-45. The adjuster might ask, "Did you have to brake suddenly?" An innocent "yes" can be twisted to argue that you contributed to the collision, even when the other driver was clearly following too closely.

Key Takeaway: You are under no legal obligation to give a recorded statement to the other driver's insurance company. It’s a tool they use to lock you into a story and poke holes in it later. Politely declining until you've spoken with a lawyer is almost always your best move.

Resisting the Pressure of a Quick Settlement

Another trap to watch out for is the quick, lowball settlement offer. The adjuster might call you just days after the accident, offering a check for a few thousand dollars to "help with your immediate expenses." When you're stressed and bills are coming in, it can be incredibly tempting.

Accepting that offer is almost always a huge mistake.

Once you take their check, you sign away your right to seek any more money for that accident—forever. Many serious injuries, like whiplash or internal damage, don't fully reveal themselves for days or even weeks. If you settle early, you'll be stuck paying for any future medical treatments out of your own pocket.

The global accident insurance market, valued at a staggering USD 90.01 billion in 2025, thrives on closing claims quickly and cheaply before the true costs are known. Discover more insights about these global insurance trends and you'll see how these strategies fit into a much larger financial picture.

Before you say a word to an adjuster or even think about accepting an offer, you need to protect yourself. A skilled Texas injury attorney can take over these conversations for you, making sure your words aren't twisted and you don't get pressured into a settlement that's a fraction of what you truly deserve.

Who Is Liable in a Texas Car Accident?

After a car wreck, knowing what you're entitled to is the first step toward getting a fair outcome. This is where we talk about damages—the legal term for the financial compensation you can recover for all your losses. In Texas, the person or party who is legally responsible, or liable, for the crash is responsible for paying these damages.

A thoroughly documented claim is your most powerful tool for recovering everything you deserve. It’s not just about telling the insurance company what happened; it's about proving the full financial and personal toll the accident took on your life.

The Two Types of Damages in Texas

The compensation you can pursue is split into two main categories: tangible, easy-to-calculate costs and the more personal, intangible losses. Understanding both is essential for building a strong claim.

- Economic Damages: These are the black-and-white numbers—the straightforward, provable expenses. This includes all your medical bills (from the ER visit to ongoing physical therapy), lost wages from being unable to work, and the cost to repair or replace your vehicle.

- Non-Economic Damages: These losses are just as real, but they don't come with a neat price tag. This category covers your physical pain and suffering, emotional distress, mental anguish, and the loss of enjoyment of life. Texas law (specifically Chapter 41 of the Texas Civil Practice & Remedies Code) acknowledges that what you have endured has value and deserves compensation.

The accident insurance market is huge and getting bigger, projected to hit USD 159.60 billion by 2034. That’s a massive jump from USD 85.40 billion in 2024. This trend underscores just how critical it is for the system to handle claims efficiently so victims aren't left waiting. You can read the full research about the accident insurance market to see how these industry shifts play out.

A critical deadline to remember: In Texas, the statute of limitations for personal injury claims is generally two years from the date of the accident. This is your legal deadline to file a lawsuit. If you miss that window, you lose your right to seek compensation forever. Time is not on your side.

It's also crucial to know what you're up against with the other driver's insurance. We've put together a detailed guide on understanding insurance policy limits after a car accident in Texas that can help set realistic expectations from the start.

When Should I Call a Houston Car Accident Lawyer?

A minor fender-bender with no injuries might be handled between you and the insurance companies. But the moment an accident involves serious injuries, everything changes. Suddenly, you're not just dealing with a dented bumper; you're facing a complicated battle for fair compensation while trying to heal. That's when you need to bring in a professional.

An experienced Texas injury attorney immediately steps in to handle all the stressful back-and-forth with the insurance companies. They take on the mountains of paperwork, make sure every critical deadline is met, and start building a powerful case to get you a settlement that actually covers your losses—medical bills, lost income, and the very real pain and suffering you're going through. This can also include seeking wrongful death compensation if your family has lost a loved one.

Many people hesitate to call a lawyer because they're worried about the cost. That's why we work on a contingency fee basis. It’s simple: you don't pay us a dime upfront. Our fee is just a percentage of the money we win for you. If we don't win your case, you owe us nothing.

This model gets rid of the financial risk and lets you get the strong legal help you need right away. Your only job should be focusing on your recovery. Let us handle the fight for the justice you deserve.

Common Questions After a Texas Car Accident

When you're trying to figure out what to do after a crash, a lot of questions pop up. It's a confusing time, for sure. Here are some of the most common concerns we hear from clients and the straightforward answers you need.

How Long Do I Really Have to Report an Accident to My Insurance Company?

This is a big one. Most Texas insurance policies use vague terms like "promptly" or "within a reasonable time," which isn't very helpful when you're under stress.

While there isn't a hard-and-fast legal deadline written into state law, you absolutely shouldn't wait. Waiting gives the insurance company an easy reason to question or even deny your claim. To protect your rights, we always advise clients to make the report within 24 to 72 hours of the accident. The sooner, the better.

What if it's Just a Minor Fender-Bender? Should I Still Report It?

Yes, without a doubt. It’s tempting to just exchange numbers and move on, especially if you don't see any real damage, but that can come back to haunt you.

Some of the most common car accident injuries, like whiplash or even internal bruising, don't show up right away. What looks like a tiny scratch on a bumper could be hiding serious damage to the frame underneath. Reporting the incident, no matter how small, creates an official record. This protects you if the other driver suddenly claims they were hurt a week later.

Think about it this way: a minor tap in a Houston parking lot seems harmless. But if you don't report it and the other driver later decides their neck hurts, you could be left to handle the claim on your own. A quick call to your insurer is just smart protection.

Is My Insurance Rate Going to Skyrocket if I Report a Crash?

This is probably the number one reason people hesitate to make a call, and it’s a valid concern. The answer really boils down to one thing: who was at fault?

If the other driver was clearly negligent and the evidence backs that up, your rates are unlikely to go up. However, if you are found to be at fault for the accident, you might see an increase when your policy renews. But you have to weigh the risks. The potential cost of a personal lawsuit because you failed to report a claim is infinitely higher than a possible rate hike.

Navigating the aftermath of a car accident is challenging, but you do not have to do it alone. The dedicated team at The Law Office of Bryan Fagan, PLLC is here to protect your rights, deal with the insurance companies for you, and fight for the full compensation your family deserves. We are here to inform, reassure, and empower you every step of the way.

For a free, no-obligation consultation to discuss your case and learn about your legal options, contact our compassionate Houston personal injury attorneys today at https://houstonaccidentlawyers.net. Let us help you move forward.