A car crash can change your life in seconds—but you don’t have to face recovery alone. If you've been injured, you're likely wondering, "How much settlement for a car accident can I actually get?" While every accident is unique, the average settlement for bodily injury claims in Texas is around $22,734. But this number is just a starting point. A settlement can range from a few thousand dollars for a minor collision to well over a million for catastrophic injuries, because the final amount is tied directly to the specific facts of your case.

Understanding Your Texas Car Accident Settlement Value

After a wreck, one of the first questions you probably have is, "How much is my car accident claim actually worth?" It’s a completely fair and urgent question. The answer isn’t a random number; it’s a value built by carefully adding up every single loss you've suffered. In legal terms, these losses are called damages, and they are the building blocks of your settlement.

Think of a settlement as the financial compensation meant to make you whole again. It’s designed to cover more than just the obvious costs, like your ER bills or the repairs for your car. A fair settlement from your auto insurance claim should also account for the less visible impacts, like the paychecks you missed while recovering and the physical pain and emotional trauma you’ve had to endure.

Key Factors That Determine Your Settlement Amount

Several different factors come together to shape the final value of your claim. Both the insurance adjuster and your attorney will analyze these elements to arrive at a settlement figure. Understanding what they are puts you in a much stronger position to advocate for the compensation you rightfully deserve.

For a deeper dive into the nuts and bolts, you can explore our detailed guide on the car accident settlement process.

To give you a clearer picture, we've broken down the main components that drive a settlement's value in the table below.

Key Factors That Determine Your Car Accident Settlement Amount

This table outlines the primary elements that insurance companies and lawyers use to calculate the value of a personal injury claim in Texas.

| Factor | How It Impacts Your Settlement | Real-World Example |

|---|---|---|

| Severity of Injuries | More serious injuries mean more medical treatment, longer recoveries, and greater pain and suffering. All of this significantly drives up the settlement value. | A Houston driver with simple whiplash might settle for a few thousand dollars. But a victim suffering a traumatic brain injury from a crash on I-45 could need lifelong care, justifying a seven-figure settlement. |

| Total Medical Expenses | This is the sum of all your medical costs—past, present, and future. It starts with the ambulance ride and ER visit and includes everything from surgery to ongoing physical therapy. It's the foundation of your economic damages. | Your settlement needs to cover not just the surgery you had last month, but also the projected costs for the physical therapy appointments you'll need for the next two years. |

| Lost Wages & Earning Capacity | If your injuries kept you from working, your settlement must replace that lost income. If you can no longer do your old job, it should also compensate you for your diminished ability to earn money in the future. | An office worker who misses two weeks of work would claim those lost wages. A surgeon who sustains a permanent hand injury might claim millions in lost future income. |

| Texas Fault Laws | Texas operates under a "modified comparative fault" rule. If you are found to be partially to blame for the accident, your settlement gets reduced by your percentage of fault. Crucially, if you are 51% or more at fault, you get nothing. | If you're awarded $100,000 but found to be 20% at fault, your final recovery is cut by 20%, leaving you with $80,000. |

| Insurance Policy Limits | Often, the biggest hurdle is the at-fault driver's insurance policy. No matter how high your damages are, you generally can't recover more than the maximum amount their policy will pay out. | If your total damages are $100,000, but the other driver only carries the Texas minimum of $30,000 in liability coverage, your initial recovery is capped at that amount. |

Understanding these factors is the first step, but applying them to your unique situation is where it gets complicated. This is where having an experienced Houston car accident lawyer on your side can make all the difference.

Calculating the Full Cost of Your Damages

After a car crash, the true cost goes far beyond the initial hospital bill or the estimate from the body shop. To determine what your settlement should be worth, we must account for every single loss—both the obvious and the hidden ones. In Texas, this compensation is called damages, and it’s split into two main categories that together show the full value of your claim.

Think of it like building a house. You need a solid foundation—the tangible, provable costs. But you also need the structure itself—the very real, but less tangible, human cost of the accident. Both are absolutely essential to making you whole again.

Economic Damages: The Foundation of Your Claim

First, we start with economic damages. These are the straightforward, out-of-pocket expenses that have a clear price tag. They represent the direct financial hit you’ve taken because of the accident.

Your economic damages include:

- All Medical Bills: This isn't just the ER visit. It’s everything from the ambulance ride and surgery to prescriptions, hospital stays, and follow-up appointments.

- Future Medical Care: A fair settlement doesn’t just pay for what's already happened. It has to cover the cost of any future treatment you'll need, like physical therapy, rehab, or more surgeries down the road.

- Lost Wages: If your injuries kept you out of work, you deserve to be repaid for every dollar of income you missed during your recovery.

- Loss of Earning Capacity: For serious injuries that permanently affect your ability to do your job or earn what you used to, your settlement needs to cover this long-term financial loss.

- Property Damage: This is the cost to repair or replace your vehicle and any other property damaged in the crash.

Let's say you were rear-ended on I-45 here in Houston and suffered a herniated disc. Your economic damages would be the sum of your spine surgeon’s bills, the projected cost of physical therapy for the next year, and the three months of salary you lost while you couldn't work. These hard numbers form the concrete base of your settlement demand.

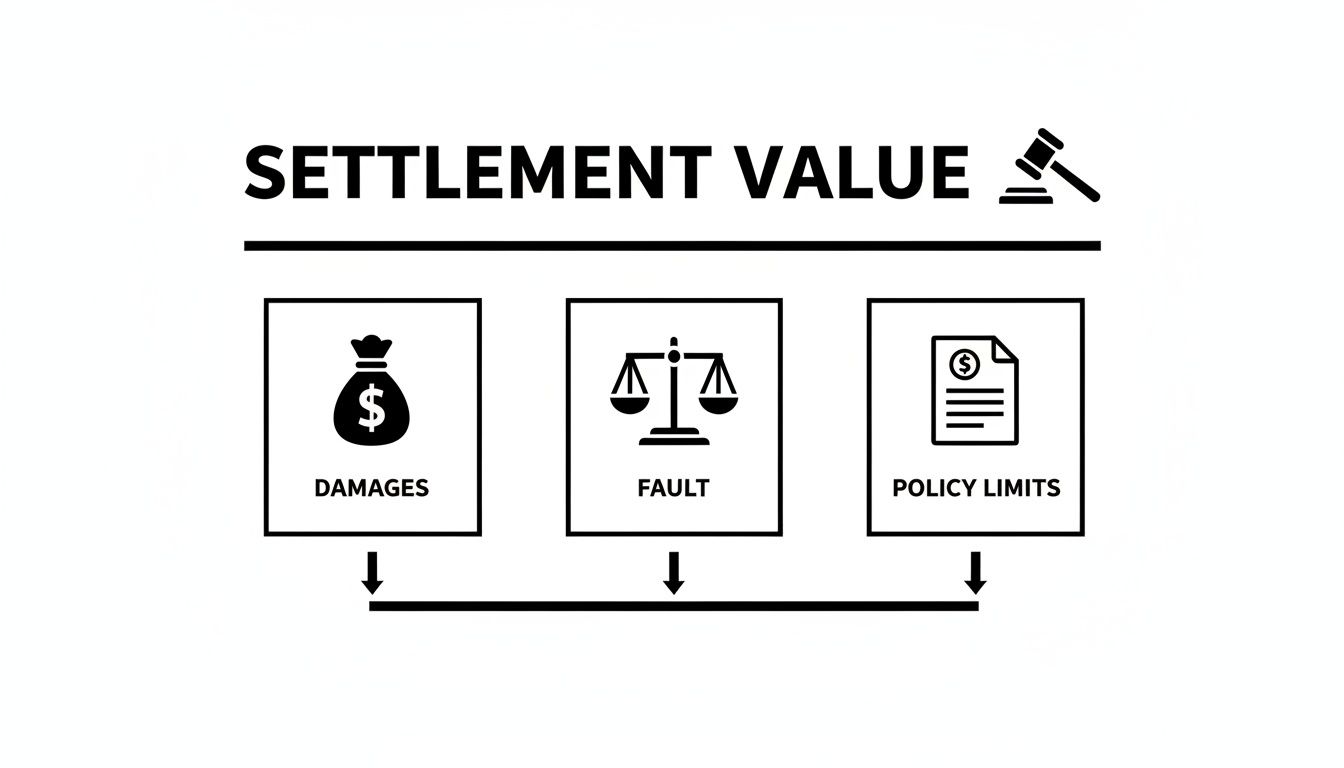

This infographic breaks down how the total damages you've suffered are just one of the core pillars supporting your final settlement value.

As you can see, proving your damages is critical, but it works together with other major factors like who was at fault and the available insurance policy limits to determine the final amount you can recover.

Non-Economic Damages: The Human Cost

Next, we must address non-economic damages. These losses are just as real as a hospital bill, but they don't come with a neat receipt. This is compensation for the human suffering the accident forced upon you and your family.

In Texas, the law recognizes that the impact of a car crash is more than just financial. Your physical pain, emotional trauma, and the disruption to your life have significant value, and you have a right to be compensated for them.

These damages are more personal and subjective, but they are a critical part of any fair settlement. They can include compensation for:

- Pain and Suffering: This covers the physical pain and discomfort you've had to endure because of your injuries.

- Mental Anguish: This addresses the emotional fallout from the crash—anxiety, depression, fear, or even post-traumatic stress disorder (PTSD).

- Physical Impairment: If your injuries left you with a long-term or permanent disability, this compensates you for that loss of physical function.

- Loss of Enjoyment of Life: This is for the loss of your ability to participate in hobbies, activities, or simple daily experiences that you once loved.

Going back to our Houston I-45 crash example, the non-economic damages would be for the constant back pain that keeps you from playing with your kids, the anxiety that now grips you every time you get behind the wheel, and the frustration of not being able to go for your morning run anymore. For a deeper look at this crucial component, you can learn more about how to calculate pain and suffering damages.

An experienced Houston car accident lawyer knows how to document both types of damages to build a powerful case that shows the insurance company the full, devastating impact the crash has had on your life.

How Injury Severity Shapes Your Settlement Amount

The single biggest factor in any car accident claim is how badly you were hurt. A minor fender-bender might leave you sore for a few days, but a serious crash can completely upend your life with broken bones, spinal damage, or a traumatic brain injury. This is where settlement values can differ dramatically.

Insurance adjusters don't just see an "injury"; they categorize it. They group your case into broad buckets, from soft tissue strains like whiplash to catastrophic injuries that change your life forever. Understanding where your injuries fit helps set realistic expectations for what your claim is worth.

Think about it this way: someone who only needs a bottle of ibuprofen after a low-speed collision is in a completely different situation than a person facing surgery, months of physical therapy, and a permanent disability.

Common Injury Categories and Typical Settlement Ranges

Let's break down what these categories often look like in terms of potential compensation.

-

Soft Tissue Injuries: This includes whiplash, muscle sprains, and deep bruising. While painful, these injuries usually heal over time. These claims often settle in the $10,000–$30,000 range.

-

Moderate Injuries: This category includes injuries like fractures, herniated discs, or conditions requiring minor surgery. These cases can easily climb into the $50,000–$100,000 range to cover hospital stays, physical therapy, and lost wages.

-

Catastrophic Injuries: These are the most severe cases, such as traumatic brain injuries (TBIs), spinal cord damage leading to paralysis, or amputations. Settlements here can and often do exceed $1,000,000 because they must account for a lifetime of medical care, home modifications, and lost future earnings. In some tragic cases, this may involve filing a claim for wrongful death compensation.

Beyond just the medical bills, adjusters often use multipliers for "pain and suffering"—the non-economic side of your ordeal. A common 2x–3x multiplier on your economic losses can add another $20,000 or more, even in less severe cases.

Ever wonder why some car crash victims score millions while others get peanuts? Injury severity rules 2025 settlements, with averages masking huge spreads—$20,000 for nonfatal injuries per Blue Sky Legal, but traumatic brain or spinal cases balloon to seven figures. Soft tissue? $10,000-$30,000 range, per Gain Servicing's 2025 benchmarks, including 2-3x multipliers on economic damages like $10,000 meds + $15,000 lost wages. Fractures or surgery? $50,000-$1M, compensating long-term care and earning loss.

Adjusters are always looking for a reason to pay less. Any gap in your medical treatment or sign of improvement can be used to argue your injuries aren't that severe. That’s why detailed medical records are your most powerful evidence.

Why Detailed Medical Documentation Matters

Every single doctor's visit, lab test, and prescription receipt helps build a stronger case. An emergency room bill proves you were hurt at the scene, but it’s the follow-up MRI results and specialist notes that prove the long-term impact of the injury.

If you have gaps in your treatment, an adjuster will likely argue your injuries must not have been that serious or that you’ve already healed.

This is where keeping a simple recovery journal can be a game-changer. Jot down your daily pain levels, what medications you took, and any activities you couldn't do. It paints a vivid picture of your suffering that numbers on a bill just can't capture.

| Injury Type | Settlement Range | Key Considerations |

|---|---|---|

| Soft Tissue | $10k–$30k | Physical therapy notes, time off work |

| Fractures | $50k–$100k | Surgical reports, rehabilitation logs |

| Catastrophic | $1M+ | Lifelong care plans, expert testimony |

A driver who gets rear-ended on I-45 in Houston might only need a few weeks of chiropractic care and end up with a $15,000 settlement. In contrast, a victim of a catastrophic truck wreck on Highway 290 who suffers a brain injury could justify a seven-figure demand to cover a lifetime of needs.

Working with a Texas Injury Attorney

This is where an experienced Texas injury attorney becomes invaluable. They know how to take complex medical records and translate them into a compelling demand for both your economic and non-economic damages. They are also experts on Texas-specific laws, like the rules on comparative fault and damages found in the Texas Civil Practice & Remedies Code.

Your lawyer’s job is to fight back against the insurance company's lowball offers. They will investigate every detail to ensure you receive the maximum compensation available under the law.

Who is Liable in a Texas Car Accident?

Figuring out who’s at fault after a crash might feel obvious to you. But in Texas law—and to every insurance adjuster—fault isn’t always a simple yes or no. The driver responsible is considered liable for the damages, but in many cases, liability can be shared.

Texas follows a legal doctrine known as modified comparative fault (sometimes called proportionate responsibility or the 51% bar rule), which is outlined in Chapter 33 of the Texas Civil Practice & Remedies Code. In plain English, this means you can still recover financial compensation even if you were partially to blame for the accident—as long as your share of the fault is 50% or less.

However, if you are found to be 51% or more responsible, you are barred from recovering any compensation at all. Insurance companies are very familiar with this rule and will often try to shift a portion of the blame onto you to reduce their payout.

How Comparative Fault Reduces Your Settlement

Think of your settlement as a whole pie. The insurance company will try to cut away a slice that is equal to your percentage of fault. Every percentage point they assign to you comes directly out of your final recovery.

For example, imagine you’re driving in Dallas and another motorist makes an unsafe lane change, sideswiping your car. Your total damages—for medical bills, lost income, and pain and suffering—come to $100,000. However, the insurance company argues that you are 20% at fault because you didn't react quickly enough.

Here’s how the math works:

- Total Damages: $100,000

- Your Percentage of Fault: 20%

- Reduction Amount: $100,000 × 0.20 = $20,000

- Your Final Recovery: $80,000

Even a small percentage of fault can cost you thousands of dollars. And if they successfully argue you’re 51% at fault? Your recovery becomes zero.

Protecting Your Rights Against Unfair Blame

Insurance adjusters are trained negotiators whose job is to minimize your claim. They may ask leading questions or try to get you to give a recorded statement where they can twist your words to suggest you admitted fault. That’s why having an experienced advocate on your side is so important.

An experienced Texas injury attorney understands these tactics. We work to gather strong evidence—like police reports, witness statements, and accident reconstruction analysis—to clearly establish the other driver's liability and defend you against unfair accusations of fault.

Your lawyer’s mission is to build a strong case based on facts to keep your assigned fault as low as possible. Don’t let an insurance company's strategy determine your financial future.

The Role of Insurance Policy Limits on Your Claim

Even if you have a rock-solid case with serious injuries, there's often a frustrating cap on what you can recover: the at-fault driver's insurance policy limit. This is the absolute maximum amount their insurer is legally obligated to pay, no matter how high your medical bills and other damages climb. It's a harsh reality that can feel deeply unfair.

Imagine your total damages from a major pile-up on a Houston freeway are $150,000. If the driver who hit you only carries the bare minimum liability coverage required in Texas—just $30,000 per person for bodily injury—their insurance company won't pay a penny more. You're left with a massive shortfall, highlighting a critical gap in the system.

Texas Minimum Liability Coverage Is Often Not Enough

Texas requires drivers to carry what’s known as 30/60/25 coverage. It might sound technical, but it’s a simple breakdown of the minimum protection available if they cause a crash.

- $30,000 for bodily injury liability per person.

- $60,000 for total bodily injury liability per accident (no matter how many people are hurt).

- $25,000 for property damage liability per accident.

Think about it: a single night in the hospital or a necessary surgery can easily surpass that $30,000 limit. This is especially true in accidents that cause significant or life-altering injuries. Relying only on the other driver’s minimum policy often isn’t enough.

Recent U.S. legal analyses show that the average car accident injury settlement is about $30,416. While minor sprains might settle for $8,200 to $20,000, claims involving broken bones or surgeries quickly jump to the $50,000-$100,000 range, easily surpassing minimum policy limits. You can explore more about these settlement averages and their influencing factors on ConsumerShield.com.

This is exactly why a skilled Texas injury attorney never stops at the at-fault driver's insurance. We immediately start digging for other potential avenues for recovery to bridge that financial gap.

Uncovering Other Sources of Compensation

When your damages are far greater than the other driver’s policy limits, it can feel hopeless. But it’s not. There are often other options available to get you the compensation you need to truly recover. A thorough investigation by a legal professional is key.

An experienced lawyer will explore avenues like:

- Your Own UM/UIM Coverage: Uninsured/Underinsured Motorist (UM/UIM) coverage is a vital part of your own auto insurance. It’s designed to step in and cover your damages when the at-fault driver has no insurance or not enough to cover your bills.

- Personal Injury Protection (PIP): Texas requires insurance companies to offer PIP. This coverage pays for your medical bills and lost wages up to your policy limit, regardless of who was at fault in the crash.

- Third-Party Liability: Was a defective part on the car to blame for the accident? Or was the other driver on the clock for a company like Uber or a delivery service? In these situations, other parties and their commercial insurance policies could also be held liable.

For a more detailed explanation, read our guide on understanding insurance policy limits after a car accident in Texas. Navigating these complex insurance layers is critical to maximizing your recovery. We leave no stone unturned in finding every available source of compensation.

Steps to File an Insurance Claim and Maximize Your Settlement

The chaos and confusion right after a car accident are overwhelming. But the steps you take in those first few hours and days can have a major impact on your ability to get a fair settlement. Taking the right actions from the beginning is about protecting your health, your rights, and the strength of your future claim.

Step 1: Immediately After the Crash

Your first priority is always safety. Before you think about insurance or legal claims, check yourself and your passengers for injuries and call 911 right away.

Even if the accident seems minor, calling the police and seeking medical attention are two of the most important things you can do. A police report creates an official record of what happened, which is crucial for proving liability. Seeing a doctor—even if you feel fine—establishes a medical record that directly links any injuries to the accident. This helps prevent the insurance company from arguing your injuries were caused by something else.

Step 2: Gather and Preserve Evidence

Evidence is the foundation of a strong insurance claim. If you're physically able, start documenting everything at the scene with your phone.

Here’s a quick checklist of what to capture:

- Photos and Videos: Take pictures of both cars from every angle. Get shots of the wider scene, including traffic lights, road conditions, skid marks, and any visible injuries.

- Contact Information: Exchange names, phone numbers, and insurance details with the other driver. If there were witnesses, get their contact information too—their impartial perspective can be invaluable.

- Write It All Down: As soon as you can, write down every detail you remember about the crash. Note the time of day, the weather, and exactly what led to the collision. Memories fade quickly, so do this while it’s fresh.

Knowing what to do in the immediate aftermath is critical. For a more detailed checklist, this guide on What To Do After a Car Accident is a great resource.

Step 3: Be Careful When Dealing with Insurance Companies

It won't be long before you get a call from the other driver's insurance adjuster. It is vital to remember that their job is to pay you as little as possible. They are trained negotiators looking for any reason to deny or reduce the value of your claim.

Never give a recorded statement to the other driver's insurance company without talking to a lawyer first. Adjusters are masters at using your words against you to shift blame or downplay your injuries.

Be extremely cautious of a quick settlement offer. The first offer is almost always a lowball amount, made before you even know the full extent of your injuries or what future medical care you might need. Once you accept an offer, you cannot ask for more money later, even if your condition worsens.

Patience is key. The settlement process can take time for a reason. Research shows that most car accident cases take 12-36 months to resolve. Simple cases might settle in 6-12 months, but crashes with significant injuries often take 12-24 months while both sides negotiate and gather evidence. By taking these steps, you are actively building a powerful case to get the full and fair compensation you are owed.

Common Questions After a Texas Car Wreck

After a car wreck, your head is probably swimming with questions. It's a stressful, confusing time, and getting clear answers is the first step toward regaining control. Here are some of the most common concerns we hear from our clients, answered in plain English.

How Long Do I Have to File a Car Accident Lawsuit in Texas?

In Texas, a deadline known as the statute of limitations starts ticking the moment the crash happens. You generally have two years from that date to file a personal injury lawsuit.

This is a strict deadline. If you miss that two-year window, the courts will almost certainly dismiss your case, and you will lose your right to recover any compensation for your injuries. That's why it's so important to speak with a Texas injury attorney as soon as possible. Building a strong case takes time, and waiting too long can jeopardize your rights.

Will My Car Accident Case Go to Court?

It's highly unlikely. The vast majority of car accident claims—more than 95%—are settled out of court through negotiations between your lawyer and the insurance company. Insurance companies are businesses, and they would rather avoid the time, expense, and uncertainty of a jury trial.

So why file a lawsuit at all? Filing a lawsuit is often a strategic move that signals to the insurance company that you are serious and will not accept a lowball offer. It motivates them to negotiate fairly. A skilled Houston car accident lawyer is an expert negotiator who knows how to use this leverage to secure the settlement you deserve, often without ever needing to step inside a courtroom.

Should I Take the First Offer from the Insurance Company?

No, you should almost never accept the first settlement offer. Think of it as their opening bid in a negotiation—and it’s almost always an intentionally low one. The insurance adjuster’s goal is to save their company money, and they make these quick offers hoping you’ll take the cash before you understand what your claim is truly worth.

Accepting an early offer is a final decision. Once you sign the release, you forfeit your right to seek any more compensation, even if your injuries turn out to be far more serious than you initially realized.

Always talk to an experienced attorney before you sign anything. We can help you determine how much a car accident settlement is truly worth in your unique situation, making sure it covers everything—your current medical bills, future treatment, lost wages, and your pain and suffering.

A car crash can be overwhelming, but you don't have to face the insurance companies alone. At The Law Office of Bryan Fagan, PLLC, our compassionate and experienced team is ready to fight for the full compensation you deserve. We will handle the legal complexities so you can focus on what matters most: your recovery.