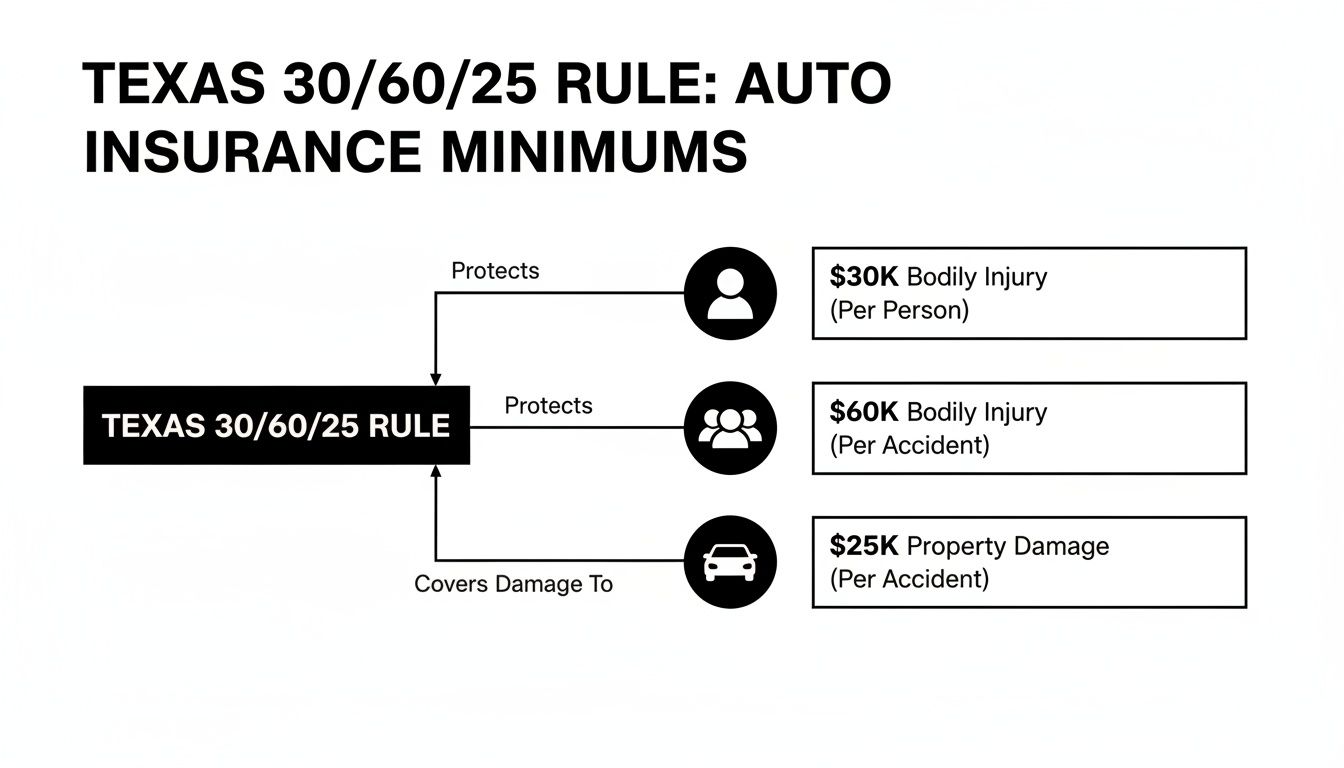

A car crash can change your life in seconds—but you don’t have to face recovery alone. The legal baseline for insurance in Texas is called 30/60/25 liability coverage. This means the at-fault driver’s policy must cover at least $30,000 for one person’s injuries, $60,000 total for all injuries per accident, and $25,000 for property damage.

While that’s the law, it’s often nowhere near enough to cover the true costs of a serious accident. Your rights and your recovery depend on understanding what these numbers mean for you and your family.

Who Is Liable in a Texas Car Accident?

In the moments after a wreck, your world can feel chaotic and overwhelming. You’re dealing with physical pain, emotional shock, and the sudden disruption of your daily life. The last thing you need is the added stress of financial uncertainty, but this is the reality for far too many accident victims in Texas.

Understanding the insurance rules is the first step toward regaining some control. Every driver in Texas is legally required to carry liability insurance. In plain English, liability means legal responsibility. The at-fault driver's liability insurance is their financial responsibility to pay for the harm they caused due to their negligence. Unfortunately, the state-mandated minimums are dangerously low and can leave you with thousands in unpaid bills.

The Harsh Reality of Minimum Coverage

Imagine you're a Houston driver rear-ended on I-45. Your medical bills quickly climb to $50,000, but the driver who hit you only has the bare minimum: $30,000 per person for bodily injury. That 30/60/25 limit means their insurance will only pay up to that $30,000—even if your injuries, like a serious back injury requiring surgery, cost far more.

Suddenly, you’re left with a $20,000 gap, trying to get the rest directly from the driver, which can be an uphill battle if they don't have personal assets to cover it.

This gap between the minimum coverage and the actual cost of an accident is where so many families find themselves in a financial crisis. The insurance company’s first offer is rarely enough to cover your long-term needs, including lost wages and future medical care.

Taking the First Step to Protect Your Rights

After a crash, it's critical to remember that the insurance adjuster's goal is to protect their company's bottom line, not yours. They may sound helpful, but their job is to settle your claim for the lowest amount possible. This is why knowing your rights is so important.

While financial protection is key, all drivers have other legal duties, like passing the annual Texas State Inspection, that contribute to road safety. When someone else’s negligence causes you harm, you deserve a fair recovery. A knowledgeable Houston car accident lawyer can help you navigate the complex auto insurance claim process, calculate the full extent of your damages, and fight for the compensation you need to heal.

Decoding the Texas 30/60/25 Liability Rule

When you hear an insurance adjuster mention "30/60/25," it can sound like some confusing legal code. In reality, it’s a simple formula that lays out the bare-bones minimum liability insurance every Texas driver is required to carry.

Think of it as three separate pots of money the at-fault driver's insurance company must have available to pay for the harm they caused. Let's break down each number so you know exactly what you're dealing with when you file a claim.

The First Number: $30,000 for Bodily Injury Liability Per Person

The "30" in 30/60/25 stands for $30,000. This is the absolute maximum amount the at-fault driver's insurance will pay for the injuries of a single person hurt in the crash.

This money is meant to cover your medical bills, lost wages from being unable to work, and other injury-related costs. The problem is, this amount is often exhausted frighteningly fast after a serious collision. One trip to the emergency room, an MRI, and a few follow-up appointments can easily blow past this limit, leaving you on the hook for the rest.

The Second Number: $60,000 for Bodily Injury Liability Per Accident

The "60" represents $60,000. This is the total pot of money the insurance company will pay for all injuries to all people in a single wreck, no matter how many victims there are.

Imagine a multi-car pile-up on I-45 where the at-fault driver injures three other people. Even if each person has $30,000 in medical bills, the insurance company is only on the hook for a total of $60,000 to be split among them.

Real-World Example: If three victims have a combined $90,000 in medical costs, the at-fault driver’s policy only provides $60,000. That leaves a $30,000 gap that the injured people now have to figure out how to cover—often from their own pockets or by filing a lawsuit against the driver directly.

This is a critical limitation that can leave multiple families facing financial hardship after just one crash. The fund is depleted quickly, often pitting victims against each other for a limited pool of money.

The Third Number: $25,000 for Property Damage Liability

Finally, the "25" stands for $25,000. This is the maximum the at-fault driver's policy will pay to repair or replace all property damaged in the accident.

This includes things like:

- Repair costs for your vehicle

- The value of your car if it's declared a total loss

- Damage to other property, like a fence, mailbox, or personal items inside your car (think laptops or phones)

With the skyrocketing cost of cars and repairs, even this amount can fall short, especially if a newer car is totaled or multiple vehicles are damaged.

To help you visualize how this works, here’s a simple breakdown of what these minimum limits mean for you as an accident victim.

Texas Minimum Liability Insurance (30/60/25) Explained

| Coverage Type | Minimum Amount | What It Covers For You (The Victim) |

|---|---|---|

| Bodily Injury Per Person | $30,000 | Pays for your individual medical bills, lost wages, and pain and suffering, up to this limit. |

| Bodily Injury Per Accident | $60,000 | The total available for all injured people combined. If you and your passengers are hurt, you share this pot. |

| Property Damage Per Accident | $25,000 | Pays to repair or replace your vehicle and any other property that was damaged in the crash. |

Understanding these numbers is the first step in protecting your rights. Each part of the 30/60/25 rule has firm limits that insurance companies will not exceed. For a deeper look into how these policies work, you can learn more about liability insurance in Texas in our detailed guide.

When your costs go far beyond these state minimums, you need an experienced advocate to explore every other possible option for your recovery.

When Minimum Coverage Fails to Cover Your True Costs

Those state-mandated minimums give drivers a false sense of security. The hard truth is that the 30/60/25 limits are dangerously low for covering the real-world costs of a serious car wreck. A single severe injury can easily generate expenses that blow past these caps, leaving victims in a devastating financial hole.

When a Texas injury attorney talks about your losses after a crash, we use the term damages. It’s simply the legal term for all the harm you've suffered—physical, emotional, and financial. Grasping what counts as "damages" is the first step to understanding why minimum coverage is almost never enough.

What Are Damages in a Car Accident Claim?

In a Texas personal injury claim, your damages are split into two main categories. Each one represents a different kind of loss you've experienced because someone else was negligent.

- Economic Damages: These are the tangible, out-of-pocket costs that come with a clear price tag. Think of them as the bills and financial losses you can add up on a calculator. This includes medical bills (ER visits, surgeries, physical therapy), lost income from being unable to work, and the cost of any future medical care you'll need.

- Non-Economic Damages: These are the intangible losses that don’t come with a receipt but are just as real and debilitating. This category covers your physical pain, emotional suffering, mental anguish, and the loss of your ability to enjoy life. While harder to put a number on, they are a critical part of your recovery.

The infographic below breaks down how the Texas 30/60/25 rule is structured.

As you can see, those policy limits are hard ceilings on what the at-fault driver's insurance will pay, no matter how high your actual costs climb.

A Realistic Scenario of Minimum Coverage Failing

Let’s walk through a real-world example to see just how quickly these minimums evaporate. Imagine you're rear-ended on US-290 in Houston and suffer a traumatic brain injury (TBI).

The immediate aftermath involves an ambulance ride, an emergency room visit, CT scans and MRIs, and a hospital stay for observation. The bills for this initial care alone can easily fly past $30,000 within just a few days.

And that doesn't even touch the long-term consequences. A TBI victim often needs:

- Months or years of neurological rehab

- Ongoing physical, occupational, and speech therapy

- Potential home modifications to accommodate new disabilities

- Lost earning capacity if they can no longer do their old job

The total economic damages could quickly rocket into the hundreds of thousands of dollars. On top of that, the victim endures immense pain and suffering. But the at-fault driver's minimum liability policy? It will only pay out the first $30,000.

This is the devastating gap where victims are left vulnerable. When the at-fault driver’s insurance is not enough to cover your damages, they are considered an underinsured motorist. You are now facing a mountain of debt for an accident that wasn't your fault.

This situation is frighteningly common across Texas. It shines a harsh light on the critical flaw of relying on state minimums for protection. When you’re up against an underinsured driver, you have to find other sources of compensation. This is where your own insurance policy and the guidance of an experienced Texas injury attorney become absolutely essential to protecting your financial future and ensuring you get the care you need.

Steps to File an Insurance Claim and Protect Your Rights

Knowing that the Texas minimum insurance requirements often leave a massive financial gap after a serious crash is scary. The good news? You don't have to leave your family's financial security in the hands of the other driver. You have the power to build your own safety net by adding a few key coverages to your own policy.

Think of it like this: the at-fault driver's liability insurance is their plan to pay for the mess they made. But what happens when their plan isn't good enough? That's where your own policy needs a backup plan. The two most critical types of "backup" coverage in Texas are Uninsured/Underinsured Motorist (UM/UIM) coverage and Personal Injury Protection (PIP).

Uninsured/Underinsured Motorist (UM/UIM) Coverage

Uninsured/Underinsured Motorist (UM/UIM) coverage is your personal financial shield against irresponsible drivers. And in a state like Texas, with one of the highest rates of uninsured drivers in the country, this isn't a luxury—it's a necessity.

It’s actually two types of protection rolled into one:

- Uninsured Motorist (UM) Coverage: This helps you if you’re hit by a driver with no liability insurance at all. It also applies in most hit-and-run situations where the other driver is never found.

- Underinsured Motorist (UIM) Coverage: This is the big one. It kicks in when the at-fault driver does have insurance, but their policy limits are too low to cover all your damages.

Let’s go back to that Houston driver facing $50,000 in medical bills after being hit by someone with a bare-bones $30,000 policy. If that victim had their own $100,000 UIM policy, their insurance would step in to cover the remaining $20,000 in medical bills. It could also cover other damages like lost wages or pain and suffering, right up to their policy limit. To see a full breakdown, check out our underinsured motorist coverage in Texas in our guide.

Personal Injury Protection (PIP) Coverage

Personal Injury Protection (PIP) is another non-negotiable layer of protection. Unlike almost every other type of insurance, PIP is "no-fault." That means it pays out for your medical bills and a portion of your lost wages right away, no matter who caused the crash.

PIP is designed to get cash in your hands fast while you’re waiting for the at-fault driver’s insurance to get its act together. This can be a total lifeline, helping you pay the mortgage and cover co-pays without draining your savings.

In Texas, insurers are required by law to offer you at least $2,500 in PIP coverage. You have to sign a form to reject it in writing. We tell every client not only to accept PIP but to buy higher limits if they can afford it—like $5,000 or even $10,000. The slight increase in your premium is nothing compared to the peace of mind it buys you.

Review Your Policy and Take Action

Once you’re in a wreck, it's too late to add coverage. The time to protect yourself is now, before you ever need it. Find your insurance policy’s declaration page or call your agent and ask two simple questions:

- Do I have UM/UIM coverage, and what are the limits?

- Do I have PIP coverage, and what is my limit?

If your limits are low—or worse, you waived this coverage—we urge you to fix it today. By investing in solid UM/UIM and PIP policies, you’re taking a powerful, proactive step to protect your family’s future from the financial disaster an underinsured driver can cause.

How a Car Accident Lawyer Maximizes Your Claim

When you’re facing a mountain of medical bills and an uncooperative insurance adjuster, it feels like the odds are stacked against you. This is exactly where a skilled Houston car accident lawyer can level the playing field.

Our role goes far beyond filing paperwork. We become your dedicated advocates, fighting to ensure you get the full and fair compensation you need to rebuild your life. Remember, insurance companies are businesses, and their main goal is to protect profits by minimizing payouts. An experienced attorney knows their tactics inside and out and has the resources to counter them.

Launching an Independent Investigation

The insurance company's investigation isn’t designed to help you; it’s designed to find ways to reduce or deny your claim. That’s why we conduct our own thorough, independent investigation focused on one thing: proving the other driver’s liability.

Liability is just a legal term for responsibility. To win your claim, we have to show the other driver was negligent and that their negligence directly caused your injuries.

Our investigation often includes:

- Securing critical evidence from the scene, like police reports, photos, and traffic camera footage.

- Interviewing eyewitnesses to get unbiased accounts of what really happened.

- Hiring accident reconstruction experts to scientifically prove how the crash occurred, which can be absolutely vital in complex cases like a multi-car pileup on I-45.

Calculating the True Value of Your Damages

One of the biggest mistakes you can make is accepting an early settlement offer from the insurance company. That initial offer almost never accounts for the full scope of your damages—the total physical, emotional, and financial harm you've suffered.

We meticulously calculate the complete value of your claim, digging into costs the adjuster might conveniently overlook:

- Future Medical Expenses: This includes potential surgeries, ongoing physical therapy, medication, and any long-term care you might need down the road.

- Lost Earning Capacity: If your injuries keep you from returning to your old job or working at all, we calculate the lifetime impact on your income.

- Non-Economic Damages: We fight hard for compensation covering your pain, suffering, and the diminished quality of life that numbers can't easily capture.

Protecting You from Unfair Blame

Insurance adjusters love to shift blame onto the victim to reduce their payout. This tactic is rooted in a Texas law known as comparative fault.

Under the Texas Civil Practice & Remedies Code, Chapter 33, if you are found to be more than 50% responsible for the accident, you are barred from recovering any compensation at all. If you are found partially at fault (but 50% or less), your compensation is reduced by your percentage of fault. This is why it's called "comparative fault"—your recovery is compared to your level of responsibility.

For example, if you are awarded $100,000 but found 10% at fault, you would only receive $90,000. An attorney’s job is to use the evidence from our investigation to fight back against these baseless accusations and protect your right to a full recovery. Understanding the details can be tricky, but you can learn more about what a car accident lawyer does in our comprehensive guide.

You Don’t Pay Unless We Win

We know the last thing you need after a crash is another bill. That’s why our firm works on a contingency-fee basis.

This means you pay absolutely no upfront costs or attorney’s fees. We only get paid if we successfully recover compensation for you. This model removes the financial barrier to getting expert legal help, allowing you to focus completely on your physical and emotional recovery while we handle the legal fight.

Common Questions After a Texas Car Accident

When you’re trying to recover from a serious crash, your mind is probably racing. The aftermath is a confusing mess of pain, paperwork, and uncertainty, and trying to get straight answers from insurance companies can feel like navigating a maze in the dark.

We hear the same questions from accident victims every day. Below, we’ve put together clear, straightforward answers to help you feel more in control and understand the path forward.

What if the At-Fault Driver Has No Insurance at All?

This is a frighteningly common scenario on Texas roads, and it’s the exact reason why carrying your own Uninsured Motorist (UM) coverage is so critical. If an uninsured driver hits you—or if you're the victim of a hit-and-run—your UM policy is your best line of defense.

Here’s how it works: you file a claim with your own insurance company. Your insurer then steps into the shoes of the at-fault driver's insurance (the one that doesn't exist) and covers your damages. This includes medical bills, lost wages, and pain and suffering, all the way up to your policy limits.

Without UM coverage, your options get much harder. You can sue the uninsured driver personally, but the reality is that most people driving without insurance don't have the assets to pay a court judgment. A skilled Texas injury attorney can investigate every possible avenue for recovery to make sure you aren't left holding the bill for someone else's mistake.

How Long Do I Have to File a Car Accident Lawsuit in Texas?

Texas law sets a strict deadline for filing a personal injury lawsuit, known as the statute of limitations. For nearly all car accident claims, you have just two years from the date of the crash to file your case in court.

If you miss that two-year window, the court will almost certainly throw your case out, and you will permanently lose your right to seek compensation, such as wrongful death compensation for a lost loved one. Two years might sound like a long time, but building a strong legal case is a detailed process. Evidence disappears, witness memories fade, and medical treatments need to be fully documented.

The statute of limitations is a hard deadline. Waiting too long puts your entire ability to hold the negligent driver accountable at risk.

The best way to protect your rights is to contact a Houston car accident lawyer as soon as you can after a crash.

Will My Rates Go Up if I Use My Own UM/UIM Coverage?

This is a huge worry for a lot of drivers, but you can relax. Texas law explicitly prohibits insurance companies from raising your premiums for filing a UM/UIM or PIP claim when you were not at fault for the accident.

You pay for these coverages for this exact reason—to protect you when someone else causes you harm. Using the benefits you’ve paid for is your legal right, and you can't be punished for it. If an insurer tries to jack up your rates or denies a valid claim anyway, they may be acting in "bad faith." An experienced attorney can fight back against these illegal insurance tactics.

Should I Accept a Quick Settlement Offer from the Insurance Company?

Be extremely wary of any fast settlement offer. Insurance adjusters are trained professionals whose entire job is to protect their company’s bottom line by closing your claim for as little money as possible. That first offer is almost never what your case is truly worth.

These lowball offers rarely, if ever, account for the full picture. They conveniently ignore critical factors like:

- Future medical care, such as surgeries, physical therapy, or long-term pain management.

- Lost earning capacity if your injuries impact your ability to work down the road.

- Non-economic damages, which includes your physical pain, emotional trauma, and the loss of quality of life.

Once you accept a settlement and sign that release form, it's over. You give up all rights to seek any more money for your injuries, even if they turn out to be far worse than you first realized. Before you sign anything or agree to a recorded statement, you need to speak with a personal injury attorney. We can calculate the true, long-term value of your claim and fight for the fair compensation you need to actually recover.

The moments after a car accident are overwhelming, but you don’t have to face the complex insurance and legal systems by yourself. At The Law Office of Bryan Fagan, PLLC, our compassionate Houston car accident lawyers are here to answer your questions, protect your rights, and fight for the justice you deserve. We handle the legal battle so you can focus on healing.

Contact us today for a free, no-obligation consultation to discuss your case and learn how we can help you and your family.