A car crash can change your life in seconds—but you don’t have to face recovery alone. When another driver’s negligence causes a wreck, you have the right to seek compensation directly from their insurance company. This is called a third-party claim, and it’s how you hold the at-fault driver financially responsible for your medical bills, lost income, and the pain you’ve endured.

Simply put, you’re demanding payment from the people who caused the harm, not from your own insurer. This guide is here to walk you through that process, step by step, and empower you with the knowledge to protect your rights.

Who Is Liable in a Texas Car Accident?

Before you can get a single dollar from the other driver's insurance, you have to establish one critical concept: liability. In plain English, liability means determining who is legally responsible for the accident and all the damage it caused.

Under Texas law, the person whose carelessness—or negligence—caused the crash is the one held liable. When that person is the other driver, you have the right to file a claim against them and their insurance company. This is what makes them the "third party," and proving their liability is the foundation of your entire case.

What is Negligence in a Car Accident?

Negligence isn't about someone intentionally setting out to cause a wreck. It’s about a person failing to act with the same caution that any other reasonable person would in that situation, and that failure leading directly to someone getting hurt.

Here’s a real-world example: A Houston driver on I-45 glances down to read a text message and drifts into your lane, sideswiping your car. They’ve acted negligently. Their momentary carelessness directly caused the collision, which makes them liable for your injuries and vehicle repairs.

Proving Fault is Everything

Here’s the hard truth: insurance companies won't just take your word that their driver was at fault. Their investigators will immediately start looking for ways to pin the blame on you, because their primary goal is to pay out as little as possible.

To build a successful third party claim, you and your attorney must gather solid evidence to prove four key elements:

- Duty: The other driver had a basic legal responsibility to drive safely and follow all traffic laws.

- Breach: They failed in that duty by doing something careless, like speeding, running a red light, or texting while driving.

- Causation: Their careless action was the direct cause of the crash and your injuries.

- Damages: You suffered real, measurable harm—the legal term for all your losses, like medical bills, lost income, and physical pain.

Under Chapter 33 of the Texas Civil Practice & Remedies Code, our state uses a "modified comparative fault" rule. This means you can still recover money even if you were partially to blame for the accident, as long as your share of the fault is 50% or less. Your final compensation, however, will be reduced by whatever percentage of fault is assigned to you.

This rule is exactly why insurance adjusters will fight so hard to shift even a tiny bit of the blame your way. If they can convince a jury you were 10% at fault, they can instantly slash their payout by 10%. It’s a common tactic, and it's one of the biggest reasons why having an experienced Houston car accident lawyer on your side is so critical.

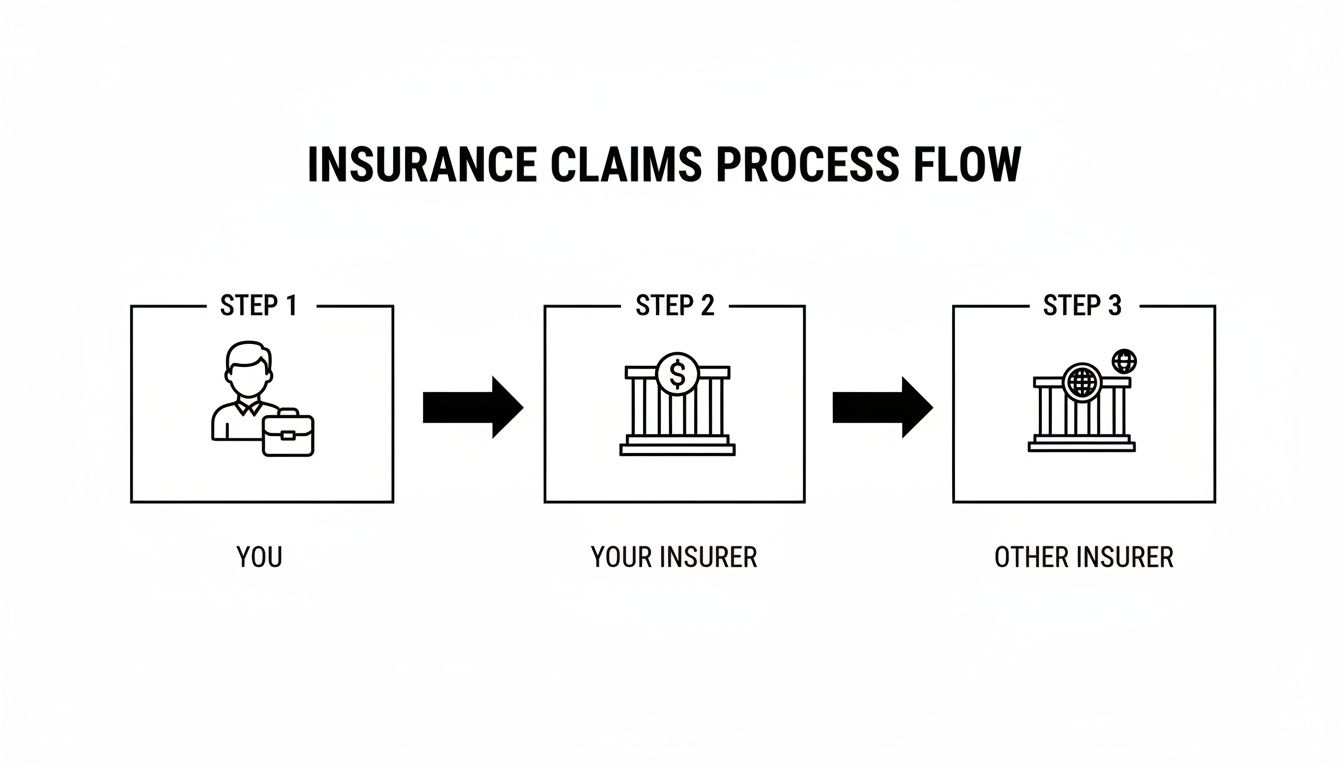

Understanding First-Party vs. Third-Party Claims

After a car wreck, insurance jargon can feel like a foreign language. You’ll hear adjusters and attorneys throw around terms like “first-party” and “third-party” claims, but what do those actually mean for your recovery?

Understanding this difference is one of the most important first steps toward getting the financial help you need. It all comes down to who you’re filing the claim against.

Let's break down the players involved:

- You are the first party: The person injured in the collision.

- Your insurance company is the second party: The insurer you have a contract with.

- The at-fault driver and their insurer are the third party: The ones you are making the claim against.

First-Party Claims: Using Your Own Policy

Imagine you were rear-ended on the Katy Freeway. Your neck is already hurting, and you need to see a doctor now—but the other driver's insurance company hasn't even bothered to call you back. This is where your own policy comes in handy with a first-party claim.

A perfect example is using your Personal Injury Protection (PIP) coverage. In Texas, PIP is a no-fault benefit that helps cover your immediate medical bills and some lost wages, no matter who caused the crash. Filing a PIP claim is a first-party action because you’re dealing directly with your own insurance company.

Third-Party Claims: Holding the At-Fault Driver Accountable

Now, let's talk about the main event. Your PIP coverage might only offer a few thousand dollars, which is rarely enough to cover all your losses after a serious crash.

To recover the full value of your damages—including all your medical expenses, lost income, vehicle repairs, and compensation for pain and suffering—you must file a third-party claim. This claim is aimed directly at the insurance company for the driver who hit you. You are making it clear that their client was negligent and is legally on the hook for making you whole again. This is your primary path to getting full and fair compensation.

A third-party claim is your opportunity to hold the negligent driver accountable. It isn’t about hitting the lottery; it’s about recovering everything that was taken from you—your health, your financial security, and your peace of mind.

What if the At-Fault Driver is Uninsured or Underinsured?

What happens when the driver who hit you has no insurance at all, or just the bare-minimum policy that won't cover your serious injuries? This is where another kind of first-party claim can save the day: Uninsured/Underinsured Motorist (UM/UIM) coverage.

If you have this protection on your policy, your own insurance company essentially steps into the shoes of the at-fault driver's insurer and pays for your damages up to your policy limits. We've laid out the key differences in this table to make it even clearer.

First Party vs. Third Party vs. UM/UIM Claims at a Glance

| Claim Type | Who You File With | What It Typically Covers | Common Scenario |

|---|---|---|---|

| First-Party (PIP) | Your own insurance company | Initial medical bills & a portion of lost wages (no-fault) | You need immediate funds for doctor visits after a crash. |

| Third-Party | The at-fault driver's insurance company | All damages: medical bills, lost income, vehicle repair, pain & suffering | The other driver ran a red light and caused your injuries. |

| First-Party (UM/UIM) | Your own insurance company | Your damages when the at-fault driver has no insurance or not enough | A hit-and-run driver, or someone with only state-minimum coverage, seriously injures you. |

A compassionate Texas injury attorney will build a strategy that pulls from every available policy—first-party and third-party—to make sure you get the maximum recovery possible. You can also learn more about the differences between first-party and third-party claims in our detailed article to get a deeper understanding.

Steps to File an Insurance Claim

The moments after a car crash are chaotic and disorienting. What you do right then and there is absolutely crucial for protecting your rights. Every action you take—or don't take—can either build a strong foundation for your third-party claim or give the insurance company an excuse to tear it down.

Here is some practical, step-by-step advice on what to do after a crash to give yourself the best possible chance at a fair recovery.

1. Seek Immediate Medical Attention

Even if you think you feel fine, go see a doctor. Adrenaline is a powerful hormone that can easily mask serious injuries like internal bleeding or whiplash, which might not show symptoms for hours or even days. Getting checked out right away creates an official medical record that directly links your injuries to the accident. If you wait, the other driver's insurance company will argue your injuries aren't that serious or that something else caused them.

2. Report the Accident to the Police

Always call 911 from the scene. Don't let the other driver talk you out of it. An officer will create an official Texas Peace Officer's Crash Report, one of the most important pieces of evidence you can have. It will document contact and insurance details, witness statements, and often, an initial opinion on who caused the crash.

3. Gather Your Own Evidence at the Scene

If you’re physically able, use your phone to take pictures and videos of everything: all vehicle damage, skid marks, traffic signs, and any visible injuries. Also, get the names and phone numbers of anyone who saw what happened. An independent witness who can back up your story is incredibly powerful.

4. Report the Crash, but Be Careful What You Say

You should notify your own insurance company that an accident occurred. But you do not have to speak with the at-fault driver’s insurance adjuster, and you should never give them a recorded statement without first talking to a lawyer.

Adjusters are trained to ask leading questions designed to trick you into minimizing your injuries or admitting partial fault. Anything you say in a recorded statement can and will be used to devalue or deny your auto insurance claim.

The safest move is to politely decline and tell them your attorney will be in touch. This one simple step protects you from their tactics. For more details, review the critical steps to take immediately after a car accident.

Calculating Damages and the Texas Statute of Limitations

Figuring out what your third-party claim is actually worth is a critical step. When you file a claim against the at-fault driver's insurance, you’re seeking compensation for your damages—the legal term for all the losses you’ve suffered.

In Texas, these damages fall into a few key categories. A skilled Houston car accident lawyer will meticulously calculate each one to ensure your demand for compensation reflects everything you and your family have endured.

Economic and Non-Economic Damages

First, you have economic damages, which are the straightforward financial losses with a clear paper trail.

- Medical Expenses: This covers everything from the ambulance ride and ER visit to ongoing physical therapy, surgeries, medications, and any future medical care you’ll need.

- Lost Wages: If your injuries kept you out of work, you can claim the income you lost, as well as your "diminished earning capacity" if you can no longer do your job at the same level.

- Property Damage: This is the cost to repair or replace your vehicle and any personal property destroyed in the collision.

Next are non-economic damages. These are tougher to put a number on, but they are just as real. This is compensation for the human cost of the crash, including pain and suffering, mental anguish, physical impairment, and loss of enjoyment of life.

Punitive Damages for Gross Negligence

In some extreme cases, Texas law allows victims to seek punitive damages. As laid out in Chapter 41 of the Texas Civil Practice & Remedies Code, these aren't meant to repay you for a loss. Instead, their purpose is to punish the at-fault driver for shocking recklessness and to deter others from similar behavior. For example, a court might award punitive damages if you were hit by a drunk driver.

The Two-Year Statute of Limitations

This is absolutely crucial: there is a strict deadline for taking legal action. In Texas, the statute of limitations for most personal injury claims is two years from the date of the accident. If you don't file a lawsuit within that two-year window, you lose your right to seek compensation forever.

This deadline is unforgiving. Imagine your family is devastated by a truck accident on Houston's Beltway 8 and you're pursuing a wrongful death compensation claim. With liability claims surging 57% in the last decade, the stakes for families have never been higher. Discover more insights about rising liability claims from Aon's global study. Missing that two-year deadline means losing any chance at justice. To get a handle on these critical timelines, you can learn more about the statutes of limitations in Texas in our article.

Why a Houston Car Accident Lawyer Is Your Best Ally

When you file a third-party claim, you are stepping into an adversarial process. The at-fault driver’s insurance company is a massive corporation focused on one thing: protecting its bottom line. Their adjusters and lawyers are trained to minimize payouts, not to make sure you get what you’re owed.

Hiring an experienced Houston car accident lawyer from The Law Office of Bryan Fagan, PLLC, is the most critical step you can take to even the odds. We become your advocates, fighting to protect your rights and secure your future.

Leveling the Playing Field Against Insurers

The moment you hire us, we take over. Our team launches a thorough investigation, digging for the evidence that builds an undeniable case. We handle all communication with the insurance company, shielding you from their tactics.

The other driver’s insurance adjuster is not your friend. Their job is to find reasons to minimize your injuries, shift blame, and pay you as little as possible. Our job is to stop them.

We make sure you are never taken advantage of. While you focus on your physical and emotional recovery, we carry the complex legal weight.

Maximizing Your Financial Recovery

Insurers love to make a quick, lowball offer, hoping you’ll take the money before you understand the true cost of your injuries. We don't let that happen. Our attorneys collaborate with medical and financial experts to calculate the full, long-term value of your claim, including:

- All current and future medical expenses.

- Total lost income and diminished earning capacity.

- Real compensation for pain, suffering, and emotional distress.

We are tough negotiators who prepare every case as if it’s headed to trial. This sends a clear message to the insurance company that we won't back down.

Best of all, you don't have to face this battle alone or worry about how to afford it. We work on a contingency fee basis, which means you pay us absolutely nothing unless we win your case. There are no upfront costs or hidden fees.

Common Questions About Third-Party Claims in Texas

After a wreck, your mind is probably racing with questions. It's a confusing, stressful time, and not knowing your rights only makes things worse. Here are some straightforward answers to the questions we hear most often.

How Long Does a Third-Party Claim Take in Texas?

There’s no single answer. A straightforward claim might wrap up in a few months, but complicated cases can take a year or longer. The timeline depends on the severity of your injuries, arguments over fault, and the insurance company's tactics. An experienced Texas injury attorney knows how to counter these delays and keep the pressure on.

Should I Talk to the Other Driver's Insurance Company?

We strongly advise against it. Never give a recorded statement or sign anything without talking to a lawyer first. Their adjusters are trained to ask tricky questions to get you to downplay your injuries or accidentally admit fault. The safest move is to politely decline and tell them your attorney will be in touch.

What if I Was Partially At Fault for the Accident?

You can still recover money. Texas follows a "modified comparative fault" rule (Chapter 33 of the Texas Civil Practice & Remedies Code). This law says you can recover damages as long as your share of the fault is 50% or less. Your final compensation, however, will be reduced by your percentage of fault.

What if the At-Fault Driver's Insurance Is Not Enough?

This is a common problem. If the driver who hit you only carried the state-minimum liability coverage, it often won’t be enough. A good attorney will immediately look for other sources of recovery, like your own Underinsured Motorist (UIM) coverage, which can cover the difference.

A car accident can make you feel lost and powerless, but you don’t have to navigate this alone. If someone else’s carelessness left you injured, the dedicated team at The Law Office of Bryan Fagan, PLLC is ready to fight for you. We’ll handle the insurance companies, protect your rights, and work tirelessly to get you every dollar you deserve. Contact us for a free consultation today to discuss your case and learn how we can help.