A car crash can change your life in seconds—but you don’t have to face recovery alone. The initial shock of the collision is overwhelming. Then comes the devastating discovery that the driver who hit you has no insurance. Suddenly, you’re facing a mountain of medical bills and repair costs, wondering how you'll ever get back on your feet.

The Unfortunate Reality of Uninsured Drivers on Texas Roads

Being hit by an uninsured motorist isn't just a worst-case scenario; it's a common problem on Texas roads. The moments after a crash are a blur of adrenaline and confusion. Learning that the person responsible for your injuries was driving illegally without liability coverage can make you feel completely powerless.

That feeling of helplessness is a harsh reality for thousands of Texans. In fact, our state has one of the highest rates of uninsured motorists in the country. Recent data shows that roughly one in seven Texas drivers is on the road without the required insurance. This means your chances of being in this exact situation are far higher than you might think.

A Safety Net You Might Not Know You Have

Thankfully, you may already have a critical safety net in your own auto insurance policy: Uninsured Motorist (UM) coverage. Think of it as a shield that protects you and your family when the at-fault driver simply cannot pay for the harm they’ve caused. It is designed specifically for this frustrating situation.

This guide will serve as your roadmap to understanding your rights and options. We’ll explain in plain English:

- What uninsured and underinsured motorist coverage is and how it works for you.

- The practical steps to file an auto insurance claim with your own provider.

- How to fight for the compensation you need for a full recovery.

After a crash, trying to navigate the claims process can be overwhelming. But you are not out of options. The Law Office of Bryan Fagan, PLLC is here to help you take back control. Our Houston car accident lawyers can stand between you and the insurance company, fighting to protect your rights and secure the fair compensation you rightfully deserve.

Your Financial Shield Against Uninsured Drivers

Think of Uninsured and Underinsured Motorist (UM/UIM) coverage as your personal financial safety net. It’s designed to protect you and your family not just in your own car, but also if you’re a passenger in someone else’s vehicle or even a pedestrian hit by an uninsured driver. It's a specific part of your own auto policy that kicks in when the person who caused the crash can’t pay for the damage they’ve done.

Many Texas drivers are surprised to learn they have this coverage. Under state law, insurance companies are required to offer UM/UIM with every policy they sell. If you don't want it, you must formally reject it in writing. Because most people don't take that extra step, they often have this valuable protection without even realizing it.

This coverage is your first line of defense in two incredibly common and frustrating situations.

Uninsured Motorist (UM) Coverage

Uninsured Motorist (UM) coverage is exactly what it sounds like: it protects you when the at-fault driver has zero liability insurance. It’s also your only path to recovery in a devastating hit-and-run where the driver is never identified. Instead of being stuck with all the bills, you can file a claim with your own insurance company to cover your medical expenses, lost wages, and other damages.

Imagine you're a Houston driver rear-ended on I-45. The police find the other driver 100% at fault, but it turns out they let their insurance lapse. Without UM coverage, you'd be on the hook for everything. With it, your own insurer essentially steps into the shoes of the at-fault driver's insurance company, giving you a way to get compensated.

Underinsured Motorist (UIM) Coverage

Underinsured Motorist (UIM) coverage is slightly different but just as critical. This applies when the at-fault driver has insurance, but their policy limits are too low to cover all of your losses. This is a massive problem here in Texas.

The state’s minimum liability limits—just $30,000 per injured person—are often completely exhausted by a single trip to the emergency room after a serious crash. UIM coverage is there to bridge that dangerous financial gap.

Let’s say you are rear-ended on I-10, and the accident causes a neck injury that requires surgery and months of physical therapy. Your medical bills quickly reach $80,000, and you miss two months of work. The driver who hit you only has the state minimum $30,000 liability policy.

Once their insurance pays its limit, you’re still facing $50,000 in medical debt, not to mention your lost income and the pain you’ve endured. This is exactly when your UIM coverage kicks in. You can then file a claim against your own policy to recover the remaining damages. You can learn more in our detailed guide to underinsured motorist coverage in Texas.

Texas’s required minimums—$30,000 per person, $60,000 per accident for injuries, and $25,000 for property damage—are dangerously low. The medical bills from even a moderate wreck can easily surpass $30,000, creating a huge gap between what you're owed and what the at-fault driver's insurance can pay.

Navigating The UM And UIM Claim Process

You might think filing a claim with your own insurance company would be simple. After all, this is why you pay your premiums. But when it comes to uninsured motorist coverage in texas, things can get complicated—fast. Your insurer's financial interests don't always align with yours.

Even though it's your policy, your insurance provider can quickly shift from being your protector to your adversary. Their goal is often to protect their bottom line, which means paying out as little as possible. This is where the process can feel like a fight, but taking the right steps will protect your rights.

Practical Steps to File an Insurance Claim

What you do in the moments and days after a collision is critical. Strong documentation and timely reporting are the foundation of a successful UM/UIM claim.

-

Call 911 Immediately: Always report the accident to the police. A formal police report is a powerful piece of evidence that documents the at-fault driver's information (or their lack of insurance) and provides an official, unbiased account of what happened.

-

Notify Your Insurer Promptly: Your policy has a strict deadline for reporting an accident. Contact your insurance company as soon as you can to let them know about the crash and that you might need to open a UM/UIM claim.

-

Document Everything: Gather every piece of evidence you can. Take photos of the accident scene, vehicle damage, and your injuries. Get contact information from any witnesses. Start a file and keep every medical bill, receipt, and record of lost wages.

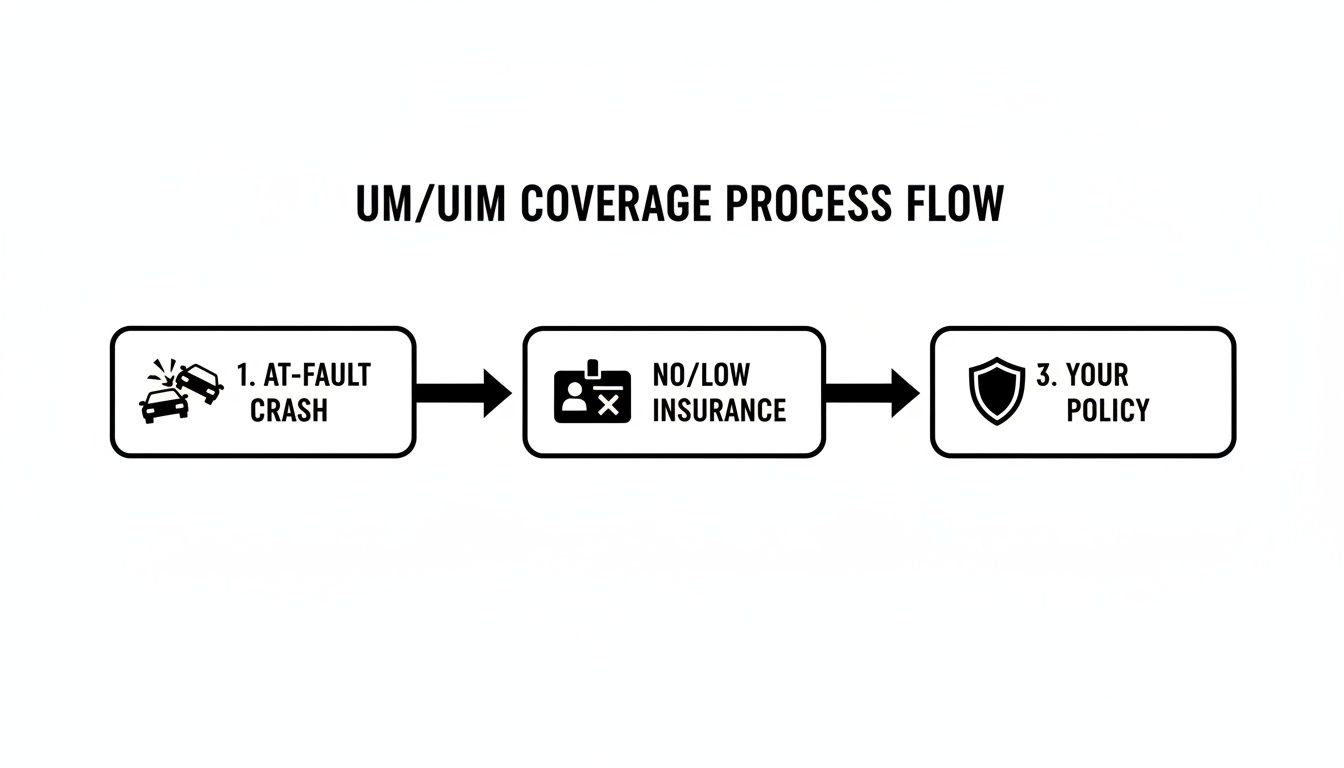

This diagram breaks down how your own insurance policy is designed to step in and shield you when the at-fault driver's coverage is missing or inadequate.

As you can see, your UM/UIM coverage acts as a vital financial backstop, turning a potential disaster into a manageable situation.

Be Cautious With Recorded Statements

Your insurance adjuster will ask you for a recorded statement about the accident. You are not legally required to give one, and it's almost always a bad idea to do so before speaking with a Houston car accident lawyer.

Adjusters are trained to ask questions that can bait you into saying something that could be used to devalue or deny your claim. They might try to get you to downplay your injuries or unintentionally admit partial fault. Remember, anything you say can be held against you.

Crucial Tip: When the adjuster calls, politely tell them you aren't comfortable giving a recorded statement and that your attorney will provide all necessary information. This simple step can protect you from common insurance company traps.

As you move through the process, you'll need to formally present your case. Using a well-structured personal injury demand letter template can make a huge difference. Still, insurers look for any reason to poke holes in a claim. They might question the severity of your injuries or argue a pre-existing condition is the real source of your pain. If your claim gets unfairly denied, knowing what to do when insurance denies your claim is the next critical step.

At The Law Office of Bryan Fagan, PLLC, we handle these communications for you. We know how to present the facts of your case without putting your rights at risk.

Understanding Your Rights and Recoverable Damages

Knowing what you’re legally entitled to is the first step toward a fair recovery. Even though you’re filing a claim for uninsured motorist coverage in Texas, the core principles of personal injury law still apply. You must understand them to build the strongest possible case for the compensation you deserve.

Your insurance company won’t just write you a check. They will investigate this just as seriously as the other driver's insurer would have, and the burden of proving your case rests on your shoulders.

Who is Liable in a Texas Car Accident?

In plain English, liability is the legal term for responsibility. To win your claim, you must prove the uninsured or underinsured driver was negligent—and that their negligence caused your injuries. This means showing they failed to act as a reasonably careful driver would have.

For example, if a driver on a San Antonio road runs a red light and T-bones your car, that is a clear violation of traffic laws and solid evidence of negligence. A Texas injury attorney would use the police report, witness statements, and traffic camera footage to establish liability.

However, the insurance company will scrutinize every detail to see if they can shift some of the blame onto you. This is where a critical Texas rule comes into play.

How Comparative Fault Affects Your Recovery

Texas follows a "modified comparative fault" rule, found in Chapter 33 of the Texas Civil Practice & Remedies Code. In simple terms, comparative fault is a legal doctrine that addresses situations where more than one person shares blame for an accident.

Here’s how it works for you:

- If you are found to be 50% or less at fault, you can still recover money. However, your total compensation will be reduced by your percentage of fault.

- If you are found to be 51% or more at fault, you are barred from recovering any compensation at all.

Let's say your total damages are $100,000, but an insurer argues you were 10% to blame. Under this rule, your final recovery would be cut by 10%, leaving you with $90,000. It's a common tactic insurers use to reduce payouts.

The Types of Damages You Can Recover

The money you receive in a personal injury claim is called damages. It is meant to compensate you for all losses—financial and personal—that you suffered because of the accident. These damages are typically split into two main categories:

Economic Damages: These are the tangible losses with a clear dollar amount, such as medical bills, lost wages from time off work, reduced future earning capacity, and the cost to repair your car.

Non-Economic Damages: These are the intangible losses that don't come with a receipt but are just as devastating. This category covers physical pain, mental anguish, scarring or disfigurement, and the loss of your ability to enjoy your life.

A skilled Texas injury attorney will meticulously document every loss to calculate the full, true value of your claim.

The Critical Two-Year Deadline

In Texas, you have a strict time limit to take legal action, known as the statute of limitations. For most personal injury cases, you have just two years from the date of the crash to file a lawsuit.

If you miss this deadline, you will almost certainly lose your right to seek compensation forever. Insurers know this clock is ticking and may use delay tactics, hoping you'll run out of time. Acting quickly is one of the most important things you can do to protect your claim.

It's also worth remembering that insurance companies are under financial pressure. Recent industry filings reveal they're dealing with soaring claim costs, which gives them a powerful incentive to challenge, deny, and limit what they pay out. You can learn more about the factors pushing up Texas auto insurance rates from the Texas Department of Insurance.

Why You Need a Car Accident Lawyer for Your Claim

Trying to get your own insurance company to pay on an uninsured motorist coverage in Texas claim can feel like you’re going into battle outnumbered. You’ve paid your premiums faithfully, trusting them to have your back. But now, you’re up against adjusters and lawyers whose job is to protect the company’s bottom line, not yours.

Going it alone is a risk you don’t have to take.

A dedicated Houston car accident lawyer from The Law Office of Bryan Fagan, PLLC instantly levels the playing field. We become your shield and your advocate, ensuring your rights are defended at every turn. The moment we take your case, the stressful, high-pressure phone calls stop for good.

Building an Undeniable Case for Your Recovery

A successful UM/UIM claim isn’t just about telling your story; it’s about backing it up with powerful evidence. Our legal team hits the ground running, gathering every piece of proof needed to establish the other driver's liability and the full cost of your damages.

This thorough process often involves:

- Accident Reconstruction: We can bring in experts to recreate the crash, using science to prove exactly who was at fault.

- Evidence Collection: We dig deep, securing police reports, traffic camera footage, witness statements, and cell phone records to build a clear timeline.

- Medical Expert Testimony: We work with your doctors and other medical specialists to paint a detailed picture of your injuries, treatment needs, and future prognosis.

Our mission is to leave no stone unturned. We bundle this evidence into a demand package that an insurance company cannot ignore. When a lawyer takes on your case, they may rely on expert legal intake services to efficiently manage initial client contact and ensure every detail is properly documented from the start.

Calculating the Full Value of Your Claim

One of the most critical roles a Texas injury attorney plays is determining what your claim is actually worth. This goes far beyond adding up your current medical bills. Insurance adjusters often make a quick, lowball offer that ignores the long-term impact of a serious injury.

We calculate every loss you've faced, including:

- Future Medical Expenses: This covers future surgeries, ongoing physical therapy, prescriptions, and medical equipment.

- Lost Earning Capacity: If your injuries prevent you from returning to your old job—or working at all—we calculate the lifelong financial impact.

- Pain and Suffering: We fight to assign a fair dollar value to the physical pain and emotional trauma the accident has inflicted on you and your family.

By meticulously documenting your future needs, we ensure you aren't stuck paying out-of-pocket for accident-related costs years from now. Our goal isn’t just to cover your immediate bills; it’s to secure a settlement that provides for your complete recovery.

Handling a UM/UIM Claim With vs. Without an Attorney

Navigating a UM/UIM claim is a maze of legal hurdles. The table below shows how different the journey can be when you have an experienced attorney from our firm fighting for you.

| Task | On Your Own | With The Law Office of Bryan Fagan |

|---|---|---|

| Communicating with the Insurer | Directly fielding calls from adjusters trained to weaken your claim. | We handle all communications, protecting you from pressure tactics and legal traps. |

| Gathering Evidence | Struggling to get police reports, witness contacts, and medical records. | Our team immediately begins a formal investigation, using legal tools to secure all necessary evidence. |

| Valuing Your Claim | Likely underestimating your claim by focusing only on current bills. | We conduct a comprehensive damage assessment, including future medical needs and lost earning potential. |

| Negotiating a Settlement | Accepting a lowball offer without knowing what your case is truly worth. | We leverage our trial-ready reputation and evidence to negotiate from a position of strength. |

| Meeting Deadlines | Risking missing the statute of limitations or other critical filing deadlines. | Our firm meticulously manages all legal deadlines to ensure your rights are preserved. |

Having a skilled advocate doesn't just make the process easier—it fundamentally changes the odds in your favor.

Proven Negotiation and Trial Readiness

With a rock-solid case built on hard evidence, we don’t just ask for a fair settlement—we demand it. Our reputation as trial-tested lawyers often motivates insurance companies to offer a fair settlement without ever needing to go to court. They know we are prepared to fight.

This readiness to go to trial is your biggest advantage. We handle the aggressive tactics and legal back-and-forth, freeing you to focus on what really matters: your health and your family. Having a lawyer from The Law Office of Bryan Fagan in your corner is the surest way to maximize your chances of getting the justice you deserve.

Common Questions About UM and UIM Claims in Texas

Navigating the aftermath of a car accident is confusing. When the other driver is uninsured or underinsured, it can feel like you’ve been left to pick up the pieces alone. You likely have many questions. We’ve provided clear, straightforward answers to the concerns we hear most often from accident victims.

How Much UM and UIM Coverage Should I Carry?

This is one of the most important financial decisions you can make to protect your family. While Texas law only requires insurers to offer you the bare minimum for UM/UIM coverage ($30,000 per person / $60,000 per accident), that is a dangerously low amount. A single serious injury can easily result in medical bills that far exceed those limits.

A smart strategy is to match your UM/UIM coverage to your own bodily injury liability limits. If you carry $100,000 in liability coverage to protect others, you should carry at least $100,000 in UM/UIM coverage to protect yourself. The cost to increase these limits is usually small, but the financial security it provides is priceless.

Think of it this way: your liability coverage protects your assets if you cause a crash. Your uninsured motorist coverage in Texas protects your health and your family’s future from someone else’s recklessness.

What if I Was the Victim of a Hit and Run?

A hit-and-run is one of the most frustrating things that can happen on the road. The driver who hurt you took off, leaving you to deal with the consequences. This is exactly what Uninsured Motorist (UM) coverage was designed for.

Since the at-fault driver cannot be identified, the law treats them as an uninsured motorist. This allows you to file a claim against your own UM policy to cover your medical bills, lost wages, and other damages.

However, there is a critical requirement.

To successfully use your UM coverage after a hit-and-run, you almost always need to prove there was actual physical contact between the “phantom” vehicle and your car. This rule exists to prevent fraud.

Because of this specific proof requirement, having a Texas injury attorney on your side is critical. We know how to gather evidence, like paint transfer on your car or witness statements, to prove the hit-and-run happened and ensure your claim is paid.

Will Filing a UM Claim Make My Insurance Rates Go Up?

This is a common fear that unfortunately stops many people from using the benefits they’ve paid for. The good news is that Texas law is on your side.

State law prohibits an insurance company from raising your premiums for filing a UM/UIM claim for an accident that wasn't your fault. You pay for this coverage as a safety net, and you have every right to use it without worrying about a rate hike.

Filing a claim for any of these reasons should not impact your rates:

- You were in a crash caused by an uninsured or underinsured driver.

- You were the victim of a hit-and-run.

- Your vehicle was hit while legally parked.

If an insurer tries to raise your rates or drop your coverage after a not-at-fault claim, they are likely acting in bad faith, and you should seek legal advice immediately.

Do I Have to Sue My Own Insurance Company?

The goal of any uninsured motorist coverage in Texas claim is to get a fair settlement without going to court. In most cases, a skilled Houston car accident lawyer can achieve this through tough negotiation backed by a trial-ready case.

However, insurance companies don't always play fair. They might:

- Unreasonably delay your claim.

- Make a lowball offer that doesn't cover your losses.

- Deny your claim based on a flimsy excuse.

In those situations, filing a lawsuit against your own insurance company might be the only way to hold them accountable. This legal action forces them to take your claim seriously and often brings them to the negotiating table with a real offer. While a lawsuit is a last resort, our attorneys are always prepared to take this step to protect your rights.

A car crash can leave you with serious injuries and overwhelming financial burdens, but you do not have to face the insurance companies alone. At The Law Office of Bryan Fagan, PLLC, our compassionate attorneys are here to fight for your rights, your recovery, and your future. If you were hurt by an uninsured or underinsured driver, contact us today for a free, no-obligation consultation to understand your legal options. Let our experienced Texas injury attorneys help you get the justice and wrongful death compensation you deserve.