A car crash can change your life in seconds — but you don’t have to face recovery alone. One moment, you're driving. The next, you're dealing with the jarring crunch of metal, shattered glass, and the overwhelming fear of what comes next. The pain and confusion are immense, and a mountain of unexpected bills starts to pile up.

Then comes the gut punch: the driver who hit you doesn't have insurance. Suddenly, the stress multiplies, and it feels like you've been left to clean up someone else's mess all by yourself.

If this sounds familiar, we want you to know that help is available. This guide is for every Texan who has been blindsided by an uninsured or underinsured driver, whether on the busy streets of Houston or the highways connecting Dallas, Austin, and San Antonio. We are here to help you understand your rights and find a path forward.

Your Shield Against Irresponsible Drivers

We're here to walk you through Uninsured/Underinsured Motorist (UM/UIM) coverage—a critical part of your own insurance policy designed for this very scenario. Think of it as your financial shield when the person at fault simply can't pay for the damage they’ve caused you and your family.

Unfortunately, this is a scenario that plays out far too often in our state. Texas has one of the highest rates of uninsured drivers in the nation. Some estimates suggest that nearly 1 in 7 drivers on our roads are breaking the law by driving without insurance.

That means your chances of being hit by someone who can't cover your losses are alarmingly high. For example, a Houston driver rear-ended on I-45 could be facing tens of thousands of dollars in medical bills, lost wages, and car repairs, with no way to get compensation from the at-fault driver. This is exactly where your own policy is supposed to step in and fill that gap.

We understand what you're going through. Our goal is to explain your rights with compassion and clarity, helping you find the path to getting your life back on track.

Understanding what your policy covers—and what your rights are—is the first step toward recovery. You have been through enough; you shouldn’t have to fight an insurance company by yourself, especially when you've been hit by an uninsured motorist. Knowing the right steps to take is crucial for protecting your financial future.

Filing a UM claim involves specific procedures and deadlines that are tough to manage while you’re trying to heal. Our goal is to give you clear, practical advice. From proving the other driver was at fault to properly documenting your damages, we'll explain how to build a strong claim and fight for the fair compensation you deserve.

What Is Uninsured Motorist Coverage in Texas?

Let's break down Uninsured/Underinsured Motorist (UM/UIM) coverage in plain English. It’s not a complicated legal product—it’s a safety net you buy for yourself and your family. Think of it as a promise that you will be protected when the unexpected happens on the road.

When a driver who causes an accident has no insurance—or not nearly enough—your UM/UIM coverage steps up. It’s designed to pay for your medical bills, lost wages, and even vehicle repairs, filling the financial gap left by someone else’s irresponsibility. It ensures your path to recovery isn’t blocked by their negligence.

Two Layers of Protection

In Texas, your Uninsured Motorist coverage is really two policies rolled into one. Each part serves a critical function after a crash.

- Uninsured Motorist (UM) Coverage: This is for when the at-fault driver has no liability insurance at all. It’s also your go-to in those incredibly frustrating hit-and-run situations where the other driver vanishes and can't be identified.

- Underinsured Motorist (UIM) Coverage: This applies when the at-fault driver does have insurance, but their policy limits are too low to cover all your damages. For instance, if your medical bills hit $50,000 but the other driver only carries the Texas minimum of $30,000, your UIM coverage can step in to cover the remaining $20,000.

Imagine you get rear-ended on I-45 in Houston by someone with minimum coverage. If your injuries require surgery and months of physical therapy, their small policy will run out almost instantly. This is exactly when your own UIM coverage becomes an absolute financial lifeline.

Why This Coverage Is So Important in Texas

Texas law is clear: every insurance company must offer you UM/UIM coverage whenever you buy or renew your auto policy. While you aren't forced to buy it, you do have to reject it in writing. Skipping it might save a few dollars on your premium, but it leaves you dangerously exposed on Texas roads.

The hard truth is that our roads are filled with risk. Texas has one of the worst uninsured driver rates in the country—some data suggests 1 in 7 drivers are on the road without legal coverage. In metro areas like Houston, that number can creep closer to 1 in 5.

This growing problem of uninsured drivers, made worse by skyrocketing insurance costs, makes UM/UIM coverage not just a smart choice, but an essential protection for your family.

"UM/UIM coverage isn't for the other driver—it's for you. It ensures that your recovery isn't dependent on the financial responsibility of a stranger."

What Does Uninsured Motorist Coverage Pay For?

Many people think UM/UIM just covers car repairs, but it's much broader than that. It’s designed to cover the full range of losses you suffer when an uninsured or underinsured driver hits you.

This includes:

- Medical Expenses: Everything from the ambulance ride and hospital stay to surgery, physical therapy, and any future medical care you might need.

- Lost Wages: The income you lose because you’re unable to work while you heal.

- Pain and Suffering: Compensation for the physical pain and emotional trauma the accident has put you through.

- Property Damage: The cost to get your vehicle repaired or replaced, which comes with a standard $250 deductible.

Without this coverage, you would be stuck paying these costs yourself or hoping your health insurance covers some of them—but it won't touch your lost income or pain and suffering. A skilled Texas injury attorney can help you navigate your policy to make sure you get every dollar you're owed.

Comparing Your Texas Auto Insurance Options

This table breaks down different types of auto insurance to clarify what each covers after you've been in an accident with an uninsured driver in Texas.

| Coverage Type | What It Typically Covers For You | When It Is Most Useful |

|---|---|---|

| Uninsured/Underinsured Motorist (UM/UIM) | Your medical bills, lost wages, pain and suffering, and property damage. | When the at-fault driver has no insurance, not enough insurance, or flees the scene (hit-and-run). |

| Liability Coverage | Nothing. This coverage only pays for damages you cause to others. | It's legally required but offers you zero personal protection if another driver is at fault. |

| Personal Injury Protection (PIP) | Your medical bills and a portion of your lost wages, regardless of who is at fault. | For immediate medical needs after any accident, but limits are often low and it doesn't cover pain/suffering. |

| Medical Payments (MedPay) | Your medical bills only, up to your policy limit, regardless of who is at fault. | For immediate medical bills, but it's less comprehensive than PIP and doesn't cover lost wages. |

| Collision Coverage | Repairs to your vehicle after an accident, regardless of fault. | When your car is damaged in any type of collision, but it won't cover your medical bills or lost income. |

As you can see, UM/UIM is the only coverage specifically designed to protect you from the financial fallout caused by an irresponsible driver. Relying on other coverages leaves major gaps that can put your financial future at risk.

Steps to File Your UM/UIM Insurance Claim

Knowing what to do after a crash is overwhelming. Adrenaline is pumping, you might be hurt, and now you have to deal with insurance companies. But having a clear, step-by-step plan can bring back a sense of control. Here is practical advice for filing an Uninsured/Underinsured Motorist (UM/UIM) claim and protecting your rights.

Your first priority, always, is safety. If you can, move your vehicle out of traffic, check on everyone involved, and call 911 immediately to get police and paramedics on the way. Even if you think you feel fine, see a doctor. Adrenaline can easily mask serious injuries that may appear later.

What to Do at the Scene of the Accident

The information you gather right after the crash can make or break your claim. While you wait for the police, start documenting everything you can.

- Get Driver Information: Exchange names, addresses, phone numbers, and—most importantly—insurance details with the other driver. If they admit they don't have insurance, make a note of it.

- Document Everything: Use your phone to take photos and videos of the accident scene from multiple angles. Get pictures of the damage to both cars, any skid marks on the road, traffic signals, and any visible injuries.

- Speak to Witnesses: If anyone saw the crash, get their names and phone numbers. An independent witness can provide powerful, unbiased testimony down the road.

- Get a Police Report: When officers arrive, give them a clear, factual account of what happened. Do not guess or speculate. Make sure you get the police report number before you leave—this document is a key piece of evidence for proving liability, a legal term for showing the other driver was at fault.

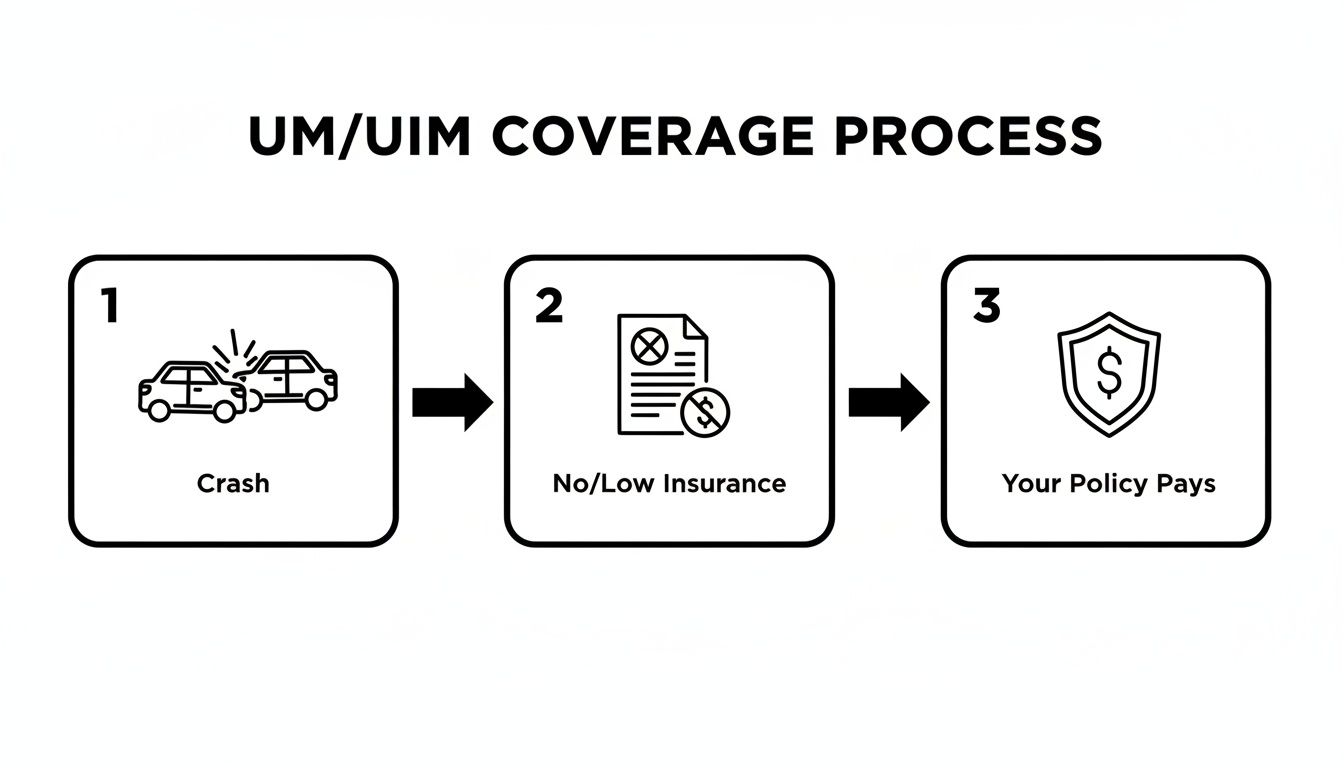

Using your UM/UIM coverage follows a straightforward path when the at-fault driver can't pay for the damage they caused.

As you can see, it’s a simple trigger: a crash happens, the other driver has little or no insurance, and your own UM/UIM policy is supposed to step in and cover your losses.

Notifying Your Insurance Company

Once you are safe and have seen a doctor, it's time to call your own insurance company. You need to let them know you've been in an accident and that you plan to file a claim under your uninsured motorist coverage Texas policy.

This is where things can get tricky. Remember, even though it's your insurance company, their goal is to pay out as little as possible. They will assign an adjuster to investigate your auto insurance claim. You'll need to provide them with the police report, the photos you took, and any other evidence you collected. You can learn more about how underinsured motorist coverage works in Texas in our detailed guide.

Statute of Limitations: This is a legal term for a deadline. Under Texas law, you generally have two years from the date of the accident to either settle your claim or file a lawsuit. If you miss it, you lose your right to seek compensation forever.

Proving Your Damages and Losses

To get a fair settlement, you have to prove every single one of your losses, which lawyers call damages. This isn't just about the immediate bills. It's about documenting all the ways this accident has upended your life.

Your damages can include:

- Medical Records: Every bill from the hospital, doctors, chiropractors, physical therapists, and pharmacies.

- Proof of Lost Income: Pay stubs or a letter from your employer showing the time you were forced to miss from work.

- Repair Estimates: Quotes from body shops for fixing your car or documentation showing it's a total loss.

- Personal Journal: This can be incredibly powerful. Keep a simple log of your daily pain levels, emotional struggles, and all the ways your injuries affect your daily life.

For example, a Houston driver rear-ended on I-45 may have obvious immediate damages like the ambulance ride and car repairs. But the real costs pile up over time—ongoing physical therapy, lost wages from being unable to work, and the significant pain and suffering that follows. All of these are legitimate damages that should be covered by a UM/UIM claim.

Filing this kind of claim involves strict deadlines and requires careful proof. A Houston car accident lawyer can take this burden off your shoulders, managing the entire process so you can focus on what really matters: your recovery.

Why Your Own Insurance Company May Fight Your Claim

You have faithfully paid your insurance premiums for years, trusting that your provider would have your back if the worst happened. So when you file a claim for uninsured motorist coverage Texas, it’s a shock when the company you trusted starts treating you like an opponent.

It’s a frustrating and deeply unfair feeling, but it’s an all-too-common reality. The simple truth is that even your own insurance company is a business first. Its primary goal is to protect its bottom line, which means minimizing every payout—including yours. In their eyes, your claim is a potential loss on their balance sheet.

Common Tactics Insurance Adjusters Use

Insurance adjusters are trained negotiators, and they have a playbook of tactics designed to reduce the value of your claim. Recognizing these moves is the first step toward protecting yourself.

Watch out for these common strategies:

- The Quick, Lowball Offer: Shortly after the crash, an adjuster might call, sounding friendly and concerned. They may offer a fast check to "help you out," hoping you’ll take it before you understand the full extent of your injuries and future medical needs. This offer is almost always a fraction of what your claim is really worth.

- Questioning Your Medical Treatment: They might pick apart your doctor’s recommendations, suggesting your physical therapy is excessive, your treatment is too expensive, or that your injuries aren't even related to the accident. This is a calculated move to reduce what they owe for your medical care.

- Requesting a Recorded Statement: An adjuster will often ask for a recorded statement, framing it as a routine step. Be careful. They are trained to ask tricky, leading questions designed to get you to say something that undermines your claim, like downplaying your pain or accidentally admitting partial fault.

These are deliberate strategies to pay you as little as possible.

Using the Law Against You

One of the most powerful tools in an insurer's arsenal is Texas’s comparative fault rule. Also known as proportionate responsibility, this law (found in Chapter 33 of the Texas Civil Practice & Remedies Code) states that your total compensation can be reduced by your percentage of blame for an accident. If you're found to be 10% at fault, your final settlement gets cut by 10%.

Insurance companies will dig for any reason—no matter how small—to shift blame onto you. They might argue you were speeding, distracted, or made an improper lane change, even if the police report says otherwise. By unfairly pinning even a small amount of fault on you, they can save themselves a significant amount of money.

For instance, an Austin driver T-boned by an underinsured motorist could be left with massive medical bills. The high rate of uninsured drivers—climbing towards 20% in dense urban areas like Houston—makes this a daily reality for many Texans.

When an Insurer Acts in Bad Faith

There’s a clear line between aggressive negotiation and illegal behavior. When an insurance company acts dishonestly or unfairly to avoid paying a legitimate claim, it is known as acting in bad faith.

Examples of insurance bad faith include:

- Unreasonably denying a claim without a valid reason.

- Failing to conduct a proper and timely investigation.

- Misrepresenting the facts of the crash or the terms of your own policy.

- Refusing to make a fair settlement offer when liability is clear.

If your insurer is engaging in these practices, you may have grounds for a separate bad faith lawsuit in addition to your original UM/UIM claim. If you're already struggling with a denial, it's crucial to know what to do when your insurance denies your claim. A dedicated Houston car accident lawyer can hold them accountable and fight for every penny you are owed.

Understanding the Full Value of Your Claim

To get the fair compensation you need after a crash, you first have to understand what you're truly owed. When you file an uninsured motorist coverage Texas claim, you are not just asking for a check to cover the first hospital bill. You are seeking compensation for every single loss the accident caused—both the ones you can see on paper and the ones you feel every day.

These losses are legally known as “damages,” and they represent the total financial, physical, and emotional cost of the accident. Your insurance policy is a contract, and unlocking the true value of your claim often hinges on a deep understanding of its contract interpretation principles. A skilled Texas injury attorney can break down the fine print and explain exactly what you are entitled to.

In Texas, damages are split into two main categories.

Economic Damages: The Tangible Costs

Economic damages are the most straightforward part of your claim because they come with a receipt. These are the direct, out-of-pocket financial losses you’ve suffered because of someone else's negligence. It is absolutely critical to keep detailed records of every expense.

Your economic damages can include:

- Current and Future Medical Bills: This includes the ER visit, ambulance ride, surgery, follow-up appointments, physical therapy, prescription medications, and any long-term care you might need.

- Lost Wages: This is the income you lost because you were physically unable to work while recovering.

- Loss of Earning Capacity: If your injuries permanently impact your ability to do your job or earn the same living you did before, you can claim damages for this future lost income. This can provide crucial compensation for wrongful death cases where a family loses its primary earner.

For example, a construction worker in Dallas is hit by an uninsured driver and can no longer perform physical labor. His claim would include not only his immediate medical bills but also the projected income he will lose over the rest of his career.

Non-Economic Damages: The Human Cost

Non-economic damages are just as real as a stack of medical bills, but they compensate you for the losses that don’t have an obvious price tag. These damages are meant to acknowledge the profound human toll an accident takes on your life and well-being.

They provide compensation for things like:

- Pain and Suffering: This accounts for the physical pain, chronic discomfort, and emotional distress you've endured.

- Mental Anguish: This covers the psychological impact—anxiety, depression, insomnia, fear of driving, or even PTSD.

- Physical Impairment or Disfigurement: This compensates you for permanent limitations on your physical abilities or for scarring and other visible injuries that change your life.

When calculating these damages, an insurance adjuster or a jury will look at the severity and permanence of your injuries. This is where keeping a personal journal detailing your daily struggles can become powerful evidence.

Under Texas law, the goal of compensation is to make you "whole" again. While no amount of money can erase your pain, it can provide the financial stability you need to move forward.

Finally, in rare cases involving extreme recklessness—like a crash caused by a drunk driver—you might be able to seek punitive damages. As laid out in Chapter 41 of the Texas Civil Practice & Remedies Code, these are not meant to compensate you. They are meant to punish the at-fault party and deter others from similar behavior. A Houston car accident lawyer can tell you if these might apply to your case.

You Don’t Have to Face the Insurance Company Alone

Going up against an insurance company after being hit by an uninsured driver can feel like an uphill battle. It’s a frustrating and overwhelming process, especially when your own insurer seems more interested in its profits than your recovery. You do not have to walk that path by yourself.

Let’s quickly review the hard truths:

- Uninsured drivers are a common and serious risk on Texas roads.

- Your uninsured motorist coverage in Texas is the financial safety net you paid for to protect you in this exact situation.

- Your insurance company will likely use tactics to delay, deny, or underpay what you’re rightfully owed.

You have rights, and having an experienced legal team in your corner can make all the difference—not just for your financial recovery, but for your peace of mind.

How a Dedicated Attorney Can Help

At The Law Office of Bryan Fagan, PLLC, our Houston car accident lawyers step in to handle the tough negotiations and legal complexities so you can focus on what truly matters: healing. When people look for legal help, they often check online reviews for lawyers to gauge a firm’s reputation. We’re proud of the trust our clients have placed in us.

We work on a contingency-fee basis. This means you pay absolutely no upfront costs. You don’t owe us a dime unless we win your case.

This approach removes the financial burden, giving you access to top-tier legal support when you need it most. We will take over all communication with the insurance company, gather the evidence to prove the full extent of your damages, and fight tirelessly to secure the compensation you deserve.

If you or someone you love was hurt by an uninsured driver in Houston, Dallas, Austin, San Antonio, or anywhere else in Texas, reach out to us. We offer a free, no-obligation consultation to answer your questions and explain your legal options in plain English. Let our compassionate and experienced team help you take the first step toward recovery.

Common Questions About Texas Uninsured Motorist Claims

When you're trying to heal and make sense of your life after a crash, the last thing you need is more confusion. To help you feel more in control, we’ve put together straightforward answers to some of the most common questions we hear from accident victims about uninsured motorist coverage in Texas.

What if a Hit-and-Run Driver Caused My Accident?

This is one of the most devastating scenarios, and it’s exactly why Uninsured Motorist (UM) coverage exists. If the driver who caused your injuries flees the scene and can't be identified, your UM policy is designed to step in and act as their insurance.

It's there to cover your losses, including:

- Your medical bills, from the emergency room visit to ongoing physical therapy.

- The income you lose from being unable to work.

- Your physical pain and emotional suffering.

Essentially, your own insurance company is supposed to cover the damages that the phantom driver should have paid for.

Will I Have to Sue My Own Insurance Company?

Our first goal is always to negotiate a fair settlement for you without ever stepping into a courtroom. In many cases, a skilled Houston car accident lawyer can successfully resolve a UM/UIM claim through firm negotiation and a detailed presentation of the evidence.

However, if your insurance company refuses to make a reasonable offer, unreasonably denies your valid claim, or otherwise acts in bad faith, a lawsuit may become necessary. Filing a lawsuit is a powerful tool that compels the insurer to take your claim seriously. Sometimes, it's the only way to secure the full compensation you deserve. An experienced attorney can advise you on the best legal strategy for your specific situation.

How Much UM/UIM Coverage Should I Carry in Texas?

While Texas law requires drivers to carry minimum liability insurance, those amounts are often dangerously low. They can be completely exhausted after even a moderately serious accident.

We strongly recommend that you carry uninsured motorist coverage limits that are at least equal to your own liability coverage.

Think of it this way: you buy liability insurance to protect your assets if you cause a crash. Your UM/UIM coverage should be robust enough to protect your health and financial future if someone else causes one. Higher limits provide a much stronger financial safety net.

Imagine cruising down I-10 in Houston, only to get rear-ended by a driver who speeds off. This nightmare is all too common in Texas, where approximately 1 in 7 vehicles on the road lacks the required insurance coverage. Newer data shows Texas's uninsured driver rate at an alarmingly high 13.8%, ranking the state 19th nationwide for this dangerous problem. You can learn more about Texas's uninsured motorist statistics to understand the risk.

Can I Combine UM Coverage from My Different Cars?

This is a common question, and the answer in Texas is generally no. Texas is what’s known as a “non-stacking” state. This means you typically cannot add together, or “stack,” the UM/UIM coverage limits from multiple vehicles listed on a single policy to apply to a single accident.

For example, if you have two cars on your policy, each with $50,000 in UM coverage, you cannot combine them to get $100,000 in coverage for one crash. You are usually limited to the single highest policy limit.

However, insurance policies are complex legal documents, and there can be exceptions. It is vital to have an experienced personal injury attorney review your specific policy to determine the exact amount of coverage available to you.

The legal system is complicated, but you don't have to face it alone. The team at The Law Office of Bryan Fagan, PLLC is here to fight for your rights and help you secure the recovery you deserve. Contact us today for a free, no-obligation consultation to discuss your case at https://houstonaccidentlawyers.net.